A card payment may feel like a simple exchange between a customer and a merchant, but in reality, it depends on coordination between two different financial institutions. One represents the shopper who is making the purchase, and the other represents the business accepting the payment.

These two roles sit at the centre of the global card payments system and are known as issuing and acquiring.

The issuing bank provides the payment card and manages the relationship with the cardholder, whereas it’s the acquiring bank’s job to enable businesses to accept card payments and makes sure they eventually receive the funds from those transactions. Every card payment moves between these two sides, with the card network connecting them and allowing information to pass from one side to the other.

The difference between issuing and acquiring affects many important areas, including approval rates, fraud prevention, interchange fees and the timing of settlement.

The four party card model

Most card payments operate within what is known as the four party model, a structure which involves four main participants. These include the cardholder who is making the purchase, the merchant who is accepting the payment, the issuing bank that provided the card and the acquiring bank which enables the merchant to accept it.

Connecting these participants is the card network, which provides the rules and the technical infrastructure to allow transactions to move between financial institutions.

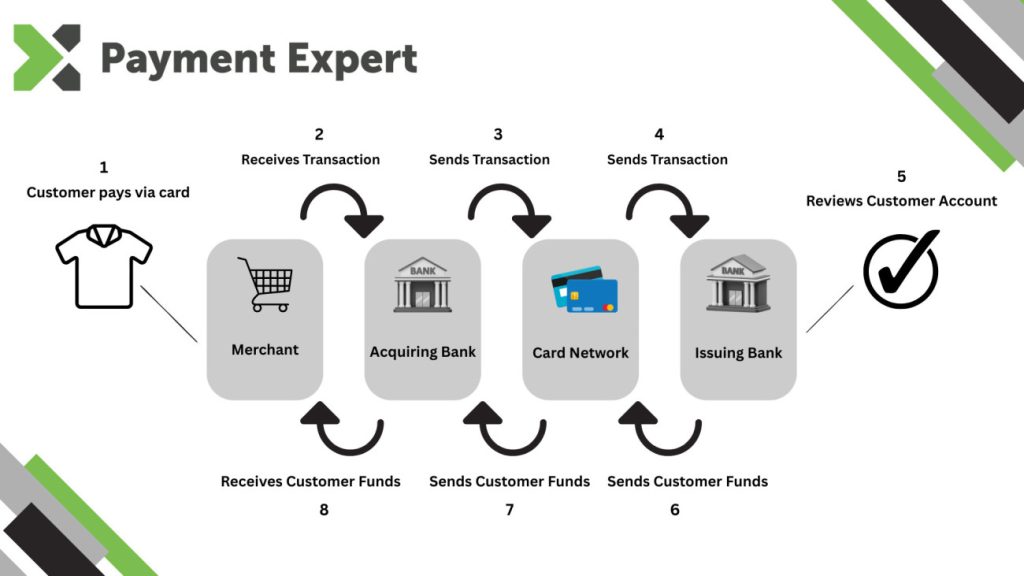

When a customer taps a card at a payment terminal or enters their details online, the transaction request begins with the merchant’s payment provider. It is then sent to the acquiring bank, which forwards it through the card network to the issuing bank linked to the card.

The issuing bank reviews the request and decides whether the transaction should be approved or declined. Although this process takes only a few hundred milliseconds, several systems are involved and multiple checks take place before the final decision is returned to the merchant.

What issuing banks do

In order to understand how these roles fit together, it helps to look at what each side of the system actually does.

Starting with issuing banks, these are responsible for the side of the payment that relates to the cardholder.

When a consumer receives a credit or debit card, the issuing bank has already completed the work needed to create that payment instrument. This includes onboarding the customer, verifying their identity, linking the card to a bank account and managing the credit limit or deposit balance behind it.

Every transaction from the issuer’s point of view, carries some level of financial risk. The bank must confirm the card is valid, the account is active and the customer has enough funds or available credit to complete the purchase. It must also identify and prevent fraudulent activity, often using data analysis and risk models to assess each payment.

These checks take place during the authorisation stage of a transaction. When a payment request arrives through the card network, the issuing bank reviews the information in real time and decides whether the payment should be approved or declined.

Issuers are also responsible for managing the full lifecycle of the card, overseeing credit card billing, handling disputes and chargebacks, replacing lost or expired cards, supporting tokenisation for digital wallets and providing customer service when cardholders experience problems.

In simple terms, the issuing bank is the financial institution which supports the cardholder and takes responsibility for the payment card they use.

What acquiring banks do

Acquiring banks play the equivalent role on the merchant side of the payment. While issuing banks focus on cardholders, acquiring banks focus on the businesses accepting card payments. They provide merchants with the systems and services needed to process transactions, which may include payment terminals in physical stores, online gateway connections and the settlement services which ensure funds eventually reach the business.

Before a merchant can accept cards, the acquiring bank must onboard the business and assess the level of risk involved. This process includes verifying the business is legitimate, reviewing its activities and evaluating the potential for fraud or chargebacks.

Once the merchant account is in place, the acquirer becomes responsible for sending transactions into the card networks and ensuring the merchant receives payment for approved purchases.

This responsibility involves a number of operational steps, including the acquiring bank collecting authorised transactions and grouping them together for processing through the card network.

After the network calculates the financial obligations between issuers and acquirers, settlement funds are transferred from issuing banks to the acquiring bank, which then pays the merchant.

The acquirer from the merchant’s perspective is the institution that makes card acceptance possible. It manages the processing of payments, oversees the timing of settlement and often provides tools to help businesses monitor transactions, manage fraud and reconcile their accounts.

How issuing and acquiring interact during a transaction

When a customer initiates a transaction at a checkout page or payment terminal, the request begins with the merchant’s payment system. The transaction details are sent to a gateway or payment processor, which forwards them to the acquiring bank.

The acquiring bank then passes the authorisation request through the card network, and the network identifies which issuing bank provided the card and routes the request to the correct institution.

The issuing bank then performs a series of checks, confirming the card is valid, verifies sufficient funds or credit are available and analyses the transaction for signs of fraud. Within a few milliseconds it returns a response through the network to the acquiring bank indicating whether the payment is approved or declined.

If the payment is approved, the merchant can complete the sale. However, the funds do not move straight away. The transfer of money takes place later during clearing and settlement, when the issuing bank sends funds through the network to the acquiring bank, which then pays the merchant.

How fintech is changing issuing and acquiring

Although the fundamental roles remain the same, the boundaries between issuing and acquiring are evolving as tech aims to make transactions faster and safer.

Fintech infrastructure providers have introduced new layers into the payments ecosystem, making it easier for both financial institutions and technology companies to participate in card issuing and merchant acceptance.

Issuer processors now allow banks and fintechs to launch card programmes without needing to build the technology, while payment facilitators bring large numbers of smaller merchants under a single acquiring relationship, which makes onboarding simpler for digital platforms and online marketplaces.

At the same time, embedded finance models are allowing non-banks to participate more directly in issuing activities, offering branded cards through partnerships with regulated banks.

On the acquiring side, global payment service providers now combine gateway technology, risk management and acquiring connectivity into unified platforms which operate across multiple markets.

These developments blur some operational distinctions, but they do not remove the foundational structure.