A Payment Expert regional guide to SEPA Instant

SEPA Instant lets a person or business move euros between two accounts in under ten seconds, at any hour, on any day of the year. The European Payments Council (EPC) runs the scheme that makes this possible, and the European Union has now made it mandatory for most banks in the euro area.

This guide sets out what the scheme is, what the law requires, where each region stands, and the numbers behind the roll-out.

What is SEPA Instant?

SEPA Instant is the common name for the SEPA Instant Credit Transfer (SCT Inst) scheme. The EPC launched it in November 2017, which sets a single rulebook that any payment service provider (PSP) in the SEPA area can follow to send and receive euro credit transfers in real time.

The scheme’s core promise, as defined by the EPC:

- Funds reach the payee’s account in less than ten seconds.

- The service runs 24 hours a day, every calendar day, including weekends and holidays.

- It works across the SEPA area, which spans 36 countries (41 including territories), using IBANs and the ISO 20022 messaging standard.

It’s worth confirming the SCT Inst is a scheme, not a piece of infrastructure. PSPs clear and settle the transactions through clearing and settlement mechanisms (CSMs).

The three pan-European CSMs are TARGET Instant Payment Settlement (TIPS), operated by the European Central Bank (ECB), and RT1 and STEP2-T, operated by EBA Clearing.

The scheme is voluntary; the law is not

Adherence to SCT Inst was optional for its first seven years, though this changed with Regulation (EU) 2024/886, the Instant Payments Regulation (IPR). The European Parliament and the Council adopted it on 13 March 2024, after it was published in the Official Journal on 19 March 2024 and entered into force on 8 April 2024.

The IPR amends the SEPA Regulation and adds instant-payment provisions to the Cross-Border Payments Regulation, the Settlement Finality Directive and the Payment Services Directive (PSD2). It converts the voluntary scheme into a legal obligation for PSPs that already offer standard euro credit transfers.

What the IPR requires

The ECB sets out four main obligations under the regulation.

- Instant credit transfers (Article 5a). A PSP that offers standard euro credit transfers must also offer instant euro credit transfers, both sending and receiving.

- Equality of charges (Article 5b). A PSP cannot charge more for an instant credit transfer than it charges for a standard credit transfer of the same type. In practice this means instant payments must be offered at or below the price of a normal transfer.

- Verification of Payee (Article 5c). A PSP must offer the payer a service that checks whether the payee’s name matches the account identifier before the payment is sent. The service must be free to the payer and applies to both standard and instant transfers.

- Sanctions screening (Article 5d). A PSP offering instant credit transfers must check its own payment service users against EU sanctions lists at least once a day, rather than screening each transaction as it happens.

The daily-screening model is a change from transaction-by-transaction screening, and the ten-second execution window leaves no time to screen each payment against sanctions lists in real time, so the regulation moves the check to the customer level.

The ten-second rule, in detail

The 2025 SCT Inst rulebook tightened the internal timing the regulation required when the EPC changed the scheme’s processing sub-timeline from 10-20-25 seconds to 5-7-9 seconds.

The receiving PSP must now make the funds available to the payee, or reject the transfer, within ten seconds of the payment order being received. The rulebook now requires the transaction timestamp to include milliseconds, because a ten-second hard limit makes sub-second timing more important.

The regulation also removed the scheme-level cap on transaction size. The EPC rulebook states a maximum amount at scheme level no longer applies, beyond any maximum set by the SEPA Regulation itself.

The deadlines

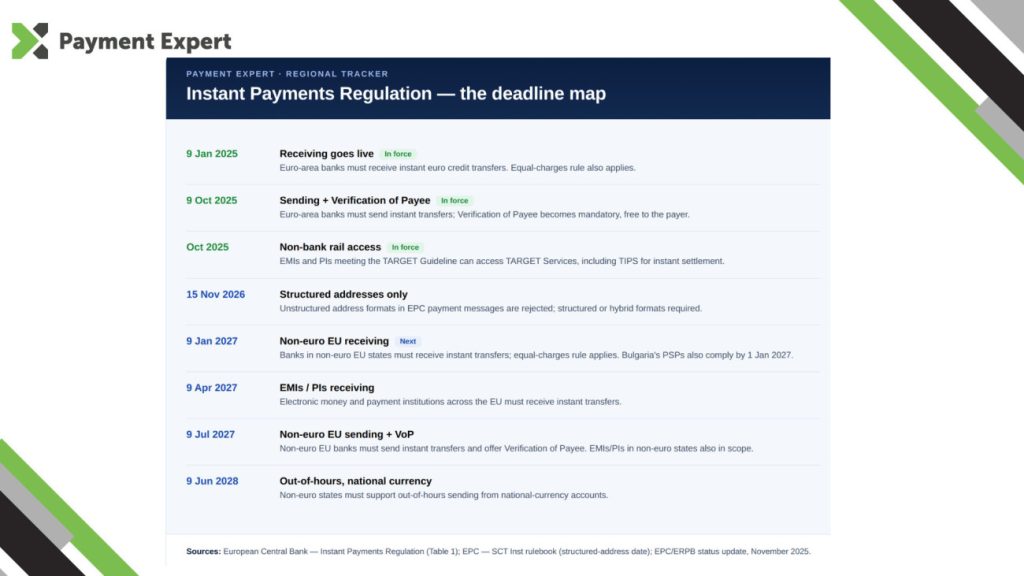

The IPR applies on a staggered basis. The dates below come from the ECB’s official implementation table (Table 1).

Receiving instant payments

- Euro area Member States: 9 January 2025

- Non-euro area Member States: 9 January 2027

- Electronic money institutions (EMIs) and payment institutions (PIs), euro area and non-euro area: 9 April 2027

Sending instant payments

- Euro area Member States: 9 October 2025

- Non-euro area Member States: 9 July 2027

- EMIs and PIs in euro area Member States: 9 April 2027

- EMIs and PIs in non-euro area Member States: 9 July 2027

- Out-of-hours sending from national-currency accounts, non-euro area: 9 June 2028

Equality of charges

- Euro area: 9 January 2025

- Non-euro area: 9 January 2027

Verification of Payee

- Euro area: 9 October 2025

- Non-euro area: 9 July 2027

Two deadlines have already passed for euro-area banks: receiving instant payments (9 January 2025) and sending them, alongside Verification of Payee (9 October 2025). The next large wave falls in 2027, when EMIs, PIs and non-euro-area PSPs come into scope. The EPC said in its November 2025 status update that it does not expect another large wave of scheme adherence applications before July 2027.

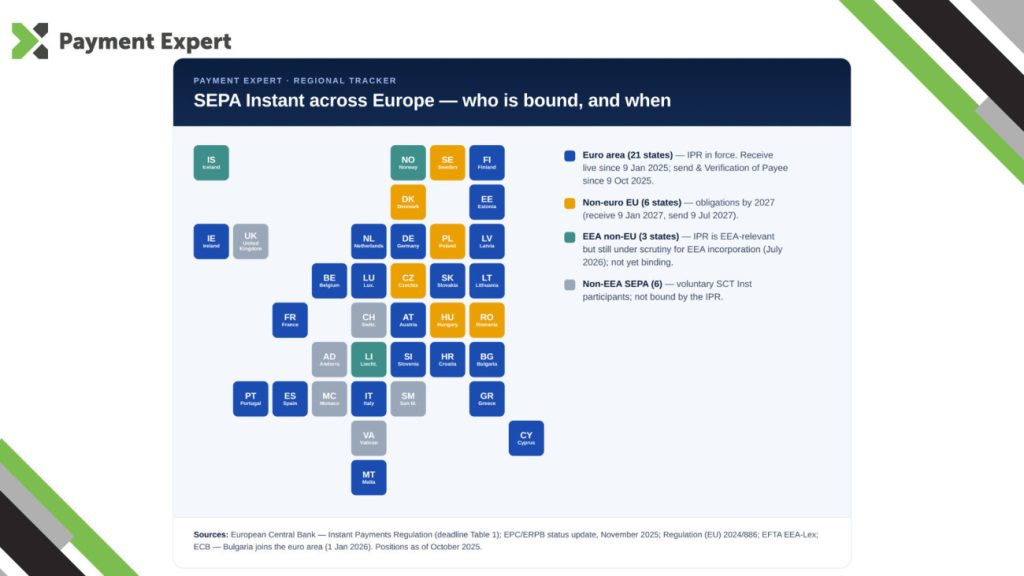

Where each region stands

The obligations that apply to a PSP depend on where it sits.

Euro area (21 Member States). Banks in the 20 states that were in the euro area before 2026 are already bound by the receiving, sending, charging and Verification of Payee rules.

Bulgaria adopted the euro on 1 January 2026 and became the 21st euro-area member. The regulation sets a separate deadline for a state that adopts the euro mid-timeline: where the euro is introduced before 9 April 2027, that state’s PSPs must comply with Articles 5a, 5b and 5c within one year of the euro’s introduction.

Bulgarian PSPs therefore have until 1 January 2027 to meet the instant-transfer, equal-charges and Verification of Payee obligations.

Non-euro EU (6 Member States: Czechia, Denmark, Hungary, Poland, Romania, Sweden). PSPs here face the 2027 deadlines, plus the 9 June 2028 date for out-of-hours sending from national-currency accounts.

Under the SEPA Regulation as amended, PSPs in a non-euro state are not obliged to offer sending of instant euro transfers above a per-transaction limit, which competent authorities set at a level no lower than EUR 25,000 for a renewable one-year period.

EEA non-EU (Iceland, Liechtenstein, Norway). The IPR is marked as EEA-relevant, meaning as of July 2026, the EFTA EEA-Lex register records the regulation as still under scrutiny for incorporation into the EEA Agreement, with no Joint Committee Decision yet in force. It does not yet bind PSPs in the three EEA-EFTA states, and no compliance dates apply to them until incorporation completes.

Non-EEA SEPA (United Kingdom, Switzerland, Monaco, San Marino, Andorra, Vatican City). PSPs in these jurisdictions can join the SCT Inst scheme voluntarily, as they are not bound by the IPR, which applies to PSPs in the EU and, where incorporated, the wider EEA.

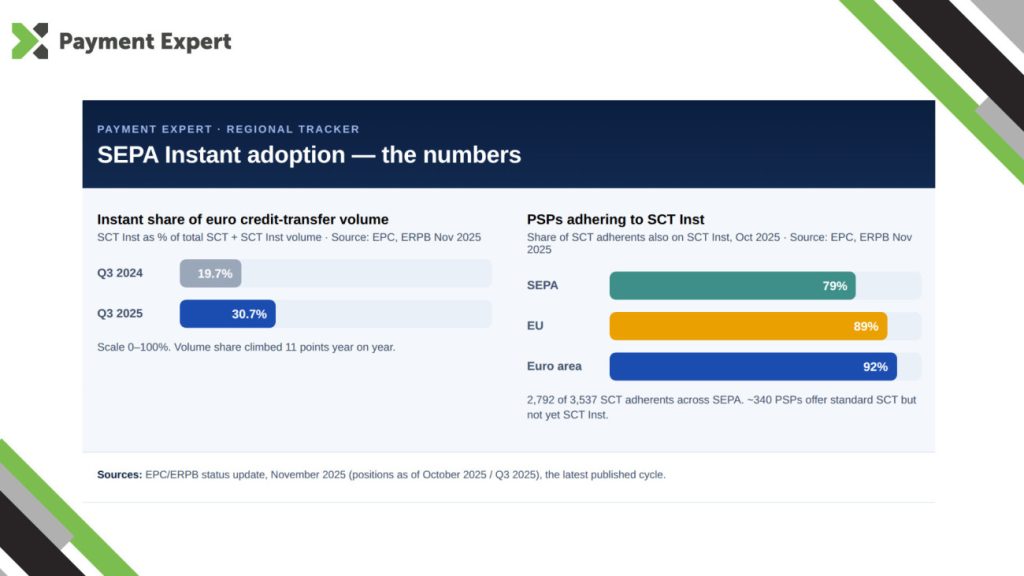

The numbers

Adherence and volume figures come from the EPC’s status update to the Euro Retail Payments Board (ERPB) in November 2025, reporting positions as of October 2025.

- Scheme participants: 2,792 PSPs had joined SCT Inst as of October 2025, out of 3,537 SCT adherents across SEPA. This is 79% across SEPA, 89% across the EU, and 92% across the euro area.

- The remaining gap: about 340 PSPs offer standard SCT but not SCT Inst. The EPC said these are mostly either exempt from the IPR or located in non-euro-area EU countries.

- Transaction volume: SCT Inst transactions made up 30.7% of the total volume of euro credit transfers (SCT plus SCT Inst) in the third quarter of 2025, up from 19.7% in the third quarter of 2024.

Verification of Payee and the fraud angle

Verification of Payee (VoP) went live for euro-area PSPs on 9 October 2025, which the EPC published the rulebook for on 10 October 2024, with an entry-into-force date of 5 October 2025.

A VoP check returns one of four results before the payment is sent: match, close match, no match, or other, where the payer sees the result and decides whether or not to proceed. The Eurosystem offers a VoP service built on solutions from Banco de Portugal and Latvijas Banka, designed to the EPC’s VoP scheme.

The EPC reported 2,782 VoP scheme participants as of its November 2025 update, of which 2,713 were ready for operations, and said the deployment “went better than expected.”

VoP is the regulation’s main answer to authorised push payment (APP) fraud, in which a payer is tricked into sending money to an account they believe belongs to someone else. The name-check gives the payer a warning before the funds leave, and instant transfers are irrevocable once settled.

Two operational changes

Structured addresses. From 15 November 2026, EPC payment messages may use only structured or hybrid address formats, and unstructured addresses will be rejected.

The EPC moved this date from 22 November 2026 in version 1.1 of the 2025 rulebook to align with the Swift Standards MX release. PSPs and their corporate customers that still send unstructured address data must change their files before that date.

Non-bank access to central-bank rails. Non-bank PSPs can now settle instant payments without routing through a sponsor bank. Since October 2025, EMIs and PIs that meet the conditions in the TARGET Guideline can access TARGET Services directly, including T2 for settlement and TIPS for instant settlement.