The EBA finds more EU banks falling short of 100% USD NSFR as foreign-currency funding climbs, led by unsecured wholesale and repos. Payments firms face higher liquidity sensitivity across USD settlement and FX corridors.

EU banks increased their use of foreign-currency funding in 2024, with the dollar now the clear driver, according to a new European Banking Authority report.

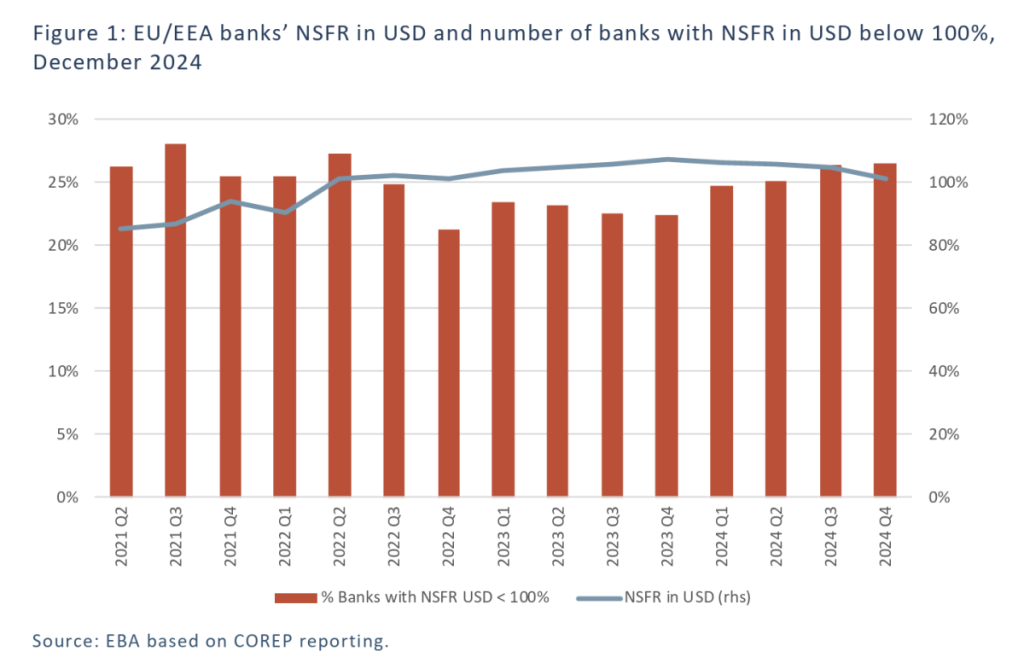

According to the regulator’s findings, while the sector remains well-funded in aggregate, more lenders are falling short of the 100% threshold in their dollar net stable funding ratio (NSFR).

On a total basis, EU/EEA banks reported a weighted-average NSFR of 127.6% at end-December 2024, little changed from a year earlier. By currency, the picture is tighter: the USD NSFR stood at 101%, down from 107% in December 2023. The share of banks below 100% in dollars rose to 27% of those that report USD as a significant currency; in sterling, 41% of reporting banks were below 100%.

The EBA notes that banks in Germany, France, Italy, the Netherlands and Portugal continue to show an average USD NSFR below 100%.

Banks’ reliance on foreign-currency liabilities also edged higher. On a consolidated view, 25.2% of total funding is in foreign currencies, up from 24.1% a year earlier. Within that, USD accounts for 16.9% of all funding, GBP 2.3%, and other foreign currencies 5.9%. The EBA attributes the annual rise mainly to higher dollar funding.

At individual-entity (solo) level, the foreign-currency share is lower: 21.1% of funding is in FX, including 13.1% in USD. The EBA highlights that consolidated figures can overstate FX use at group level because subsidiaries’ local-currency funding may appear “foreign” when rolled up to the parent.

The mix of where FX funding comes from also matters. Unsecured wholesale is the largest single source of bank funding overall and makes up roughly half of all FX funding. Within USD specifically, the composition shifted over the year towards securities financing transactions (repos/SFTs) and other liabilities, while unsecured wholesale remained the biggest bucket.

On the asset side, foreign-currency exposures are larger than FX funding. On a consolidated basis, 35.7% of exposures that require stable funding are in foreign currencies (up from 31.7% in 2023). In USD, the largest exposure buckets are derivatives (49.9% USD-denominated), off-balance sheet items (25.4%) and loans (24.4%), with the dollar share of derivatives rising the most over the year.

The report also flagged that country patterns are uneven. Above-average foreign-currency funding shares at the individual-entity level include Liechtenstein (57%), Finland (51%), Bulgaria (39%), Sweden (33%), Ireland (29%), Hungary (29%), Norway (28%), Luxembourg (27%), Spain (24%) and Denmark (24%).

Germany and France stand out for higher reliance on “other” non-EEA foreign-currency funding.