Payment Expert is on the ground live from Money 20/20 Asia 2026 (21-23 April) in Bangkok, Thailand, from the Queen Sirikit National Convention Centre.

Expect real-time insights from some of the leading industry leaders engaging in conversations around fintech, payments, banking, digital currencies and much more.

17:00 – That brings an end to Payment Expert‘s coverage of Day 1 of Money 20/20 Asia.

There has been a range of discussions and opinions on best practices for tokenisation, solving cross-border payments issues in Asia, as well as breaking news from dLocal, Trulioo and EBANX.

Stay tuned for more real-time opinions, discussions and themes being brought out of Money 20/20 Asia Day 2 tomorrow.

16:45 – Cross-border friction: Does blockchain hold the cure?

Is blockchain and distributed ledger technology (DLT) the answer to cross-border payments’ friction problems?

Kaiwan Turel, Director of Treasury Solutions at HSBC, admits the global bank is “very bullish” on the potential of these emerging technologies’ ability to provide 24/7, real-time settlements across borders.

Turel pointed to tokenised deposits as a solution, revealing HSBC has settled tokenised deposits in five different locations which he said “is not by mistake, but by design”. “We believe this is the wave of the future”, added Turel.

But are cross-border payments in the current day really hampered by friction if a majority of global companies continue to use the same traditional payment rails and schemes?

Devedra Verma, Business Lead for Digital Assets at Swift, admits there are friction points that need to be addressed with cross-border payments but “existing rails are not as bad as people think”.

Verma maintains the 10 minute time limit to settle cross-border payments is still somewhat sufficient, but highlighted that a market assessment of over 40 markets conducted by Swift revealed companies raised challenges around operating hours, foreign exchange, and liquidity, which, according to Verma, are “going to be here no matter what”.

On the subject of whether regulation can alleviate some of these friction points, Alvinder Singh, Head of the Innovation Acceleration Office at the Monetary Authority of Singapore (MAS), says: “Everybody can have their own blockchain, the issue is the trust ends at the banks borders, we need a wall where systems are stuck together.

“Our job is to be enablers. If we leave it alone for market success, institutions will take time to innovate. You can sit on your hands and still [keep to the status quo]. The banks have shown they can integrate DLT and blockchain across their tech stacks, to all their institutional clients, seamlessly.”

15:50 – Trulioo reveals AI-enabled improvements to Know Your Business procedures

Trulioo announced that new innovations in ultimate beneficial owner (UBO) entity resolution drove 51% year-over-year growth in Asia-Pacific (APAC) business verification volume in 2025.

These advancements in know your business (KYB) capabilities from Trulioo aim to enable organisations to achieve greater ownership visibility and scale verification more effectively across markets.

Trulioo’s latest UBO discovery to deliver clearer ownership visibility across complex markets is AI-governed and assisted with its engine, combining global data sources to resolve incomplete or inconsistent ownership information to deliver a more accurate and complete view of business ownership.

With this approach, Trulioo revealed it drove a 40% improvement in UBO coverage for one of the world’s largest social media platforms operating in APAC. Furthermore, Trulioo performed up to 98% UBO coverage in Vietnam, 70% in the Philippines (+69% uplift), and 81% in Singapore (+24% uplift), with overall coverage reaching 85% across tested markets.

Zac Cohen, Chief Product Officer at Trulioo, said: “Across APAC, the challenge isn’t just verifying businesses, it’s understanding who ultimately owns and controls them.

“With obscure and unreliable ownership data across SMEs, traditional KYB approaches simply don’t work at scale. We’ve built a fundamentally different way to solve this for our APAC customers. As a result, customers see higher onboarding acceptance rates, reduced manual review and the ability to scale into new markets with greater confidence. That’s what sets Trulioo apart as a global KYB provider.”

15:30 – “What’s the next breakthrough AI will unlock in payments over the next 12 months?”

Standard Chartered’s Craig Corte, Global Head of CIB Digital Channels, Data & Coverage Platforms, explains to Payment Expert why there will be a “significant change to the back office” when asked what will be the next great breakthrough involving AI’s impact on finance and payments.

Corte, alongside Arun Kini (Finastra – APAC Payments MD), Victor Mithouard (Mambu – Global Director for Payments Solutions), Barry O’Sullivan (OpenPayd – Chief Banking Officer), and Matt Weir (Tribe Payments – General Manager for Asia-Pacific), views will be shared on AI’s next great breakthrough soon on Payment Expert’s LinkedIn.

14:30 – What can the rest of Asia learn from Japan’s approach to tokenised money?

Tokenisation of real-world assets is increasingly being viewed as the next step in the finance world’s approach to innovation. But what about tokenisation of money and currencies?

There are many use cases being developed in the tokenisation of money, from the US’ bid to become a stablecoin safe haven, to Europe’s more regulatory-focused approach and its bid to launch the central bank digital currency (CBDC), the Digital Euro.

Japan’s approach is multi-faceted, which Mai Kaneko, Senior Manager of International Business at Decurrent DCP, explained in depth during a keynote presentation.

Kaneko revealed there is fear among banks that USD stablecoins are too dominant in their respective market, which is why tokenised deposits have become banks’ digital currency alternative. She stated this provides banks greater assurance as tokenised deposit technology is built and compliant with existing traditional infrastructures.

There are two different approaches to tokenised money, stablecoins, and tokenised deposits, said Kaneko. Japan’s approach has been a multi-bank participation strategy by bringing more than 100 participants together to build on a shared ledger to develop use cases for the tokenised money option of their preference.

“We are in the process of building an inclusive multi-bank network, with various types of banks, not only large banks, but also smaller regional and digital banks,” said Kaneko.

“We are also exploring new use cases, such as combining AI on the blockchain to perform end-to-end payment processing, including B2B payments. The various processes include invoicing, reconciliation and confirmation of payment, these are typically handled separately and include a lot of manual work. By combining AI and tokenised deposits, we achieved a 75% redaction in the proof of concept.”

14:30 – Let’s solve borderless payments

One of the best panels of the day looked at friction in cross‑border payments. The message was that the infrastructure exists domestically, but connecting it across borders is a huge challenge.

Speakers mentioned misaligned priorities, multiple payment methods and a lack of standardisation as key issues. AI was discussed as both a tool for fraud prevention and a potential source of new friction.

Stay tuned later, where this conversation will be written up in more detail as today’s panel of the day. However, for now, the takeaway from the floor is that everyone agrees the tech is there, but the problem is making it work across borders.

13:55 – dLocal enables stablecoin payouts in emerging markets

dLocal announced the launch of Stablecoin Full, a solution that enables merchants to collect, convert, and payout funds using stablecoins across high-growth economies, confirmed at Money 20/20 Asia.

Stablecoin Full seeks to enable global merchants to accept and send payments in stablecoins, fund and settle transactions in digital assets, and optimise their treasury operations in more than 44 emerging markets via a single API.

The offering is designed to leverage dLocal’s infrastructure, compliance frameworks, and reporting capabilities to provide merchants with a single integration that can orchestrate stablecoin and fiat flows across pay-ins, payouts, treasury, and on/off‑ramps, unified reporting and reconciliation across markets, as well as clear governance around data handling and regulated partners where applicable in each country.

“Emerging Markets are where the next wave of digital consumers is coming from, but moving money in and out of these economies is still complex,” said Marcelo Dutilh, Product Lead for Stablecoins at dLocal.

“With Stablecoin Full, we treat stablecoins as just another local payment method inside dLocal’s platform. Merchants get the benefits of faster, more flexible rails, without having to manage crypto infrastructure or regulatory complexity.”

“Stablecoins are moving from experimental to real payment infrastructure. Our merchants don’t want to become crypto experts or navigate regulation market by market. They want a single partner that handles that complexity for them. That’s exactly what dLocal provides.”

13:40 – An interesting time for payments?

Jessie Toh, Vice President and Global Treasurer at Coda Payments, pointed to the rise of embedded payments and instant local payment options as defining features of today’s landscape.

But the biggest shift, she said, is the amount of data now available. Toh said, for treasurers, this data provides transparency, which allows money to move earlier, whereas in the past, delays were more common because the information simply wasn’t there.

13:20 – EBANX announces recurring APMs

Making the most of the event, EBANX has announced the expansion of its recurring alternative payment methods to six more countries – the Philippines, Indonesia, Thailand, South Africa, Colombia and Peru.

Eduardo de Abreu, Global Chief Product Officer and Regional CEO of EBANX Singapore, said this will allow global merchants in streaming, SaaS, and gaming to reach more than a billion consumers who rely on local payment options instead of cards.

He highlighted new integrations with wallets such as GCash and Maya in the Philippines, OVO and DANA in Indonesia and TrueMoney in Thailand, as well as recurring features in South Africa’s Capitec Pay and Latin America’s Pix Automático, Nequi and Yape.

“Consumers without access to credit or debit cards rely heavily on APMs to pay for subscription-based e-commerce services,” said de Abreu.

12:40 – Know Your Agent before an Agentic Commerce push

It comes as no surprise that agentic commerce and AI agents are some of the key talking points at Money 20/20 Asia, but what are the best security practices for businesses to ensure a safe protocol is in place before enabling agentic payments?

Abhijeet Ramesh, VP, Head of Innovation & Growth, APAC at Visa, spoke on the importance of developing the Know Your Agent (KYA) standard, an offshoot of traditional finance’s Know Your Customer (KYC).

He shared how Visa is currently handling this process in real-time, as the technology is still in its relative infancy. Ramesh also spoke on the company’s ability to accommodate new, innovative players and technologies, while still maintaining that security measures are kept in place.

“There needs to be a way to bring in every new kind of player that shows up,” he said. And in this case (with agentic commerce), we can’t yet let (anyone) in as we need to know who the agent is, is it reliable, is it secure, how they connect to us, etc.”

“But more importantly, all the other network participants, such as the banks who are initiating the transactions, need to also know if (agents) are secure. The merchants want to know which agent is going to come into their surface. So to do all of that, we have programmes which we call your agent programmes. We have a structured way of bringing into agency to the payment ecosystem and in some ways, getting them to play by the same rules that everyone else does.”

But what if the agentic transaction fails, are there regulatory standards and procedures to abide by for such a new innovation?

Alvinder Singh, Head of Innovation Acceleration Office at the Monetary Authority of Singapore (MAS) believes they are close to a solution but admits that regulations for innovations such as this can take its time.

“It’s an interesting question because we are speaking in a world where we have accepted that we are in the very early days of agentic,” said Singh.

“Regulations don’t get strengthened in the very early days, only because regulators, as much as you will believe that we have special powers and we have crystal balls that fall in our hands that tell us this is what the future is like, we are finding our way and learning from all of you.

Now, are we there (with regulations) for agentic commerce? Maybe, maybe not. Maybe not would be that you could have chosen not to deploy that agent because remember, you can solve that quite effectively or you could do quite a lot of things online quite effectively without an agent.

“I’m not suggesting that that is foolproof in any case, where you could do it yourself, but you deploy this requires a degree of sophistication on your part, which means that personal responsibility has to come in as well.”

12:15 – WalletConnect and iMin bring stablecoin payments to Android checkouts

iMin, a global provider of Android‑based smart business devices, announced a collaboration with WalletConnect Pay to enable stablecoin payments directly at checkout, showcased through a live demonstration at Money20/20 Asia.

Leveraging WalletConnect’s wallet network of over 500m users, as well as over 700 wallets across all major blockchain networks, alongside iMin’s open Android hardware ecosystem, the collaboration aims to place stablecoin and crypto payments directly into merchant environments.

The iMin and WalletConnect Pay brings smart POS devices into stablecoin interactions, using iMin’s Android‑based terminals to provide the flexibility to support evolving stablecoin payments while maintaining reliability and usability merchants need from modern POS systems.

“iMin has built a global point of sale network, and that’s exactly where stablecoin and crypto payments need to show up,” said Jess Houlgrave, CEO, WalletConnect.

“Together, we’re making it simple for merchants across that network to offer stablecoin and crypto payments without changing anything about how they operate, while giving users a simple, familiar way to spend their stablecoin holdings at the places they already shop.”

The live demonstration at Money 20/20 Asia aims to simulate retail and event payment scenarios and interact with physical devices in real-time, as well as how this can be integrated into smart POS environments.

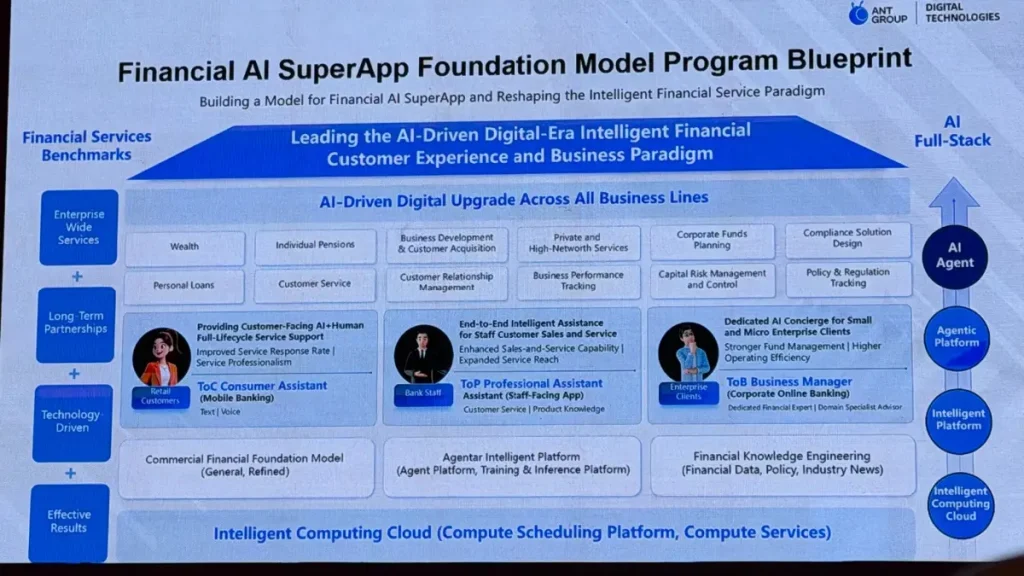

11:40 – Forget super-apps… Meet AI super-apps

Garry Sien, Chief Innovation & Solutions Officer at Ant Digital Technologies, delivered a keynote on how AI is reshaping global finance.

He notes that in China, people are already making payments from their cars, and joked about Bangkok’s traffic before asking: “Wouldn’t it be useful if AI agents could handle payments during those moments?”

“If you’re still building for desktop, that was yesterday,” Sien said, stressing that AI will drive risk management, business growth and customer experience far beyond the mobile phone.

He highlighted examples such as Ant Fortune for financial advisors, Ant AQ as an AI‑native health app, and Alibaba Real‑Time Delivery for marketing and transaction growth.

Super‑apps are a characteristic of Asia, and while the rest of the world is still playing catch‑up, it seems the region has already identified AI as the next step to improve and expand these platforms.

11:20 – The cross-border challenges in Asia

During a panel on how local payment providers can support resilient financial ecosystems, the question around cross-border and remittance challenges surfaced.

Rachel Whelan, APAC and MEA Head of Corporate Cash Management for Deutsche Bank, revealed 13 out of the 20 largest remittance corridors live in Asia and Asia-Pacific. Therefore, cross-border money transfers should be fast and seamless, right?

This is not the case for Whelan, who revealed there remains friction in the cross-border payment process in Asia. She revealed that during a Taiwan in-bank flow, the beneficiary has to show up to its branch in person just to prove the payment is there.

“To move money in and out of these countries is not easy,” said Whelan.

“We need to make a change to opening up more and working together, it’s happening, but now we have moved into a stablecoin multiverse where they are the answer, but they’re not.”

Whelan prefers to focus on the regulatory collaboration between policymakers across Asia to solve this cross-border friction issue, to alleviate manual processing of liquidity and financial exchange rates with a more digitised and seamless approach.

10:30 – A look at Azerbaijan

Azerbaijan is not a market that usually receives much attention in the payments space, but events like this bring different worlds together.

This was the case when Kieran O’Connor, Senior Journalist at Payment Expert, met Maxim Evdokimov, Chief Product and Marketing Officer at Bir, just outside the busy hall.

Evdokimov explained that Azerbaijan is working to increase adoption of digital payments and reduce reliance on cash. With an older population than some of its neighbours, such as Uzbekistan, this is turning out to be a significant challenge.

According to Evdokimov, people trust the banks but are less confident in the technology. The government is helping to bridge that gap by digitising infrastructure, including digital IDs that can be used to apply for loans.

Bir is contributing by expanding into e‑commerce and education initiatives. As seen in the UK, encouraging people to adopt new payment methods requires demand, and someone has to create it.

09:40 – The Bank of Thailand on the country’s data problem

Daranee Saeju, Assistant Governor at the Bank of Thailand, explains that farmers in Thailand are more connected than ever before.

However, there is still a gap. When a farmer goes to the bank, they are still “financially invisible,” says Saeju.

Thailand is working to close this gap by enabling people in remote areas to open bank accounts and make payments through PromptPay, which now has 92 million registered accounts.

The next challenge is data sharing, with the Bank of Thailand aiming to move from isolated “data islands” to a trusted, regulated “data highway” called Your Data.

“The task before us is clear. not simply to digitise finance, but to humanise it, ensuring that finance serves people, because behind every dataset there is a person,” Saeju says.

09:30 – Is Thailand a leading financial market?

Warotai Kosolpisitkul, International Economic Advisor for the Ministry of Finance of Thailand, followed Davies and Sieber on the Radiant Stage to deliver a keynote on why Thailand sits at the heart of financial innovation in Asia and wider Asia-Pacific.

Kosolpisitkul said there are four key pillars that defines the global money flows; goods and services, people in labour, data and knowledge, and capital and investment.

“That brings us to a key question, why Thailand?,” said Kosolpisitkul.

He declared that Thailand is “uniquely positioned” as one of the leading financial markets in Asia due to its strategic location, acting as a natural gateway to financial and capital markets. He also explained the country’s digital payment adoption as to why its financial infrastructure has become digitised to help serve multiple different demographics as “one of the most advanced in the region”.

“Thailand’s financial infrastructure is among the most advanced in the region, supported by robust payment systems, including Prompt Pay and QR code cross-border payments, strong digital banking adoption, and the introduction of virtual banks, which will expand access to unserved and underserved segments of the market.”

He continued to emphasise that the fundamental component that underpins Thailand’s financial infrastructure above all else, is trust.

Kosolpisitku explained why trust is the foundation of all successful financial ecosystems, highlighting China’s financial data and education initiatives that have enabled the country to connect dots to enable transparent and secure financial transactions.

“Allow me to emphasise that Thailand does not compromise on trust.”

“We are committed to ensuring that our financial system is secure, transparent, globally, credible, and we will not allow Thailand to become a paradise for financial misconduct.”

Kosolpisitku concluded his keynote by incentivising international companies why setting up shop in Thailand comes with additional benefits, such as reduced personal income tax which is designed to benefit corporations.

This is outlined under the International Business Centre’s framework, as its Board of Investment has introduced a corporate tax holiday and long-term Visa’s to compliment long-term residencies, underscored by a digital tax system to modernise the tax filing process.

“Ladies and gentlemen, the future of finance will not be determined by geographical boundaries, but rather by the strength of an interconnected ecosystem capable of attracting capital rules, fostering trust, and enabling sustained innovation,” said Kosolpisitku.

“In this evolving landscape, Thailand is strategically in line with global insights with the practical implementation to establish a robust and competitive financial environment.”

09:15 – Tracey Davies and Money 20/20 Chief Strategist, Scarlett Sieber, opened Money 20/20 Asia by outlining the theme of this year’s event; ‘From infrastructure to impact’.

Davies reveals that this has become the fundamental aspect of Asia’s emergence as a leading financial and payments region, proclaiming that the “impact is real and it is already happening, understanding what is working and what is next”.

“The world looked to the West to see where finance is heading, but it is now happening right here in Asia,” said Davies.

Some of the preliminary numbers Davies and Sieber revealed highlight the growth of the Asia branch of Money 20/20’s brand. Davies and Sieber said there has been a 20% year-over-year increase in the number of companies which will attend the 2026 event this year, with 1,400 projected companies. There will also be an estimated 4,000 attendees, a 30% YoY increase.

08:55 – Money20/20 Asia 2026 begins!

It’s the first day of Money 20/20 Asia as Payment Expert awaits the welcoming and opening addresses from Money 20/20 President Tracey Davies, and then followed by Warotai Kosolpisitku, Thailand’s Minister of Finance.