From the US–Mexico corridor to Pix and stablecoins, how money moves across Latin America’s borders – and the fintechs rebuilding the rails

Latin America runs on money that crosses borders from across the globe. Cross-border payments in the form of remittances to the region reached around $174.4bn in 2025, according to the Inter-American Development Bank (IDB) – up $11.7bn on 2024 and marking 16 consecutive years of growth.

For several economies, these flows are a structural part of economic stability. Banco de México (Banxico) data shows Mexico received $61.79bn in remittances in 2025, while in Guatemala, Honduras and El Salvador the flows account for a far larger share of national income. Add a fast-growing B2B cross-border market – marketplaces, payroll, supplier payments – and the region has become one of the most closely watched testbeds for payments innovation anywhere.

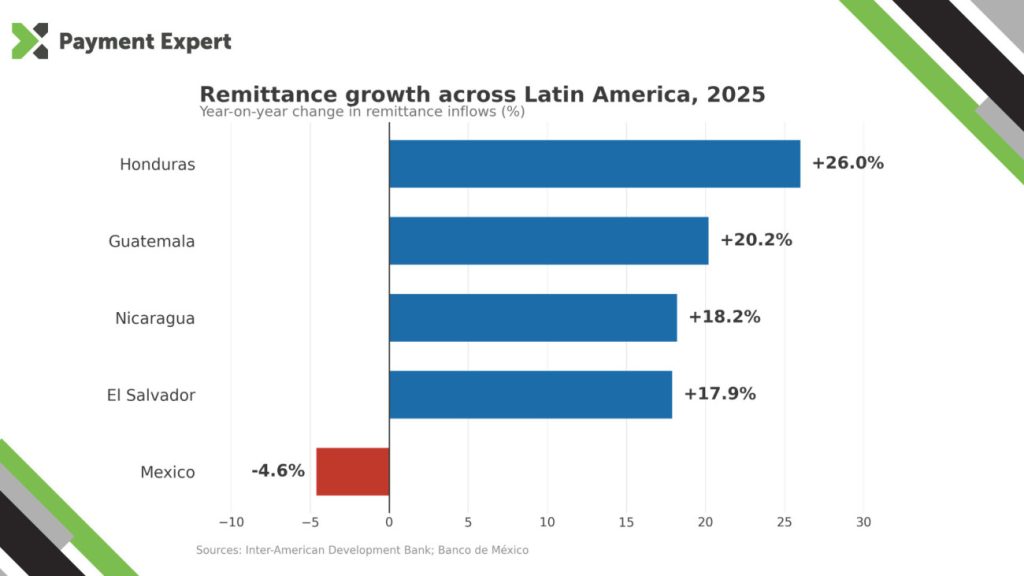

The most significant payment corridors for LatAm

The US–Mexico route is the largest remittance corridor in the world, but it is in transition. Banxico’s figures show Mexico’s 2025 total fell 4.6% from the $64.75bn recorded in 2024 – the first annual decline after more than a decade of growth – against a backdrop of tighter US immigration enforcement.

A new cost has arrived too: from 1 January 2026, the US applies a 1% excise tax on remittances funded with cash, money orders or cashier’s checks, per the US Internal Revenue Service.

The US dominates flows across the region. According to the IDB, it accounts for 73.5% of transfers to Central America and 96% of those to Mexico. And while Mexico dipped, Central America surged: the IDB estimates the subregion received around $55.4bn in 2025, up 20.4%, with Honduras (+26.0%), Guatemala (+20.2%), Nicaragua (+18.2%) and El Salvador (+17.9%) posting the largest increases.

How remittances actually move

A typical remittance involves a sender paying a money transfer operator, bank or fintech app in the origin country; the provider settles across borders through correspondent banking or pre-funded local accounts; and a payout partner delivers local currency via bank deposit, wallet or cash pickup.

Cash still matters more in LatAm than the industry sometimes admits. Banxico reports that 99.1% of remittances to Mexico in 2025 were sent electronically – yet 49.6% of those electronic transfers, worth $30.33bn, were collected in cash at the receiving end, reflecting persistent gaps in banking access.

Remittance costs in the region are down, but unevenly so. Research from the Inter-American Dialogue puts the unweighted average cost of sending to the region at 3.67%, dropping to around 3% across the most commonly used methods, and below 2.4% in effective terms for senders remitting more than $300 – well under global averages, but still meaningful money on corridors measured in tens of billions.

Fintech and the new rails

Two forces are remaking the plumbing. The first is domestic instant payments going international.

Brazil’s Pix is the standout: Central Bank of Brazil data shows the system processed 5.4 billion transactions worth BRL1.7tn ($329bn) in September 2025 alone, and research published by payments firm EBANX found Pix had processed 196.2 billion transactions worth $16tn between its 2020 launch and September 2025.

Mexico’s SPEI plays a similar role as the real-time payout leg for cross-border providers, and connecting these domestic schemes across borders is now a stated ambition of the region’s central banks.

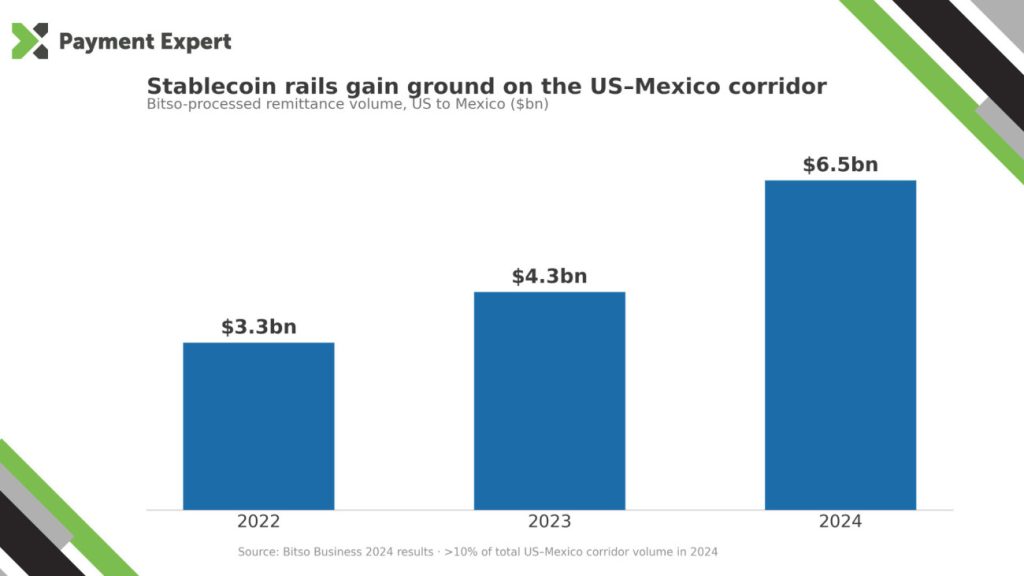

The second is stablecoins. Bitso reports that it processed more than $6.5bn in remittances on the US–Mexico corridor in 2024 – over 10% of total volume between the two countries.

The appeal is the structure this provides, because dollar-backed tokens settle around the clock, this strips out the pre-funding capital and settlement float that correspondent rails require. The IDB has noted that stablecoins are now showing up in household remittances, not just crypto-native flows – a signal that the technology has crossed into the mainstream of the region’s payments story.