Swift is upgrading its cross‑border infrastructure as newer alternative payment networks are influencing expectations around speed, transparency and user experience.

Deutsche Bank is changing the experience of receiving money from overseas as it goes live on Swift’s new cross‑border payments framework.

The bank announced on 24 June it has processed inbound transfers from Australia and Brazil in under a minute on Swift’s new framework, which aims to make cross‑border payments faster and more transparent.

Deutsche Bank is the first institution in Germany to adopt the framework, initially supporting transfers from Brazil, Australia and Turkey.

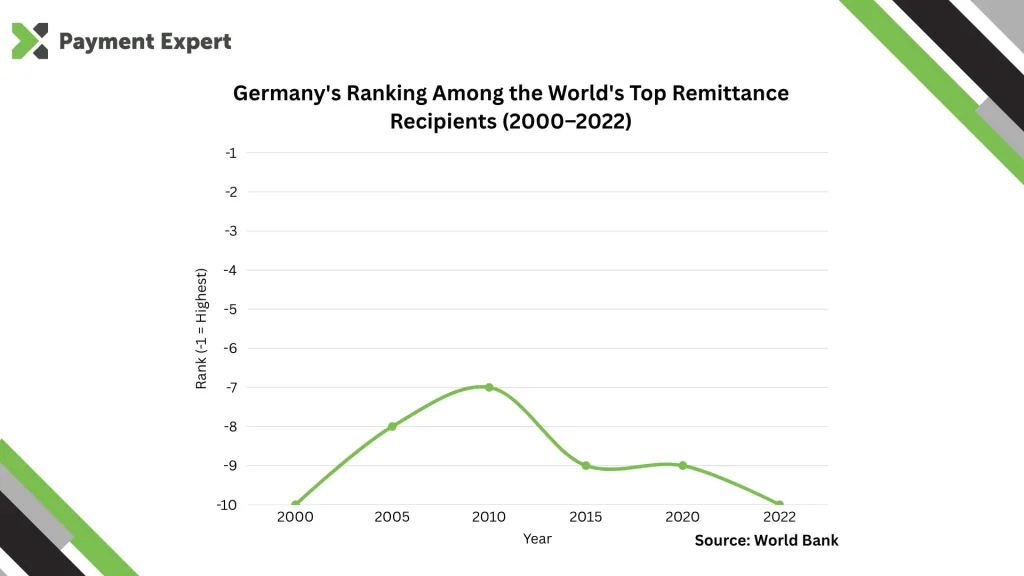

Germany’s inclusion is a significant milestone for Swift, given the country’s consistent position in the UN’s top‑ten remittance recipients and its role as a major European hub for inbound flows.

“Given the importance of the German market in global cross‑border flows, it was critical to enable a scalable and standardised framework for incoming payments,” said Ciaran Byrne, Global Product & Client Solutions Head, Institutional Cash Management at Deutsche Bank.

“As a Gateway Intermediary, Deutsche Bank is supporting financial institutions globally in sending payments into Germany, while enabling retail and SME clients to benefit from a more transparent, predictable and efficient payment experience.”

Swift’s new framework and why banks are in support

More than 60 banks worldwide support Swift’s new retail payments framework, including Lloyds Bank, JPMorgan Chase and Commonwealth Bank of Australia. While not all have gone live, they have publicly backed the initiative.

“Customers expect international payments to be as transparent and predictable as those made domestically and these standards help deliver on those expectations,” said Olivier Lens, Head of Central and Eastern Europe at Swift.

“This framework will enable a more trusted cross-border payments experience for businesses and consumers alike.”

The framework was launched in March 2026, following Swift’s 2025 announcement that it would improve the cross‑border experience in line with the G20’s targets for speed, cost and predictability.

Corridors into Australia, Bangladesh, Canada, China, Germany, India, Pakistan, Spain, Thailand, the UK and the US are all covered. These markets include Bangladesh, China, Germany, Pakistan and India, five of the world’s top ten remittance destinations.

Payments into these markets will land in full, with the exact amount sent arriving in the recipient’s account and no deductions taken during the process. Senders also see the fee and FX rate at the start of the journey.

The majority of transfers aim to arrive within minutes, and where domestic systems support it, settlement can be instant. Every payment can also be tracked end‑to‑end, which is a feature that has become standard for domestic payments but is rare across borders.

Speaking about the new framework in March, Kim Verhaaf, Managing Director for Payments at Lloyds Bank, said the bank’s involvement was about the need for greater transparency.

“Efficient cross‑border payments are a critical enabler of trade, growth and everyday economic activity for businesses and consumers alike,” said Verhaaf. “By joining the new Swift framework, we’re helping to deliver an enhanced experience for customers, offering better transparency and speed in their international payments.”

Competition in cross-border payments

Swift is still the main network for international bank‑to‑bank transfers and its sheer size and integration make it difficult for any challenger to take its top spot, although there is competition.

Wise has built a global footprint by matching transfers locally rather than routing them through correspondent chains, offering predictable fees and faster delivery for consumers and SMEs.

Airwallex has taken a similar approach for businesses operating across borders, routing payments over local rails to avoid traditional wire costs. Ripple continues to push an alternative settlement model that removes the need for pre‑funded accounts, while China’s CIPS network is expanding as a renminbi‑focused clearing system with growing geopolitical backing.

Despite none of these networks matching Swift’s reach, their different approaches have influenced user expectations around speed, transparency and user experience, causing Swift to upgrade its framework.