India’s grey‑market crypto economy, built by tens of millions of traders, faces the possibility of being wiped out should national banks press ahead with a country-wide crackdown on cryptocurrencies.

India has a reputation for being a leader in digital payments, but its central bank looks like it is closer than ever to introducing a nation-wide ban on crypto.

According to internal documents seen by Reuters, the Reserve Bank of India is recommending policies that lean towards a crypto ban, with concerns noted about financial stability, sovereignty and the difficulty of taxing crypto transactions.

The documents, which date from May and June 2026, suggest the possibility of barring banks and financial institutions from holding, trading or gaining any exposure to crypto assets and privately issued stablecoins.

The RBI has held this position for some time; the latest documents show that it hasn’t been inspired by Europe’s recent MiCA milestone or progress being made in the US.

The juxtaposition is what’s bringing attention to the RBI. The institution behind the Unified Payments Interface, one of the most adopted real‑time payment systems in the world, now looks closer to banning an asset class that Europe, the US, the UK and others are racing to regulate.

The case against crypto and stablecoins

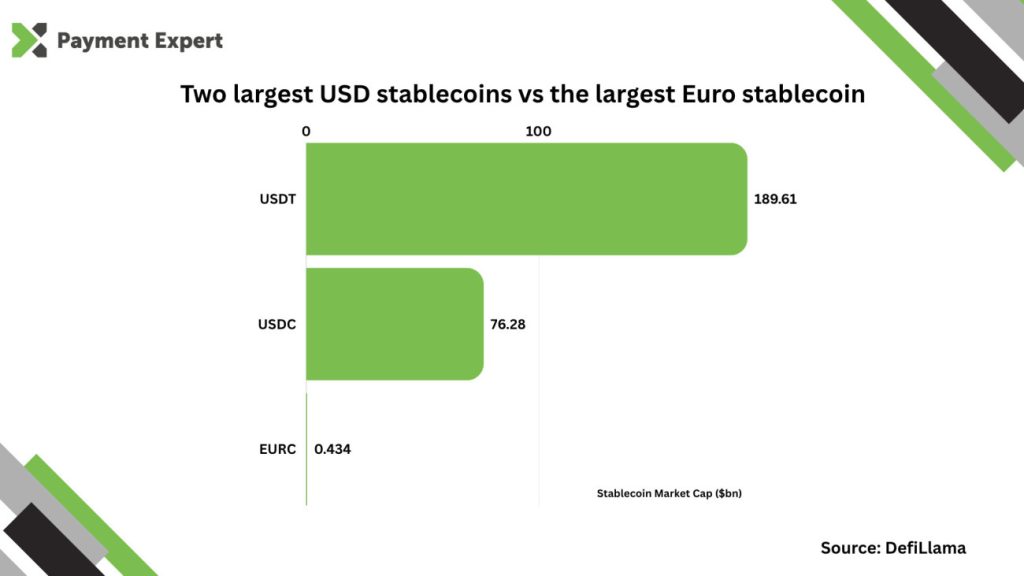

Stablecoins are perhaps the most surprising mention in the documents, with the digital asset having significantly different characteristics from crypto. Stablecoins have been lauded over recent years for their ability to send funds across borders at speed, on a 24/7 basis, while still being traceable and also maintaining their value due to being pegged 1:1 to a fiat currency.

However, the documents suggest that the RBI views tokens backed by foreign currencies as a threat to rupee sovereignty. This opinion is shared by several markets such as Europe, which isn’t helped by the fact that stablecoin market share is currently dominated by dollar‑pegged tokens in USDT and USDC.

Rupee‑backed stablecoins are also viewed as posing a problem because it is believed they could erode the government’s income from issuing fiat currency and create instability during moments when the financial system is under pressure.

The RBI has also raised an enforcement issue around taxing firms in the sector. India taxes crypto gains at 30%, but the tax department found that fewer than a quarter of those who made crypto transactions in the financial year ending March 2023 declared them.

Crypto transactions routed through offshore exchanges and private wallets are difficult to trace, and peer‑to‑peer rupee trades leave taxable income largely invisible. The RBI argues that stablecoins intensify this opacity because they reduce the need to return to fiat, eliminating one of the rare points in the system where gains can be detected.

39 million traders left in limbo

Crypto activity operates in a grey market in India and despite no clear rules or regulations, the sector has grown exponentially.

According to Chainalysis, India’s crypto market was valued at $2.6bn in 2024 and is forecast to reach $15bn by 2035, showing how digital assets have taken hold even without a regulatory framework.

India’s tax department also estimates that the country has nearly 39 million crypto traders, placing it among the largest markets in the world for retail participation.

The reason for the grey zone, which may have hindered or helped this growth, is that draft legislation to ban private crypto was never ratified in 2021 and has yet to make a comeback.

The latest documents suggest that the desire to find a solution, whether that be a complete ban or something more nuanced, is still being worked out.