Real‑time payments promise instant access to funds, but the speed that makes them so attractive also creates new risks and infrastructure demands for businesses.

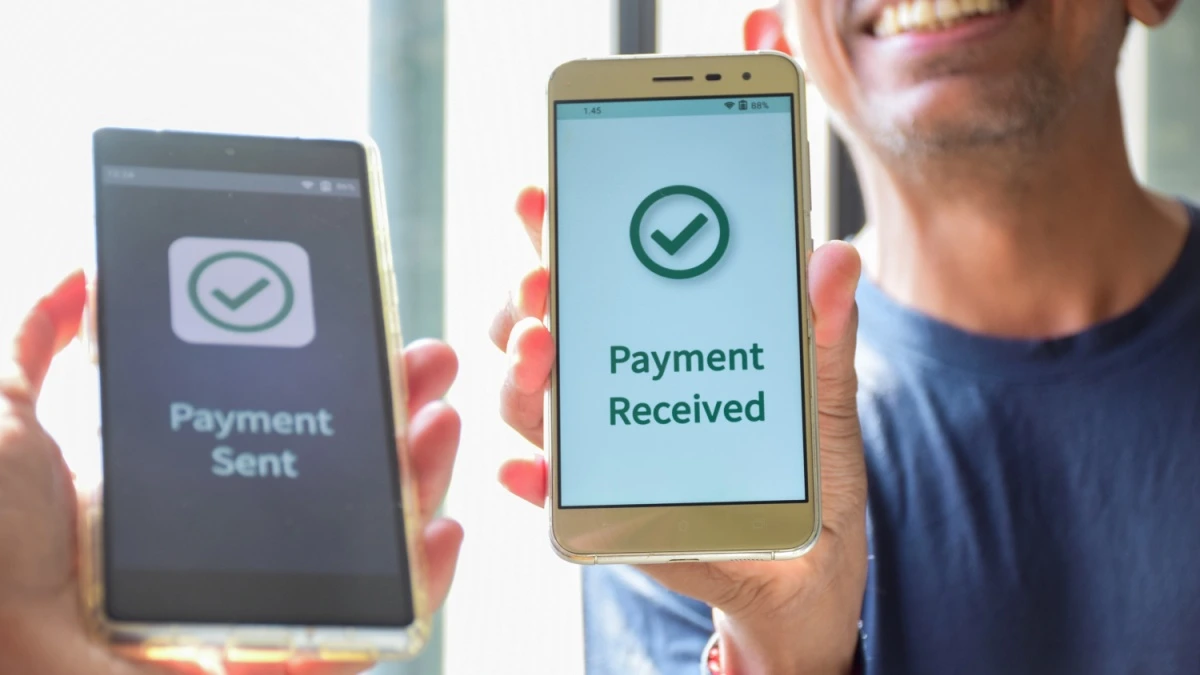

Gone are the days when businesses had to wait several days for payments to clear before gaining access to their funds. This is thanks to real-time payments, which enable money to move between accounts within seconds.

While this speed is a significant upside for businesses, real-time payments can also introduce operational and risk-management challenges.

What are real-time payments?

Real-time payments are electronic payments that are processed, cleared and settled almost instantly.

Unlike traditional payment systems, which may take hours or days to complete, real-time payment networks aim to transfer funds between accounts within seconds.

These systems can operate 24 hours a day, seven days a week, allowing businesses to send and receive payments outside normal banking hours.

Real-time payments today are being used for supplier payments, payroll, insurance payouts, refunds, marketplace disbursements and other transactions where speed is the top priority.

Opportunities for businesses

One of the biggest advantages of real-time payments is improved cash flow visibility. Businesses receive immediate confirmation when funds arrive, making it easier to oversee balances and manage capital.

Faster access to funds can also reduce delays across supply chains. Suppliers can be paid more quickly, while businesses receiving payments no longer need to wait several days for settlement before accessing money that has already been sent.

Customer experience is also likely to improve, with faster refunds, claims payments and disbursements helping to reduce waiting times and better align with modern expectations around payment speed.

Another benefit is the potential reduction in payment costs. Account-to-account real-time payments do not rely on traditional card networks such as Visa and Mastercard, which can reduce interchange and processing fees for merchants.

The challenges of working at speed

Speed is the defining characteristic of real-time payments and the biggest motivator for businesses adopting them, but it is also the source of many challenges.

The greatest challenge of real-time payments is fraud because the faster the payment, the shorter the window to detect suspicious activity before funds leave an account.

Fraud controls built around delayed settlement can be less effective in real-time environments, forcing payment providers and financial institutions to make risk decisions within seconds.

Many real-time payments are also irrevocable, meaning that once money has been sent, recovering it can be difficult.

The speed and availability of these systems also rely on modern payment infrastructure. While traditional payment processes had business hours and batch processing in mind, real-time payments require systems capable of operating all the time.

Integration can present additional challenges, with businesses potentially needing to update treasury, accounting and enterprise resource planning systems to support real-time processing and reconciliation.

Real-time payments are still being developed

Real-time payments may feel established, but regulators and financial institutions are still working to improve how they work.

In Europe, the EU Instant Payments Regulation, passed in 2024, requires banks to offer SEPA Instant transfers at the same price as standard ones, helping to accelerate adoption across the region and making instant payments more accessible.

In the US, adoption of the Federal Reserve’s FedNow service is on the rise, while Brazil’s Pix has set the global benchmark, processing more than five billion instant transactions a month.

Fraud controls are also being rebuilt for real-time environments, with the UK’s Confirmation of Payee system, now mandatory for major banks, becoming a core defence against authorised push payment fraud.

Singapore has taken a different route to combat fraud, mandating “money lock” accounts and real-time scam filters across its FAST payment system to stop funds from being moved before checks are completed.

Open banking is also helping to expand real-time payment capabilities, as in the UK, providers are enabling merchants to embed instant account-to-account payments into checkout flows.