Embedded finance integrates financial elements – such as payments, lending, banking and insurance – for non-financial businesses to then provide these services to their customers.

Embedded finance services have become extremely popular to businesses as they allow customers to stay on their platform – whether that be websites or mobile apps – without having to leave to complete a transaction.

People often confuse embedded finance with banking-as-a-service (BaaS) and open banking, but it carries many distinct functions and processes in different ways.

There are traditionally three key players in the embedded finance process: the business, the provider and the license holder.

The business is the entity that interacts with the customer, the provider – usually a banking-as-a-service (BaaS) company or fintech firm – interacts with the business to provide the financial infrastructure, and the license holder – usually a regulated traditional finance entity – interacts with the provider and business to ensure the financial service is compliant with regulatory requirements.

Embedded finance origins and how it works?

The origins of embedded finance can be traced back to the 1920s when car manufacturer Ford issued a Ford Credit, a lending program developed in-house to provide car financing to customers without the need to secure a loan from a bank.

By removing an intermediary like a traditional bank, Ford enabled the customer journey to remain entirely in-house, embedding the lending process before the transaction can be performed and settled.

The arrival of the internet and the digitisation of payments transformed embedded finance through the integration of Application Programming Interfaces (APIs).

Under the current application of embedded finance via the use of APIs, this connects non-financial or payment businesses to providers of digital infrastructure which then integrates, or embeds, the providers’ payment methods.

Not only does the business integrate the payment methods, or lending, banking, insurance, it also onboards the providers’ regulatory licences in order for the business to remain compliant to the varying regulations per country/region.

This can be fully embedded into the businesses’ website or app without the customer having to onboard a third-party to complete a transaction.

Embedded finance has been praised for benefitting customers by providing a frictionless user experience with the removal of consumer-facing intermediaries. It has also been a benefit for financial inclusion among customers, as well as personalising the user experience as businesses can tailor rewards and services to the customer’s preferences.

For businesses, the benefits of embedded finance have been shown to boost revenue through embedded lending services by earning commission, as well as gaining greater customer insights and building better customer retention.

What are some of the most high-profile use cases?

Uber – Stripe, Mastercard, Marqeta

Uber is one of the primary examples of a non-financial company transforming their infrastructure to not only support payments, but now issue its own cards.

Uber integrates Stripe’s banking-as-a-service (BaaS) service called Stripe Treasury. Stripe Connect enables Uber customers to make in-app payments when selecting their taxi service.

For Uber Eats, the company integrates Pipe which provides restaurants with working capital directly within the Uber Eats dashboard. Customer funds to a restaurant’s bank account are settled within 24 hours and are not subject to hard credit checks. Merchants can repay cash advances via an agreed-upon percentage of future Uber Eats sales.

For the Uber Pro Card, the company embeds Branch’s embedded banking platform to power checking accounts for drivers and couriers, co-developed alongside Mastercard and Marqeta.

Branch provides processing applications for business accounts, while Mastercard connects the Uber Pro Card to millions across its network, while Marqeta serves as the card issuing service that connects payments to the drivers’ Uber Driver app.

The most recent development saw Uber partner with BaaS provider Griffin to embed its underlying banking services for the Uber Pro Card for drivers to earn cashback on fuel and EV charging for trips. The service has already been available for US drivers, and is rolling out across Europe in 2026.

Amazon – Adyen, Klarna, Green Dot Bank

E-commerce giant Amazon is a melting pot of embedded finance services.

Amazon integrates Adyen and Stripe’s embedded payments services to process payments directly from the Amazon checkout page. Adyen consolidates payments made via Amazon Pay, while Stripe processes local payment methods for customers in global markets.

For Amazon’s banking services, it works with Green Dot Bank as its issuer for the Amazon Flex debit card. The card is primarily used for Amazon delivery drivers which offers cashback on gas fees and instant payouts.

Amazon also provides buy-now-pay-later (BNPL) options via providers Klarna and Affirm, enabling customers to pay in instalments, often over three tiered payments, to offer flexibility.

On lending, Amazon also embeds YouLend’s financing scheme to provide UK e-commerce businesses with up to £2m in advances to implement additional capital.

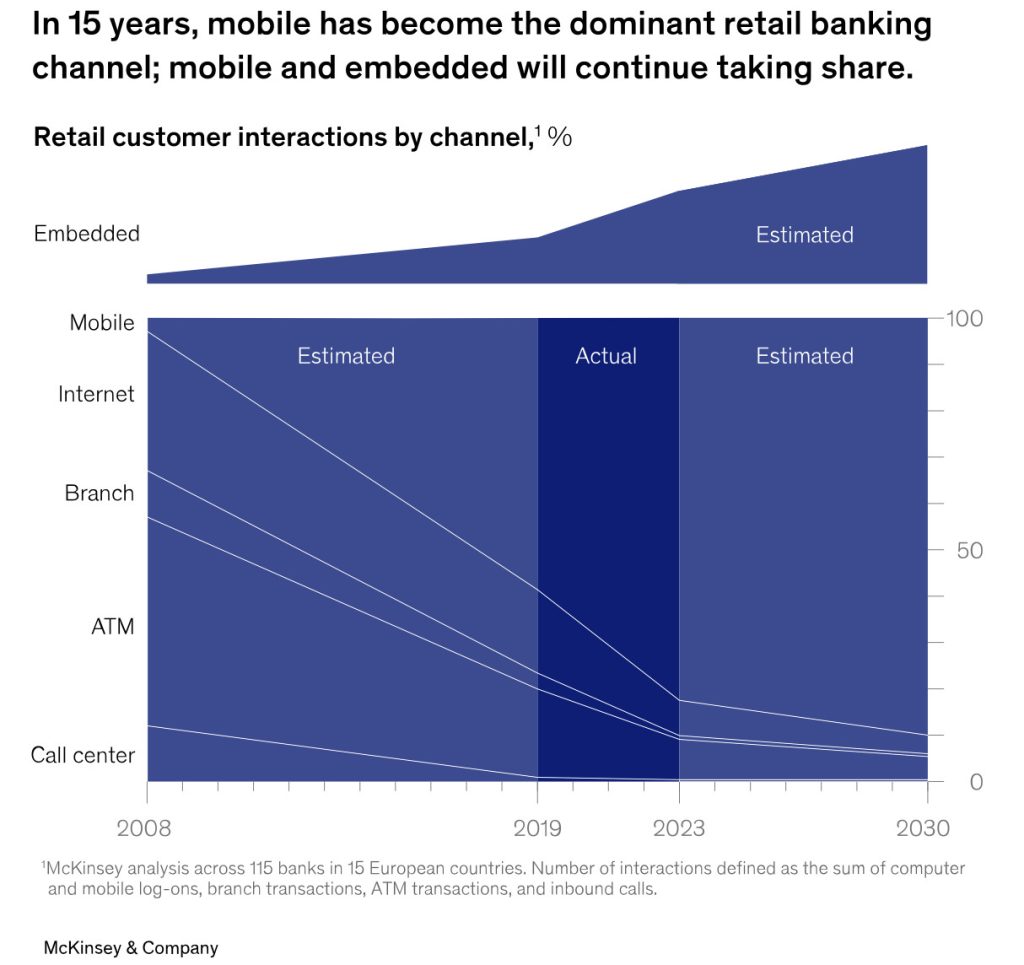

How valuable is embedded finance to firms?

With more and more non-financial businesses looking to reduce the barriers for seamless customer services, the embedded finance market has surged in value.

A McKinsey report revealed the global embedded finance market is projected to be worth upwards of $116bn by 2030.

The European market is also helping to drive that value. Businesses generated an estimated €20bn-€30bn in 2023 and is expected to increase further to €100bn by the end of the decade.

McKinsey found that embedded finance loans performed on non-financial platforms grew three times as fast as traditional loans coming directly from banks. The report expects credit volumes to migrate to embedded lending.

A report from JP Morgan found that embedded payments, besides adding revenue, is benefitting businesses by helping to reduce customer churn and boost customer acquisition.