UK Finance’s Annual Fraud Report reveals investment and purchase scams at record highs, as banks press tech and telecoms firms to share the fraud burden

Criminals stole £1.28bn ($1.72bn) through payment fraud in the UK last year, with fraudsters moving away from technical attacks in favour of targeting people directly.

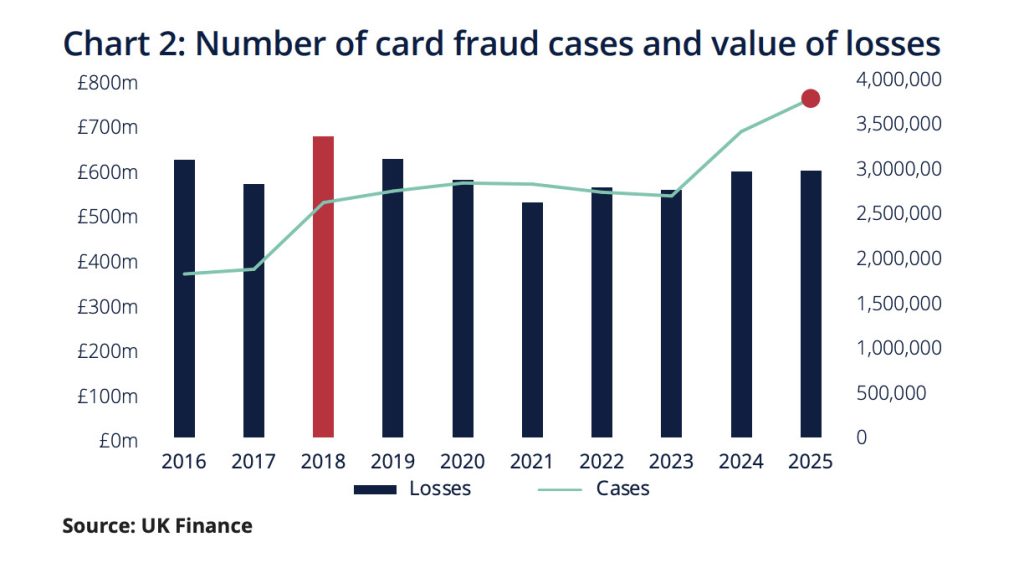

The figures, from UK Finance’s Annual Fraud Report 2026, cover both authorised and unauthorised fraud in 2025, with the figure a 4% rise year-on-year. Confirmed fraud cases climbed 11% to a record 4.06 million.

On average, eight people were defrauded every minute, losing almost £2,500 between them in that time. The industry prevented a further £1.68bn, equivalent to 70p in every £1 of attempted fraud.

Unauthorised losses – chiefly card fraud – fell 5% to £703.4m even as cases rose, highlighting a high-volume, low-value model in which criminals target far more victims for smaller sums. Authorised push payment (APP) fraud moved the other way, with losses up 19% to £576.4m.

The findings mirror those from Visa’s spring bi-annual Threat Report, which increasingly found fraud fraudsters were targeting individuals in widespread scam activity.

Investment scams drive the surge

Much like Visa, UK Finance found fraud concentrated in “malicious payee” activity – scams in which victims knowingly pay a correctly identified recipient who then absconds.

Purchase, investment, romance and advance fee scams each hit record loss totals, rising 35% collectively to £437m.

Investment fraud was the single largest driver, up 40% to £221.5m and accounting for 38% of all APP losses. Purchase scams remained the most common, making up 71% of cases.

Less remarked upon was advance fee fraud, where losses jumped 65% to £58.4m – driven, UK Finance says, by criminals taking deposits for high-value goods and holiday rentals that do not exist.

By contrast, “malicious redirection” scams fell. This included invoice and mandate, CEO and impersonation fraud, which dropped to multi-year lows, with the category now under a quarter of APP losses, down from more than half in 2020.

“Banks are winning the fight against traditional fraud, but criminals have adapted, shifting from hacking systems to manipulating people,” said Jonathan Frost, Global Advisory Director at BioCatch.

“Mandatory reimbursement may soften the impact for victims, but it cannot be mistaken for a fraud prevention strategy. Criminals continue to profit, losses continue to rise, and banks are increasingly carrying the cost. The forthcoming independent review must therefore ask a fundamental question: is the regime stopping fraud, or merely reallocating the losses once the damage is done?”

Banks press for shared responsibility

UK Finance used the report to renew calls for tech and telecoms firms to shoulder more of the burden, pointing to data showing 66% of APP cases originate online and a further 17% through telecommunications.

Ruth Ray, Managing Director of Economic Crime at UK Finance, said the sector “cannot be the only line of defence”.

She added: “Given most APP fraud still starts via online tech platforms or via telecoms, we urgently need stronger, enforceable responsibilities to be placed on these sectors.”

The body wants Ofcom to impose tougher, proactive fraud-prevention duties on high-risk platforms through the Online Safety Act, mandatory seller verification on online marketplaces, and a financial contribution from tech and telecoms firms towards prevention.

Reimbursement ‘not stopping the fraud’

Banks reimbursed £354.3m to APP victims in 2025, around 61% of losses, with the Payment Systems Regulator reporting that 89% of in-scope fraud was refunded in the first 15 months of its mandatory rules.

UK Finance argued that reimbursement, while important, does not address the root problem, as stolen funds still flow to organised crime, which it casts as a national security threat.

Kamlesh Harry, Principal Strategic Advisor for Nasdaq Verafin, warned that criminals are “exploiting advances like AI to industrialise operations” and called for a “technology-led and joined up” response built on data sharing and shared accountability.

For now, while the report shows prevention is outpacing criminal gains, the people behind the fraud are working harder and getting more persuasive.