Central bankers are pushing back hard against stablecoins, warning that privately issued digital money threatens monetary policy, financial stability and public trust

When Christine Lagarde stood before European lawmakers this week, few would have expected her to open fire on stablecoins.

Speaking at the European Parliament’s Committee on Economic and Monetary Affairs, on June 23, the President of the European Central Bank (ECB) delivered a striking warning about the growing risks posed by digital assets, particularly those marketed as stable in name but not always in nature.

“Stablecoins are privately issued and notably pose risks for monetary policy and financial stability,” Lagarde said, calling out their volatility and the threat they pose to the transmission of interest rates. Her remarks, which veered firmly into regulatory territory, included a pointed reference to Tether, the largest stablecoin issuer, highlighting that it is domiciled in El Salvador, a jurisdiction she noted has “no prudential framework” for oversight.

Lagarde’s intervention wasn’t an isolated shot.

Days earlier, the Bank for International Settlements (BIS) – often referred to as the central bank for central banks – issued a sweeping and unusually blunt report that appeared to echo, and even sharpen, the ECB’s concerns.

It accused stablecoins of failing the basic tests of what makes money “fit for purpose” in a modern economy and cast doubt on their long-term viability as instruments of value or exchange.

Together, these public-sector salvos point to a deeper anxiety gripping monetary authorities: that a parallel system of digital money, driven by private companies and anchored in crypto ecosystems, could undermine decades of carefully built monetary order.

The roots of anxiety

At the heart of the growing tension between policymakers and the private sector is a fundamental disagreement about who should control the future of money.

For stablecoin issuers like Tether and Stripe, the answer lies in decentralised infrastructure, faster settlement, and borderless transactions. For central bankers, however, these innovations come with a dangerous cost: the erosion of control, oversight, and ultimately, trust.

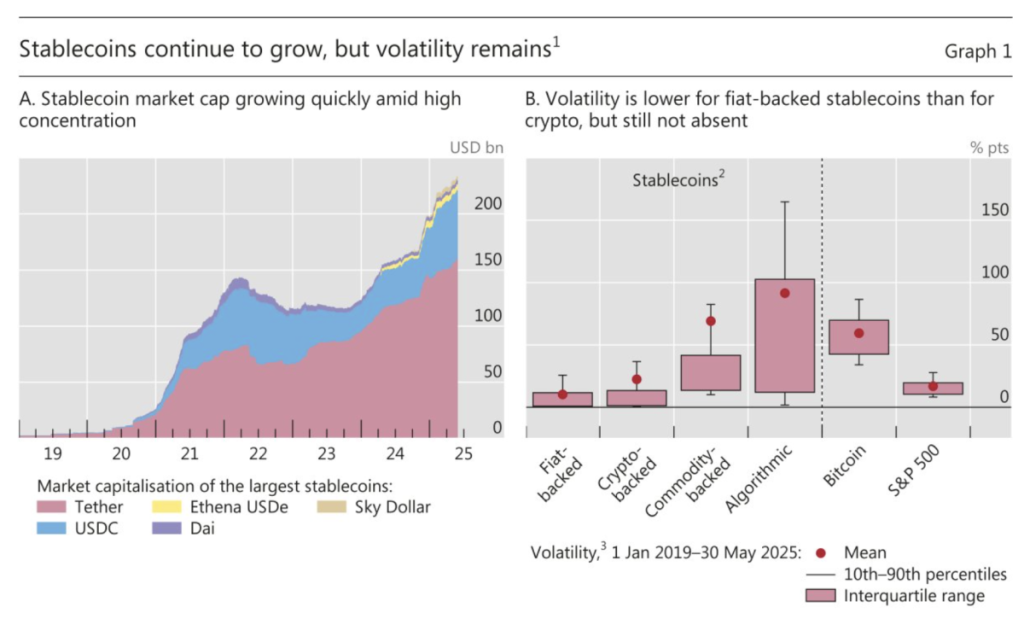

Lagarde made no effort to soften her view. While acknowledging that crypto-assets have become “a fast-developing segment of the financial landscape,” she drew a sharp line between innovation and recklessness. Unbacked crypto-assets, she said, were “unsuitable as a reliable means of exchange” due to “investor speculation and extreme price volatility.” Stablecoins, she added, might appear more secure on the surface, but pose risks that go deeper than price swings.

“Stablecoins are not always able to maintain their fixed value, compromising their usefulness as a means of payment and a store of value,” she told MEPs. More worryingly for the ECB, these privately issued digital tokens could draw deposits away from the banking system, thereby “adversely affecting the transmission of monetary policy through banks.”

The BIS – known for its typically cautious tone – went further. In its report, it deployed a rigorous framework to test the suitability of stablecoins as a foundation for a modern monetary system. It found them wanting in three core areas: singleness, elasticity and integrity.

On singleness, the report likened stablecoins to a return to the 19th-century “free banking” era in the US, when multiple private currencies coexisted with varying values and levels of trust. “When a payee receives a stablecoin as payment,” the report explains, “it is the liability of a particular stablecoin issuer.” In practice, this means users may find themselves holding a patchwork of ‘red’, ‘blue’ or ‘white’ digital dollars, none of which are guaranteed to hold equal value or be accepted universally.

On elasticity, the report notes that stablecoins are structurally limited by their design. Because each coin must be backed by a reserve asset (typically one-for-one), issuers cannot expand supply on demand – a stark contrast to how commercial banks extend credit and create money in response to economic activity.

“This imposes a cash-in-advance constraint,” the BIS says, making stablecoins fundamentally ill-suited to support liquidity in the real economy, particularly during times of stress.

But it is the third test – integrity – that raises the sharpest alarm. Stablecoins, especially those used through unhosted wallets and decentralised platforms, lack the robust anti-money laundering (AML) and know-your-customer (KYC) safeguards that underpin the traditional banking system. The BIS notes that these instruments have become “the go-to choice for illicit use to bypass integrity safeguards,” citing their pseudonymous nature and ability to operate outside regulated financial networks.

While some issuers and exchanges have introduced controls, the report warns that enforcement is patchy and difficult to scale. “In practice,” it concludes, “stablecoins are attractive for use by criminal and terrorist organisations.”

Together, these critiques paint a damning picture: a fast-growing ecosystem of digital money that offers convenience and access, but at the cost of trust, stability, and control. For central banks, that is a compromise too far.

Enter the digital euro

If stablecoins represent a fork in the road for the future of money, central banks are making it clear which path they believe society should take.

For Lagarde and her peers, the answer lies not in fighting fire with fire, but in rebuilding the system from within, with central bank digital currencies (CBDCs) forming the backbone of a modernised, programmable financial infrastructure.

“Accelerating progress towards a digital euro is a strategic priority,” Lagarde said in Brussels. “It would help safeguard Europe’s bank-based financial and monetary system… and ensure an innovative and resilient European retail payments system.”

A digital euro, unlike stablecoins, would be issued and backed by the central bank itself – providing the ultimate settlement asset with full trust and regulatory clarity. Where stablecoins float on a sea of speculation and governance opacity, CBDCs would rest on the bedrock of public accountability.

The BIS shares this vision but pushes it further. In what it calls a “next-generation monetary system”, the BIS envisions a world where not only central bank reserves are tokenised, but so too are commercial bank deposits and even government bonds; all residing on a unified, programmable platform.

Such a platform, dubbed the unified ledger, would allow for real-time, atomic settlement of payments and financial assets, automating transactions like collateral transfers, securities settlements, and cross-border payments.

“Tokenisation enables the contingent performance of actions,” the report explains, “meaning that specific operations are triggered when certain preconditions are met.” Think of a loan contract that releases funds automatically when collateral is verified, or a tax payment that executes upon receipt of a digital invoice.

To central bankers, this is a strategic defence against the fragmentation, opacity and external influence that unregulated digital money introduces. “The issuance of private currencies like stablecoins satisfies a demand for new technological features,” the BIS concedes, “but even with regulation, their limitations cast serious doubts about their ability to be the mainstay of the monetary system.”

Indeed, the push for tokenised public money is already under way. The BIS Innovation Hub is working with seven central banks on Project Agorá, exploring tokenised cross-border payments. Project Pine, run jointly with the Federal Reserve Bank of New York, is testing how monetary policy operations, like repos and interest payments, could be carried out using smart contracts on tokenised central bank reserves.

In Europe, legislative groundwork for the digital euro is being laid, with Lagarde urging swift adoption. “We need to see targeted fiscal and structural policies and strategic investments,” she said. “A legislative framework to pave the way for the potential introduction of a digital euro should be put in place rapidly.”

In short, the message is ‘innovation, yes, but on the central bank’s terms’.

A fragile truce?

The tension between stablecoin innovators and central bankers is a battle over trust, governance, and who ultimately sets the rules in the financial system.

For now, the two visions are on a collision course. The private sector promises speed, accessibility and borderless convenience; the public sector offers security, stability and regulatory clarity. But so far, efforts to reconcile these models have been limited. While frameworks like the EU’s Markets in Crypto-Assets Regulation (MiCA) mark progress, global regulation remains fragmented, and major stablecoin issuers continue to operate out of lightly supervised jurisdictions.

Yet demand for stablecoins is not going away. With over 99% of existing stablecoins pegged to the US dollar, their appeal – particularly in regions with volatile currencies or capital controls – is hard to ignore. As the BIS report notes, “stablecoins provide access to foreign currencies… and can be particularly appealing for cross-border payments and trade settlement.”

This creates a difficult policy dilemma. Should central banks seek to co-opt stablecoin innovation into the regulated sphere, or work to displace it entirely with their own digital currencies? And is there space in the middle, for example, through public-private models where regulated firms issue stablecoins backed by tokenised central bank reserves?

Some industry voices argue that alignment is not only possible, but inevitable. Just as fintechs have partnered with banks to deliver new services within existing frameworks, so too might stablecoin issuers eventually fall in line (provided the regulatory goalposts are clear and globally consistent).

“The Commission’s move is a clear signal that stablecoins are no longer on the fringe and are fast becoming a serious part of the mainstream financial system,” says Laurent Descout, CEO and Co-founder at Neo.

“Despite the ECB’s concerns, this momentum reflects real demand for faster, more transparent, and cost-efficient cross-border payments. What matters now is pairing innovation with the right safeguards to ensure stability and trust.”

As long as stablecoins promise features the public sector struggles to match – 24/7 settlement, pseudonymity, direct peer-to-peer payments – the temptation to operate in the grey areas will persist. And for central banks, whose legitimacy depends on public trust and systemic stability, that’s a red line.

For now, the future of digital money remains undecided. Will it be shaped by code written in corporate boardrooms, or by policy hammered out in parliamentary chambers and Basel committees? Perhaps the answer, as with money itself, will ultimately depend on what people are willing to accept, and who they choose to trust.