Open banking is reshaping how payments and financial data move between institutions, but its impact varies widely between consumers and businesses. This guide breaks down what it is, how it works in practice, and where adoption is heading globally.

A customer reaches the final stage of an online purchase. Instead of entering card details, they select a “Pay by Bank” option. Within seconds, they are redirected to their banking app, authenticate the payment, and return to the merchant site with confirmation.

Not long ago, that same transaction would have required manual card entry, routing through multiple intermediaries, and settlement delays that left the merchant waiting days for funds to arrive.

This change, from card-based processing to direct account-to-account payments, is one of the most visible outcomes of open banking.

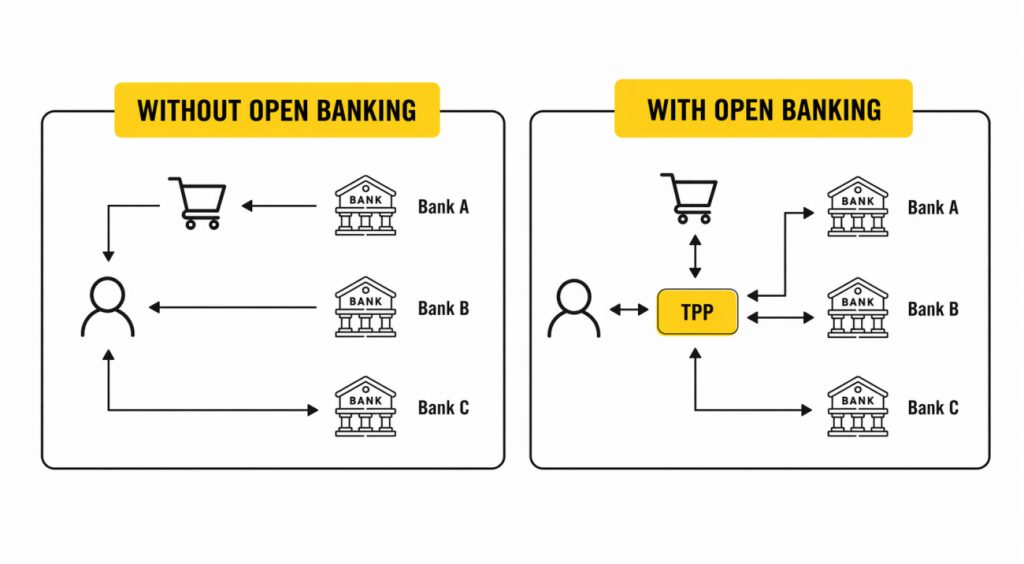

At its core, open banking enables banks to share customer financial data securely with authorised third parties, allowing new services to be built on top of traditional banking systems. While the concept is often discussed in broad terms, its practical impact differs significantly depending on who is using it.

For consumers, it is largely about convenience and visibility; whereas for businesses, it is increasingly about cost, speed, and control over payments.

What is open banking?

Open banking refers to a framework which allows regulated third-party providers to access bank account data or initiate payments on behalf of a user, typically through application programming interfaces (APIs).

In simple terms, APIs act as secure connectors between banks and external services, enabling information to be shared or transactions to be triggered without exposing sensitive credentials.

There are two core components:

- Account information services, which allow third parties to view financial data such as balances and transaction history

- Payment initiation services, which enable payments to be made directly from a bank account, often referred to as Pay by Bank

These capabilities form the basis of most open banking use cases seen today.

How open banking works in practice

Although implementations vary, the typical open banking journey follows a similar structure.

A user selects an open banking option, such as paying directly from their bank account at checkout or connecting their account to a financial app. They are then redirected to their bank’s authentication environment, where they approve the request.

Once authorised, the bank either shares the requested data or executes the payment, with the third-party provider acting as the intermediary.

The ecosystem is built around three main participants: banks, which hold the data and accounts; third-party providers, which deliver services; and regulators, which define the rules governing access.

Consumer use cases: Convenience and control

For consumers, open banking has primarily been positioned as a way to simplify financial management. One of the most visible applications is account aggregation, where apps bring together multiple bank accounts into a single dashboard. This provides users with a clearer view of their finances without needing to log into multiple platforms.

Open banking is also increasingly used at checkout. Pay by Bank options allow users to bypass card networks and authorise payments directly through their banking app, often with fewer steps and immediate confirmation.

In lending, access to real-time financial data has enabled more tailored credit assessments, particularly for consumers with limited credit histories.

Business use cases: Efficiency and conversion

For businesses, the incentives behind open banking adoption are more commercial.

Payment initiation services offer an alternative to card payments, reducing reliance on interchange fees and improving margins. For merchants, particularly in sectors with high transaction volumes, this can have a measurable impact on costs.

Settlement speed is another advantage. Payments initiated through open banking can be processed in near real time, improving cash flow and reducing reconciliation delays.

Open banking data is also being used to streamline onboarding and risk assessment. By accessing verified financial information directly from a bank, businesses can enhance KYC processes and make faster lending decisions.

In this context, open banking is less about user experience alone and more about operational efficiency and financial optimisation.

Consumers vs businesses: Where the value differs

While the underlying technology is the same, the way open banking delivers value differs between user groups.

For consumers, the focus is on usability and transparency. Tools that simplify budgeting, enable faster payments, or improve access to credit tend to drive adoption.

For businesses, the emphasis shifts to economics and infrastructure. Lower payment costs, faster settlement, and better data for decision-making are the primary drivers.

This divergence explains why certain use cases, such as pay-by-bank, are being pushed heavily by merchants, while others, like aggregation apps, have been led by consumer demand.

UK, Europe and beyond

Open banking adoption has not been uniform globally, with regional frameworks shaping how the ecosystem has developed.

In the UK, regulatory intervention through the Competition and Markets Authority created one of the most structured open banking environments. Standardised APIs and mandated bank participation have supported the growth of both data-sharing and payment initiation services.

Across the European Union, the revised Payment Services Directive, PSD2, established the legal basis for open banking. However, implementation has been more fragmented, with varying levels of bank readiness and user adoption across member states.

In the US, open banking has largely evolved through market-driven initiatives rather than a single regulatory mandate. This has resulted in a more decentralised ecosystem, with a mix of bilateral agreements and emerging standards.

Elsewhere, markets such as Brazil have taken a more expansive approach, integrating open banking into broader real-time payment systems and driving adoption through national infrastructure.

Adoption challenges and limitations

Despite its progress, open banking continues to face structural challenges.

Fragmentation remains a key issue, particularly in regions without consistent technical standards. Differences in API quality and bank participation can create uneven user experiences.

Awareness is another barrier. While industry adoption has grown, many consumers remain unfamiliar with how open banking works or where it is being used.

Commercial incentives also play a role. For some banks, the costs of enabling open access have not been matched by clear revenue opportunities, which can slow development.