Circle’s 2025 results show surging USDC adoption and doubled EBITDA — but the real story is a business model built on distribution deals that constrain margins as much as they drive growth

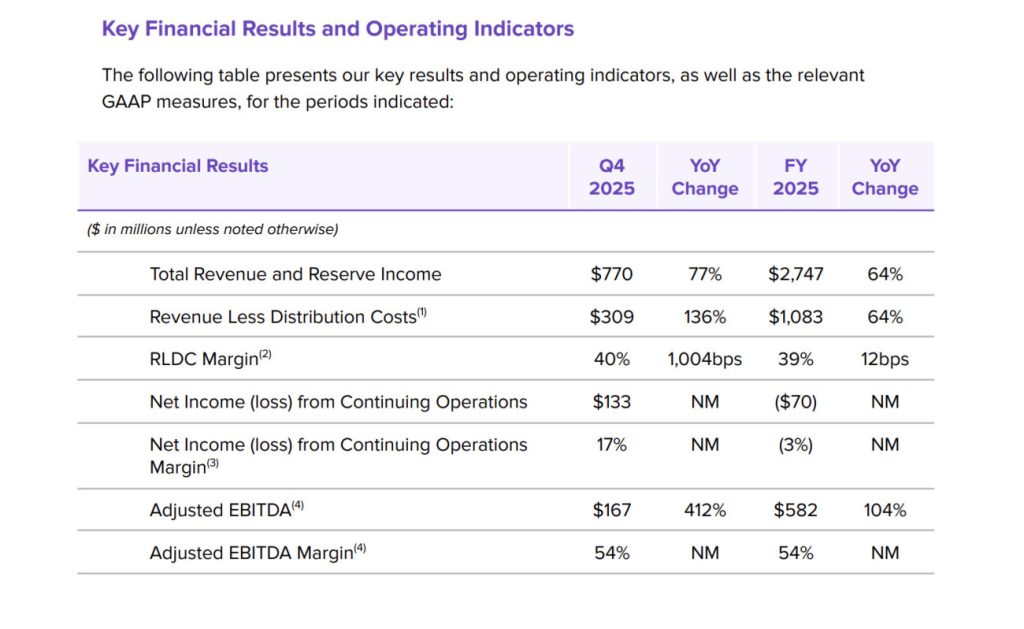

Circle reported full-year 2025 revenue and reserve income of $2.75bn on 25 February, up 64% year-on-yea and driven largely by a 72% rise in USDC circulation ($75.3bn).

Reserve income – interest earned on the assets backing USDC – accounts for the majority of this figure, a distinction which matters when assessing the business model.

Adjusted EBITDA more than doubled to $582m, reflecting strong operating leverage. A reported net loss of $70m for the year was almost entirely attributable to $424m in one-off stock-based compensation triggered by IPO vesting – Q4 alone delivered a $133m net profit.

More telling than any single line, however, is what is driving the underlying growth: a fundamental shift in how enterprises, banks, and payment networks are beginning to settle value.

Average USDC circulation across the full year reached $64.9bn – nearly double the prior year’s average – while on-chain transaction volume for Q4 alone hit $11.9tn, a 247% year-on-year increase.

The scale of that volume growth suggests USDC is moving well beyond crypto-native use cases into mainstream payment flows.

Enterprise adoption moves from pilot to platform

Perhaps the most significant signal in Circle’s results is the quality and scale of the partnerships being announced alongside them.

Visa confirmed that US issuers and acquirers can now fully settle using USDC, which enabled continuous settlement outside traditional banking hours for the first time.

Intuit launched a multi-year strategic partnership to integrate USDC across its platform, connecting Circle’s stablecoin infrastructure to millions of small and medium-sized businesses. Polymarket, the world’s largest prediction market by volume, adopted USDC as its core collateral and settlement asset.

And in a development which speaks to broader sovereign interest, the Government of Bermuda announced plans to become the world’s first fully on-chain national economy, underpinned by Circle’s infrastructure.

The common thread across each is settlement finality – reducing reliance on traditional correspondent rails in different segments of the market.

Distribution costs reveal the underlying economics

While the partnership announcements reflect Circle’s commercial momentum, the company’s distribution and transaction costs rose to $1.66bn for the full year — 60 cents of every dollar of revenue and reserve income paid out to the partners who hold and distribute USDC.

The revenue less distribution costs (RLDC) margin of 39% was flat year-on-year despite 64% revenue growth, meaning Circle’s unit economics did not improve as it scaled. This means the more USDC circulates, the more Circle pays to keep it circulating.

To understand why, it helps to understand the structure of Circle’s agreement with Coinbase, its largest distribution partner and an equity stakeholder in the business.

Under terms disclosed in Circle’s IPO filing, Coinbase receives 100% of reserve income generated from USDC held directly on its platform, and splits the remaining reserve income 50/50 with Circle.

In 2024, Coinbase received $908m of Circle’s $1.01bn in total distribution costs, roughly 54 cents in every dollar of revenue. Coinbase held around 22% of the total USDC supply by early 2025, and that share has been growing.

Critically, Circle cannot exit the agreement unilaterally. As long as Coinbase meets its obligations, the arrangement automatically renews on a three-year cycle, with the next renewal due later this year. Whatever that renegotiation yields will have a direct and material impact on Circle’s margin trajectory.

Adjusted EBITDA of $582m, more than double 2024’s figure, confirms the model generates meaningful earnings at scale.

But the pricing power question remains open: Circle’s ability to improve margins over time depends significantly on whether it can diversify distribution without simply replicating the same revenue-sharing economics elsewhere.

Competing with Tether and the rate risk ahead

So, while USDC’s 28% share of the USD-denominated stablecoin market is growing, the broader competitive picture is more complicated.

Tether‘s USDT holds a market cap roughly double that of USDC, and dominates the emerging market and cross-border trade corridors where B2B payment friction is highest; precisely the flows that payments professionals care most about. Meanwhile, USDC’s strength is concentrated in regulated, institutional markets.

Circle’s response to this has been to pursue distribution partnerships in markets where Tether has traditionally been strongest. A confirmed agreement with Binance, the world’s largest crypto exchange by volume and a key gateway to Asian and emerging market liquidity, extends USDC’s reach into corridors it has historically struggled to penetrate.

Notably, Coinbase agreed to share its own distribution fees to make the Binance deal work, accepting a reduction in its own revenue in exchange for growing the overall USDC network. That alignment of incentives between Circle and Coinbase is one of the more underappreciated aspects of the model.

The other structural headwind is interest rates. Circle’s reserve income, which accounts for the large majority of its revenue, is directly tied to prevailing rates on short-term US Treasuries.

As rates decline, so does reserve income, all else being equal. Circle’s ability to offset that pressure through fee-based revenue – from CPN transaction fees, Circle Mint, FX conversion, and custody services – is where the long-term investment case gets more complex.

Crucially, none of those revenue streams are subject to distribution-sharing arrangements, meaning Circle retains them in full. They are still small relative to reserve income, but it is reporting upward growth.

The Circle Payments Network, with 55 enrolled institutions and $5.7bn in annualised transaction volume, and the Arc blockchain, still in public testnet, are both early-stage by any honest measure. Global B2B cross-border flows run to tens of trillions annually; $5.7bn is a proof of concept, not a market position – but these will surely be product lines Circle looks to expand upon.