The RPIB consultation maps rails for bank deposits, stablecoins and a potential digital pound, with account-to-account at the checkout a key new journey

The Retail Payments Infrastructure Board (RPIB) wants the UK’s next payment rails to carry regulated stablecoins, a potential digital pound and ordinary bank deposits side by side, with a payer able to send in one form of money and the recipient receiving in another.

This interoperability across forms of money sits at the centre of its consultation on the design of the next-generation retail payments infrastructure, launched this week and running until 11 September.

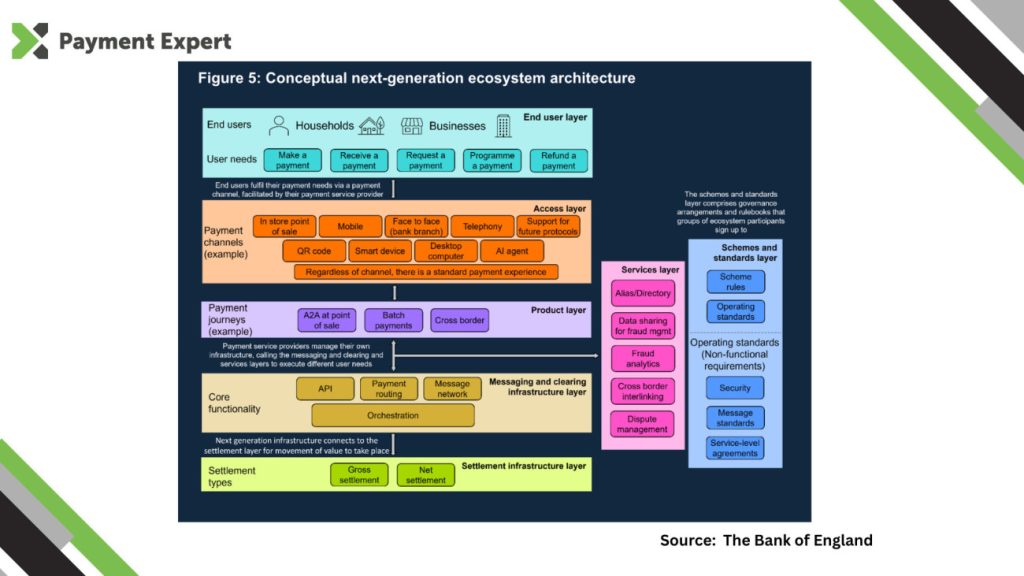

The Bank of England-chaired board is asking industry how to build the core clearing and messaging layer – the plumbing beneath the products and apps people actually use – that will eventually replace the interbank rails behind Faster Payments and BACS. Responses will shape a high-level design, or blueprint, to be handed to a new industry-led Delivery Company (DeliveryCo) to build.

The exercise follows the Future of Payments Review, which warned the UK, an early leader in real-time payments and open banking, had drifted without a clear long-term direction for its infrastructure. Pay.UK runs the existing systems in the meantime.

A checkout alternative to cards

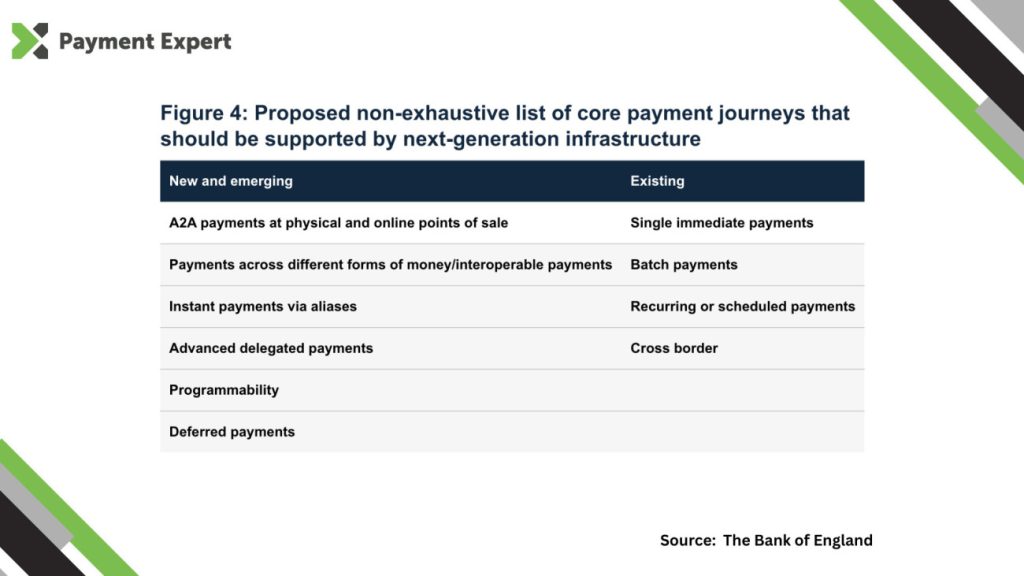

Among the new journeys, account-to-account (A2A) payments at the point of sale carry the most immediate commercial value.

The consultation pits in-store and online A2A as an alternative to cards, offering merchants faster settlement and potentially lower acceptance costs, and consumers more choice at the till.

To compete, the Bank says such payments would need near-instant confirmation that funds have cleared – certainty of fate – in fast-moving settings such as supermarkets and transport.

Pix in Brazil, UPI in India, Swish in Sweden and Bizum in Spain feature as A2A schemes that reached scale, each built around a single product arrangement with shared rules and branding.

In the UK, open banking already enables A2A through regulated payment initiation providers, and the Bank expects those propositions to evolve alongside the new infrastructure rather than be displaced by it.

Stablecoins and a digital pound on one rail

Banks and e-money firms already interoperate on today’s rails and the consultation floats regulated stablecoin issuers as a potential third type of direct participant, alongside the digital pound the Bank and HM Treasury are still assessing.

Those forms of money would exchange in the clearing layer at par, with final settlement in central bank money, preserving the principle that a pound is a pound whichever issuer holds it.

A modular, extensible core able to support payment journeys not yet imagined is the design the consultation sets out, and industry recognises the logic. Mike Walters, CEO of payments technology firm Form3, tells Payment Expert the document reflects the right instinct.

“The future of retail payments isn’t about creating a single new payment method, it’s about building infrastructure that can support continuous innovation,” he says, adding that instant, secure and seamless payments have become a baseline expectation.

Walters reads growing retailer adoption of Pay by Bank as a marker of where A2A is heading, though the gains for merchants and consumers depend on the rails beneath them.

“Those benefits will only be realised if the infrastructure behind them is right,” he says.

Because direct bank transfers are instant and irrevocable, a transaction “must authenticate, process and settle in seconds,” he adds, leaving no room for error and placing a premium on strong customer authentication and data protection.

AI agents and programmable payments

Programmability and AI agents feature too. The consultation asks how the core should handle programmable payments – transfers with conditions attached – and agentic payments, where software acts for a user within set limits.

It illustrates the latter with an AI assistant told to bid up to £200 on an online art auction during its owner’s working day, then settling the winning £160 bid from her account.

The Bank’s preference is to keep the core compatible with these patterns rather than embed the logic itself, with safeguards including clear attribution of how a payment was initiated and recovery routes when automation fails.

Walters sees the same dependency, arguing solid foundations are the only way to extend innovation to digital money and agentic commerce without weakening security or reliability.

RPIB chair Victoria Cleland called the work “a real opportunity to transform the UK’s retail payments infrastructure,” with a platform for innovation as the goal.

The consultation closes on 11 September, after which the board will publish a summary of responses and begin the high-level design phase.