Speaking with industry leaders at Money20/20 Europe, Payment Expert explores whether sandboxes, strict rulebooks or market-led regulation is best to lead the next era of crypto, stablecoins and AI.

Stablecoin and crypto regulation has recently stolen the show in payments, with Europe absorbed by the MiCA deadline, the UK’s Financial Conduct Authority (FCA) providing long-awaited clarity on stablecoins, and the US… well, the US has been the US.

If regulators from all three regions decided to go bowling, the UK would want to play a few hundred warm‑up games before anyone started counting scores, Europe would be reading out the instructions on where the ball is meant to go and the US would already be at the bar.

It’s obviously a joke, but it sums up how all three markets are approaching stablecoin and crypto regulation completely differently. The UK is obsessed with sandboxes, Europe is writing strict rulebooks and the US is letting the market take the lead.

The US looks like it’s in the lead because it’s happy to take action and ask questions later, but speed isn’t the be‑all and end‑all for regulators, as the other two markets will happily remind you.

The UK’s love for sandboxes

The UK has made sandboxes part of its regulatory identity. The FCA and Bank of England appear to favour supervised experimentation so consistently that Payment Expert Editor Rachael Kennedy joked about “another one” on an episode of the Payment Expert podcast.

One currently taking place is the Digital Securities Sandbox, where 16 firms are testing the live issuance and settlement of tokenised assets. The FCA and Bank of England believe the technology could make markets “faster and more efficient”, but firms want clarity, and the sandbox is where that clarity can be discovered.

This is the environment Janet Bastiman, Chief Data Scientist at Napier AI, knows all too well. Speaking to Payment Expert at Money20/20 Europe, she offered her own take on the bowling‑alley analogy when describing the UK’s approach.

“It’s like the bumpers in a bowling alley,” she says. “It’s there to go, if you’re gonna do this, here’s how you can do it. They don’t necessarily go, do this, and we’ll be 100% happy with it.

“It’s like hearing the things you need to consider. Make sure that you don’t go too far in one direction because it’s not explainable. It gives you a little more confidence that you’re doing the right thing.”

Few people have been closer to the UK’s sandbox machinery than Bastiman. Her team was one of the first to turn a sandbox experiment into a regulated product, testing a model inspired by river‑pollution studies in China in which they applied fluid‑dynamics logic to financial flows to combat money laundering.

The FCA’s testing approach let her team push deeper into network detection without widening the search space, something she describes as an “aggressive surf”. It was computationally expensive, but the sandbox gave them room to prove it worked.

Some people just don’t like sand

Not everyone in the industry is sold on the UK’s sandbox strategy. Speaking to Payment Expert at Money20/20 Europe, Eric Barbier, Founder and CEO of Triple‑A, says: “I’ve never been a big fan of sandboxes.”

Barbier explains that they make sense when regulators need help understanding a new technology, but in areas like stablecoins, the model is no longer necessary.

“Sandboxes are good for things which are really, really early,” he says. “But when it comes to stablecoin payments, now it’s becoming vanilla.”

The UK, however, has been doing exactly this via its Stablecoins Cohort, announced in November 2025. The programme has turned the FCA’s Regulatory Sandbox into a testing ground for UK‑issued stablecoins, with Monee Financial Technologies, ReStabilise, VVTX and Revolut trialling products across retail payments, wholesale settlement and crypto trading.

Barbier believes this caution has come at a cost because issuers have focused on other markets while waiting for clarity. He doubled down on this, stating that he is a firm believer that “imperfect regulation is better than no regulation.”

Perhaps the biggest example of imperfect crypto regulation is Europe’s MiCA, a framework that beats the US on speed and the UK on caution.

Europe pushed rules through quickly to give companies a way in, but in doing so, created one of the strictest rulebooks in the market. Barbier tells Payment Expert that the region has “shot itself in the foot.”

One example is the travel rule, which requires every stablecoin transfer to carry sender and recipient data, adding friction to what was supposed to be a faster, cheaper alternative to correspondent banking.

“Vague regulations,” he says, highlighting the travel rule, “instead of working with industry players and trying to find something which works for everyone. I think that’s something they could have done better.”

US takes the lead on crypto regulation

Across stablecoins and crypto regulation, the US looks to be in pole position. From the start, the strategy has been to let the market lead and legislate what proves to work.

President Donald Trump has pushed this approach down the necks of lawmakers, at times making for uncomfortable viewing, urging them to pass crypto‑focused legislation and encouraging firms to innovate at speed.

Barbier, who has watched crypto regulation develop across multiple markets, says the answer for any jurisdiction looking to get it right is simple. “You copy and paste Singapore or US regulation and you’re done, right?”

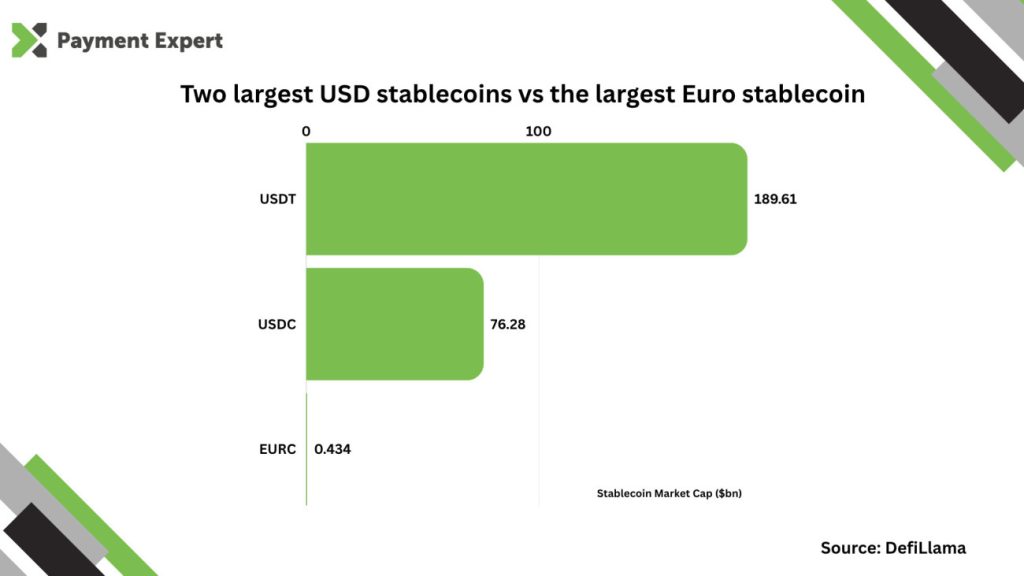

The line Trump repeatedly goes back to is making the US “the crypto capital of the world,” which is looking likely. In stablecoins, US‑issued tokens rule global circulation, with USDT and USDC accounting for the majority of supply and settlement volume.

However, the US crypto regulation strategy comes with trade‑offs, much like the approaches of the UK and Europe previously mentioned. A market‑led model can create gaps in consumer protection, uneven standards across states and uncertainty around how federal agencies will treat emerging models.

The UK’s model is slower, more supervised and criticised for caution, though it provides shared understanding between regulators and innovators, something Bastiman believes is misunderstood.

“There was a lot of suspicion that if regulators get involved, then it stifles innovation and that’s not really what it’s about,” she explains.

“Cynically, I think that’s pushed by people who either don’t want to understand or who want to move quickly and then use the excuse that ‘if we’d done it in a regulated way, we’d have never succeeded.’”

She tells Payment Expert that the reality is very different. “Whereas the FCA is really trying to push us. We’re all in it for the same reasons.”