Two of the most frequently cited trends in modern payments are often conflated. While both are reshaping how financial services are delivered, embedded finance and open banking operate on fundamentally different models, infrastructures and regulatory foundations.

In payments discourse, few terms have travelled as quickly, or as loosely, as embedded finance and open banking.

Both sit at the centre of how financial services are evolving beyond traditional banking channels. Both promise to reduce friction, expand access and reshape the relationship between consumers, businesses and financial institutions. Yet despite often being referenced in the same breath, they are not interchangeable.

Understanding where one ends and the other begins has become increasingly important for payment professionals navigating product strategy, regulation and commercial partnerships.

At their core, the distinction is relatively straightforward: open banking is an access framework while embedded finance is a delivery model. The complexity emerges in how the two increasingly intersect.

Embedded finance: Financial services within the user journey

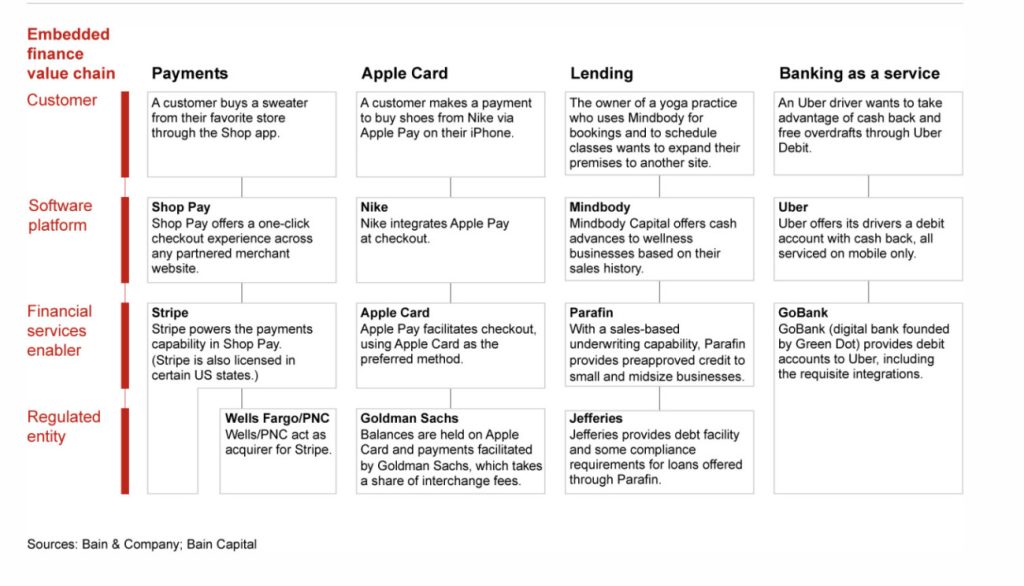

Embedded finance refers to the integration of financial services directly into non-financial platforms.

Rather than requiring a customer to engage with a bank or financial provider separately, services such as payments, lending or insurance are built into the existing user experience. The financial layer becomes part of the product itself, often invisible to the end user.

This model has gained traction across e-commerce, mobility and digital platforms. Shopify, for example, offers merchants access to payments, lending and balance accounts within its ecosystem. Uber enables drivers to receive earnings instantly through in-app wallets. Infrastructure providers such as Stripe have positioned themselves at the centre of this shift, enabling businesses to embed financial functionality without becoming regulated entities themselves.

According to research from Bain & Company, embedded finance accounted for $2.6 trillion in US transaction value in 2021, representing nearly 5% of all financial transactions. By 2026, that figure is expected to exceed $7 trillion, crossing the 10% threshold. Payments and lending remain the dominant use cases, but the model is expanding into adjacent services including insurance, tax and accounting.

Bain also estimates that revenues generated by platforms and enablers across embedded payments, lending and banking will more than double from $22 billion in 2021 to $51 billion by 2026, reflecting both increased transaction volume and deeper integration across vertical software platforms.

This growth is underpinned by what Bain describes as a “better together” proposition. By embedding financial services into existing workflows, platforms are able to streamline onboarding, reduce reliance on third-party providers and use proprietary data to improve access to credit and other services. For end users, the appeal is largely experiential: financial services are accessed as a by-product of activity, rather than as a separate destination.

The underlying model is typically powered by banking-as-a-service (BaaS) providers, which handle the regulatory and operational complexity behind the scenes. For the end user, however, the experience remains anchored to the platform they are already using.

Open banking: Regulated access to financial infrastructure

Open banking refers to the regulated sharing of financial data between institutions and third-party providers via APIs, enabling new payment flows and services to emerge outside traditional banking channels.

At its core, the model allows licensed providers to initiate payments or access account data directly from a user’s bank, reducing reliance on card networks and reshaping how transactions are routed. In markets such as the UK and parts of Europe, this has been driven by regulatory frameworks designed to increase competition and innovation in financial services.

According to data from the Cambridge Centre for Alternative Finance, open banking payments have surpassed hundreds of billions in annual transaction value globally, with adoption accelerating across both consumer and business use cases. In the UK alone, millions of users now engage with open banking-enabled services, spanning everything from personal finance tools to account-to-account (A2A) payments at checkout.

The model’s momentum is closely tied to the rise of pay-by-bank propositions, which allow merchants to accept payments directly from a customer’s bank account. These flows are typically positioned around lower costs, faster settlement times and reduced reliance on intermediaries, particularly in sectors with high transaction volumes or thin margins.

Beyond payments, open banking is also enabling new forms of financial access. Lenders, for example, are increasingly using real-time account data to inform credit decisions, while businesses are embedding account verification and reconciliation tools directly into their platforms.

However, adoption remains uneven across regions and use cases. While markets such as the UK have benefited from regulatory mandates and centralised frameworks, others continue to rely on more fragmented, commercially driven models. Questions also persist around monetisation, liability and user experience, particularly as open banking begins to intersect with broader developments in real-time payments and digital identity.

As the model evolves, the distinction between open banking and wider open finance initiatives is becoming less clear. The same infrastructure that enables payments and account aggregation is increasingly being extended to cover savings, investments and insurance products, pointing towards a more integrated financial ecosystem.

Different models, different incentives

The distinction between open banking and embedded finance becomes clearer when comparing how each operates across four key dimensions.

- The delivery model: Embedded finance is front-end focused, integrating services directly into customer journeys. Open banking operates in the background, enabling connectivity between institutions.

- Regulation: Open banking is explicitly governed, with strict requirements around licensing, consent and data access. Embedded finance typically relies on regulated partners, allowing platforms to offer financial services without holding licences themselves.

- Ownership of the customer relationship: Embedded finance allows platforms to retain control of the user experience and branding. Open banking maintains the bank as a central component of the financial relationship, even when accessed through third parties.

- Monetisation: Embedded finance is often positioned as a revenue driver, whether through lending margins, interchange or increased platform stickiness. Open banking, particularly in payments, has been framed as a cost-efficient alternative to card networks, especially through account-to-account transactions.

Despite these differences, the two are increasingly overlapping.

Open banking infrastructure is frequently used within embedded finance propositions. A pay-by-bank option at checkout, for example, may appear as a seamless part of an e-commerce flow, even though it relies on open banking APIs in the background. For the end user, the distinction is largely invisible. What appears as an embedded payment method may in fact be powered by open banking rails.

This convergence has contributed to the confusion between the two concepts, but also highlights how they can operate as complementary layers rather than competing models.

Regional approaches

The relationship between embedded finance and open banking also varies significantly by geography.

In the UK and Europe, open banking adoption has been shaped by regulatory mandates. This has created a relatively mature ecosystem of licensed providers and standardised APIs, which embedded finance players can build on top of.

In the US, the absence of a PSD2-style framework has resulted in a more market-driven approach. Open banking has developed through aggregators such as Plaid, while embedded finance has expanded rapidly through partnerships between fintechs and sponsor banks.

In Asia-Pacific markets, the picture is more fragmented. However, the dominance of super apps has led to strong adoption of embedded finance, often with less emphasis on formal open banking frameworks.

Use cases across industries

The practical applications of both models can be seen across a range of sectors.

In e-commerce, embedded finance underpins integrated payments, wallets and merchant lending, while open banking supports pay-by-bank options aimed at reducing transaction costs.

In high-risk sectors such as iGaming, embedded wallets and instant withdrawals are increasingly common, alongside open banking tools used for affordability checks and direct account payments.

For SMEs and platform-based businesses, embedded finance can provide access to working capital and expense management tools, while open banking enables visibility into cash flow and financial data aggregation.