Interchange fees can be traced as far back as the 1910s in the US and have been an essential part of the payment experience for merchants, issuing and acquiring banks, and perhaps more importantly, the card networks.

The entire payment lifecycle, from authorisation to reconciliation, includes an interchange fee and has become a source of criticism and controversy since they were implemented in the 1970s.

An interchange fee is an attached fee to a card transaction, sent to the merchant’s acquiring bank and received by the customer’s issuing bank.

Interchange fees are a part of every card transaction, debit or credit card.

Here is a step-by-step guide of the process:

- A customer pays a merchant a fee for a good or service.

- The card network authorises the payment to the customer’s issuing bank, where the issuing bank keeps a small percentage of the payment.

- The card network then authorises the payment to the merchant’s acquiring bank, keeping a small amount of of the payment, typically a larger percentage than the issuing bank

- The payment is then sent back to the merchant from their acquiring bank with the interchange fee percentages taken from the issuing and acquiring banks.

The percentages of what the acquiring and issuing banks receive varies on the card networks’ interchange fee and is dependent on which country the transaction was settled in.

The purpose for interchange fees is to protect the costs of authorising, processing and securing the payment. They are also in place in order to protect transactions from fraud, to maintain card network infrastructure and enable banks to continue issuing debit and credit cards.

How are interchange fees calculated?

Card networks determining an interchange fee are calculated on several different factors.

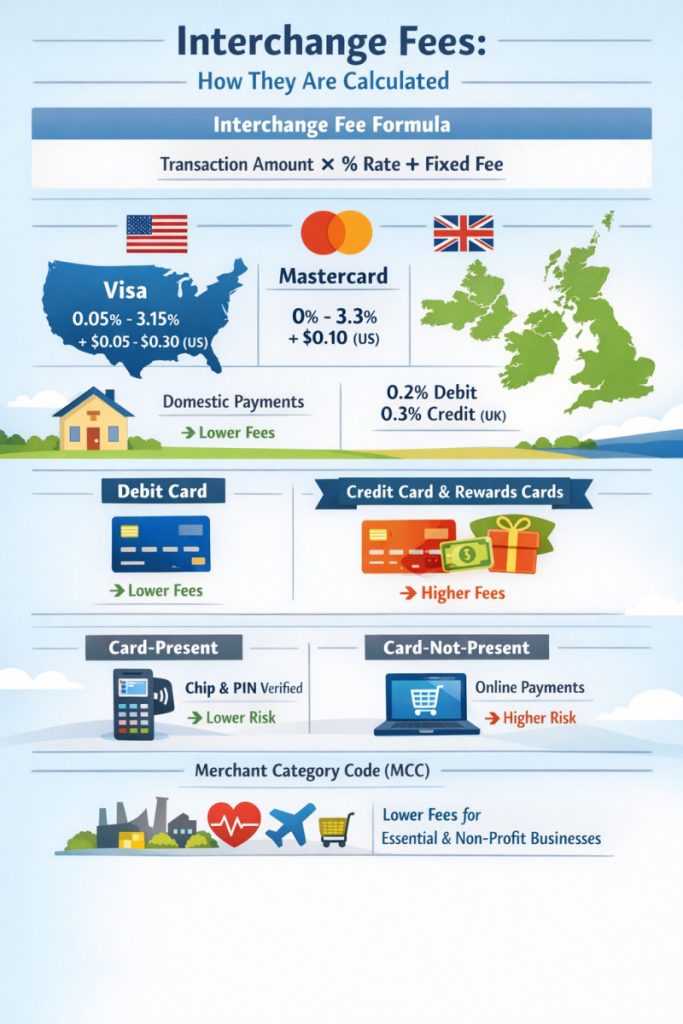

The general rule for an interchange fee calculation is transaction value x percentage rate plus fixed per-transaction fee.

The percentage rate is set by the card network. The two largest card networks, Visa and Mastercard, have different interchange fee rates for different countries.

For Visa in the US, its interchange fee ranges from 0.05% to 3.15%, plus $0.05-$0.30 per transaction. In the UK, Visa’s interchange fees are capped at 0.2% for debit cards and 0.3% for credit cards.

For Mastercard in the US, 0% to 3.3%, plus $0.10 per transaction. In the UK, Mastercard’s interchange fees are capped at 0.2% for debit cards and 0.3% for credit cards.

Domestic payments often carry a lower interchange fee than cross-border international payments.

The percentage is typically lower for payments via debit cards due to the customer already having the money in their account. Credit card interchange fees are typically higher to compensate the issuing bank due to the credit repayment process.

Interchange fees for rewards and loyalty cards are also typically higher, up to 0.3%. The reward or perk attached to the transaction, such as cashback, is covered by the interchange fee for the issuing bank.

There are differing interchange fee rates for the level of risk associated with the transaction.

- Card-Present; payments made via inserting a card or tapping it onto a terminal, typically carries a lower interchange fee charge as these transactions are verified by chip and/or PIN and therefore are lower risk to fraud.

- Card-Not-Present; payments typically made online where the merchant can not see the card information, will carry a higher interchange fee charge due to having a high risk of fraud attempts.

Interchange fees also vary depending on the merchant. This is determined by a Merchant Category Code (MCC), a four-digit code that is assigned to a merchant by its acquiring bank.

The MCC enables card networks to calculate an interchange fee which can be typically lower for businesses such as utility companies, charitable organisations, and travel agencies.

Interchange fee pricing models

There are three main types of payment processing used to process interchange fees, as each model differs in pricing and costs associated with card payments.

Interchange plus pricing

Interchange plus pricing, also known as cost plus pricing, is a model that sees the merchant pay the exact interchange fee as well as a markup fee set by the chosen payment processor.

A markup fee is an additional charge added to the total transaction value to ensure profit. This is calculated via a percentage formula of: Selling Price – (minus) Cost x (times) 100.

As interchange fees can vary, the interchange plus pricing fee enables the merchant to see the exact amount the interchange fee is charging within the total transaction value.

Subscription pricing

The subscription or membership pricing model is widely used by subscription-based services, such as streaming services like Netflix, where customers pay a recurring fee for a service.

Interchange fees within the subscription pricing model are typically lower than other models as the markup fee attached is a flat fee as opposed to a percentage used for Interchange plus pricing.

This pricing model is usually customer-friendly as it is designed to help subscription-based companies reduce churn and offer flexibility to subscription plans.

Tiered pricing

A Tiered pricing model consists of three different tiers: qualified, mid-qualified and non-qualified, each coming with their own rates based against risks and rewards.

Qualified is the tier with the lowest rates. This is for payments used by a non-rewards debit or credit card and is a Card-Present transaction. This rate typically ranges between 1.5%-1.9%.

The mid-qualified tier is for payments made with a basic rewards card, earning perks such as cashback. The payment can be performed via a manual key if terminals do not support the transaction. The rate typically ranges between 2.3%-2.8%.

Non-qualified tiered payments often carry the highest rate. This is used for premium rewards cards, such as Chase’s Sapphire Card, and mostly all payments made online or on e-commerce sites. The rate typically ranges between 3.2%-4.5%.

All three tiered pricing models are applicable for a range of business models. Netflix will primarily use a subscription pricing model, while a company like Amazon will use the tiered pricing model due to most of its payment volume being e-commerce.

History of criticism, controversy and amendments

It can be argued that interchange fees have been a source of controversy between card networks, banks and merchants since first being introduced in the 1970s.

With point-of-sale systems being developed and card payments becoming more popular amongst consumers, card networks such as Visa and Mastercard began implementing interchange fees.

Card networks will argue interchange fees are essential to keep the entire four-party payment system functioning. They also argue for interchange fees in order to compensate issuing banks and protect transactions from fraud and other security threats.

Merchants, and more recently regulators, have criticised interchange fees as an enforced charge on their business without their control.

The card networks have operated a “Honour All Cards” rule since introducing interchange fees. This rule means if a merchant were to accept a standard, basic retail card, it therefore must accept all branded cards from the card networks, including the high-reward, premium cards that come with the highest interchange fee rates.

There is also a double-edged sword dilemma for merchants: stop accepting large, common cards like Visa and Mastercard branded cards, but lose customers, or continue to accept interchange fees imposed by these card networks which could hurt profit margins.

Walmart vs. Visa and Mastercard

The first prominent, high-profile battle between a merchant and card networks involved Walmart vs. Visa and Mastercard in the US.

Walmart launched a class-action anti-trust lawsuit against Visa and Mastercard in 1996 with the support of millions of other merchants accepting debit Visa and Mastercard branded card payments.

The plaintiffs argued that due to accepting the two card networks’ credit cards, they were forced to accept their debit cards and ultimately subjected to the interchange fees that come with these transactions on these cards.

The lawsuit was settled in 2003 as Visa and Mastercard agreed to pay $3bn to Walmart and the plaintiff merchants while also agreeing not to tie their debit and credit cards, scrapping the Honour All Cards rule to allow merchants to select either debit or credit cards.

Despite this settlement, Walmart continued to take issue with Visa and Mastercard interchange fees.

In 2014, Walmart sued Visa seeking $5bn in damages after the supermarket believed the card network inflated its interchange fees from 2004 to 2012. Walmart opted out of a class-action lawsuit filed against Visa and Mastercard from several merchants, which was settled for $5.7bn, as it believed the settlement fee was not adequate.

The 2014 lawsuit was settled out of court between Walmart and Visa in 2016. The specifics of the settlement were not publicly available.

The new UK/EU interchange fee cap

On the other side of the Atlantic, UK merchants have also taken issue with Visa and Mastercard interchange fees.

A 2005 class-action lawsuit was filed by several UK retailers and trade associations for allegedly fixing interchange fees. The lawsuit also claimed it may have breached European Union (EU) and European Economic Area (EEA) and UK antitrust laws.

However, in December 2015, the EU introduced the Interchange Fee Regulation which caps interchange fees for debit cards at 0.2% and 0.3% for credit cards.

Despite this, the 2005 UK lawsuit led by Walter Merrick continued in a bid to receive damages from Mastercard. The case was settled for £200m in May 2025 after Merrick initially attempted to retrieve £14bn in damages.

The record $30bn settlement

In March 2024, Visa and Mastercard had reached a settlement with merchants who also filed an anti-trust lawsuit against both card network companies in 2005.

Visa and Mastercard agreed to pay over $30bn in damages and agreed to reduce credit interchange fees and impose caps on the new rates in 2030. In November 2025, Visa and Mastercard also proposed to drop its interchange fees for US merchants by 0.1%.