UK Finance has outlined a nine-pronged approach for how the UK’s financial services industry can deliver on the government’s plan to deliver economic growth

Modernised retail payment infrastructure could generate £9bn annually in economic uplift, according to a new report published by trade association UK Finance.

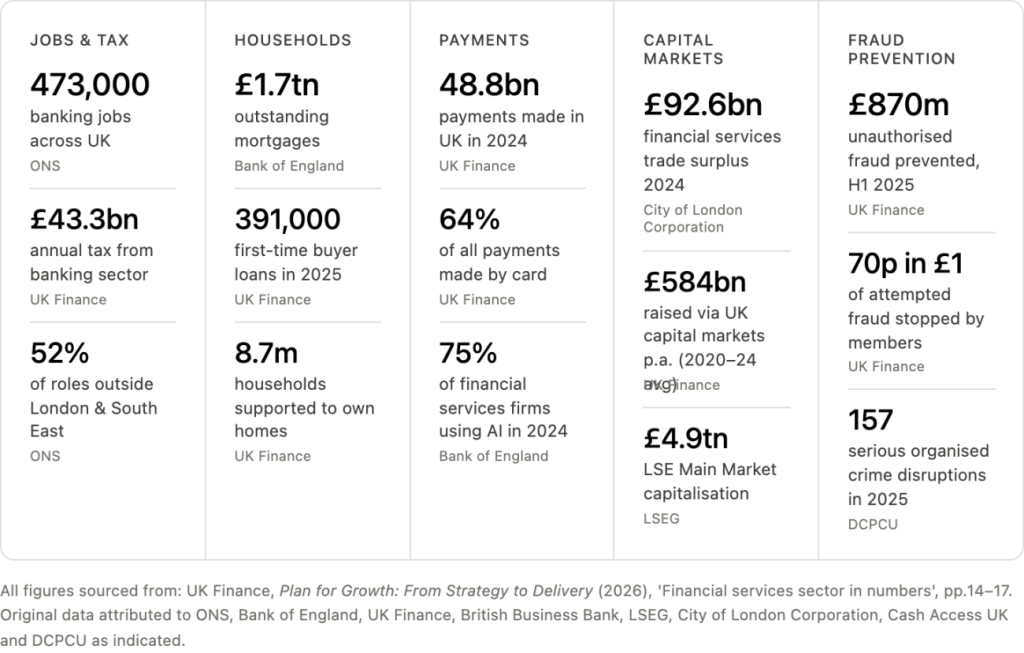

Its ‘Plan for Growth’ report, published today (11 May) identifies nine “growth enablers”, which it argues must be delivered in 2026 and beyond if the government’s economic strategies – covering housing, SME support, infrastructure, clean energy and financial inclusion – are to succeed.

The plan frames financial services reform not as a sectoral interest but as a prerequisite for broader economic renewal, arguing that every major government growth strategy carries an implicit dependency on specific financial services capabilities.

The nine reforms outlined by UK Finance can be summarised as follows:

- Reducing bank capital requirements – to unlock additional lending capacity

- Completing reform of redress arrangements – through the Financial Ombudsman Service

- Unblocking regulatory, supervisory and tax compliance barriers – holding back competitiveness

- Supporting payments modernisation and innovation – including open banking and tokenised deposits

- Transforming financial and capital markets – with tokenisation and T+1 settlement as priorities

- Strengthening technology and telecoms firms’ fraud obligations – to tackle APP fraud at source

- Supercharging government-backed SME support – scaling the Growth Guarantee Scheme to £5bn

- Broadening financial inclusion – for individuals and households

- Mobilising finance for housing – covering mortgages, new build and retrofit

Open banking reforms move back into focus

The report also renewed industry pressure on the Government to establish a commercially sustainable framework for open banking, an issue that has become increasingly contentious as adoption has grown.

UK Finance argued open banking’s long-term success depends on regulatory certainty and stronger commercial incentives for market participants. It called on HM Treasury to introduce legislation in 2026 that would place open banking “on a commercially sustainable, long-term regulatory footing”.

The document linked open banking directly to SME productivity, financial inclusion and the UK’s wider digital economy ambitions, suggesting policymakers increasingly view account-to-account infrastructure as part of the country’s strategic economic architecture rather than simply a fintech initiative.

The trade body also referenced the role of open banking in enabling more personalised financial services and future AI-driven commerce models, particularly as agentic payments begin moving from theory toward commercial experimentation.

On capital markets, UK Finance calls on the government to use this year’s Mansion House speech to confirm ambitions to position the UK as a global hub for tokenised markets, building on the forthcoming digital gilt issuance and the appointment of a ‘Wholesale Digital Markets Champion’. It also presses for delivery of T+1 settlement and share register digitisation by the end of 2027.

Fraud prevention receives a dedicated chapter. With 66% of authorised push payment fraud originating online and a further 17% through telecoms networks, the report argues the financial sector cannot remain the economy’s primary line of defence.

It calls for Ofcom to finalise and implement fraudulent advertising obligations under the Online Safety Act by early 2027 at the latest, and for mandatory seller verification and secure payment defaults on online marketplaces – potentially via legislation in the King’s Speech.

Below is a visualisation of UK Finance’s roadmap:

UK Finance backs tokenised deposits over regulatory uncertainty

Another notable aspect of the report is its strong support for tokenised commercial bank deposits, with UK Finance urging regulators to provide greater flexibility for its “Great British Tokenised Deposit” (GBTD) initiative.

The initiative aims to explore programmable sterling deposits and distributed ledger settlement infrastructure, which UK Finance and EY estimate could eventually deliver more than £3bn in economic benefits through operational efficiencies, fraud reduction and settlement improvements.

At the same time, the report warned that prolonged uncertainty around the UK’s digital money framework could begin affecting investment decisions across the sector.

UK Finance said HM Treasury, the FCA and the Bank of England should progress stablecoin regulation carefully while also reaching a clearer position on the future of a digital pound.

Capital and compliance top the agenda

The most immediate priority, according to UK Finance, is translating the Financial Policy Committee‘s (FPC) revised 13% Tier 1 capital benchmark into reduced binding requirements for individual banks.

While the FPC’s decision to lower its benchmark from 14% has been welcomed, the report warns without explicit action from the Prudential Regulation Authority (PRA), the lending capacity implied by the change will remain unrealised.

Large UK banks currently hold common equity tier 1 (CET1) ratios averaging 14.6% – more than 4% above the low point of recent stress tests. UK Finance argues this represents significant excess capital that could be deployed into mortgages, SME lending and infrastructure finance.

It also calls for reform of the leverage ratio, which it says has become a binding ceiling on balance sheet growth for banks holding large volumes of low-risk assets, noting that seven of the world’s ten most leverage-constrained banks are UK institutions.

On regulatory burden, the report welcomes the planned merger of the Payment Systems Regulator (PSR) into the Financial Conduct Authority (FCA) and calls for primary legislation to lock it in, alongside further simplification of the Senior Managers and Certification Regime (SMCR).

It also urges the government to extend its 25% compliance cost reduction target to cover supervisory and tax administration burdens – not just rule-making – and calls for greater regulatory sequencing to reduce the overlapping demands placed on firms.