New BIS research confirms stablecoins’ growing influence on Treasury yields, raising questions about financial stability and market structure

The steady growth of dollar-backed stablecoins has shifted them from crypto side projects to serious players in traditional markets.

A new working paper from the Bank for International Settlements (BIS) draws a line under that transformation. According to the authors, Rashad Ahmed and Iñaki Aldasoro, flows into stablecoins are now influencing the pricing of US Treasury bills.

Payment systems that once viewed stablecoins as experimental are now connected to instruments which move the most liquid sovereign debt market in the world.

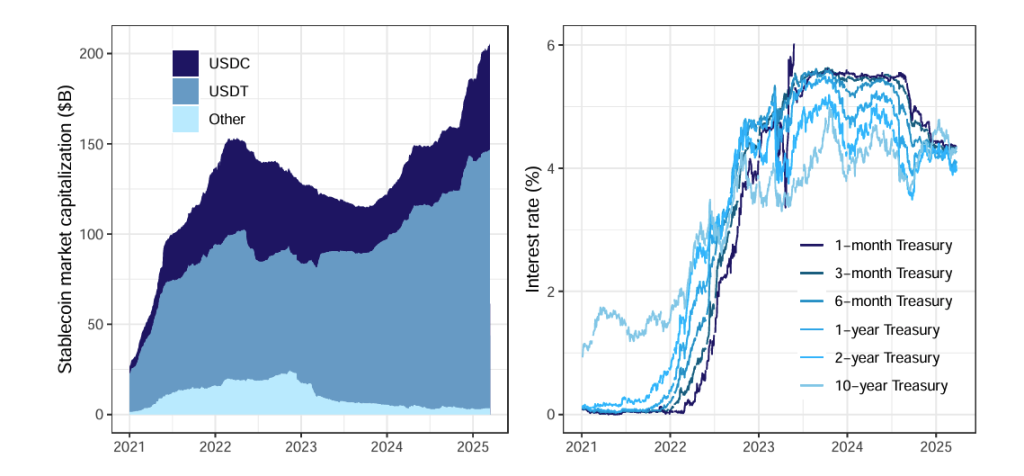

The BIS paper shows that inflows into stablecoins, particularly USDT and USDC, have a statistically significant effect on 3-month Treasury yields. A $3.5 billion inflow, equivalent to a two-standard deviation move, lowers yields by 2 to 2.5 basis points within ten days. The effect is both measurable and asymmetric; outflows of the same magnitude push yields up by as much as 6 to 8 basis points.

Stablecoin issuers back their tokens with short-term dollar assets, chiefly Treasury bills. New inflows mean new purchases; redemptions force sales. The result is a direct link between digital asset flows and public debt pricing.

Not just money, but market participants

That stablecoins now behave like institutional investors is no longer in question. In 2024, USDT and USDC bought nearly $40 billion in Treasury bills, an amount comparable to major US government money market funds. By early 2025, stablecoin reserves surpassed the short-term securities holdings of countries such as China and Japan.

This moves stablecoin issuers from the role of payment intermediaries to participants in the broader financial system. Yet unlike traditional funds, they operate in a regulatory grey zone. The BIS highlights the imbalance: while USDC, issued by Circle, offers relatively detailed reserve disclosures, USDT, issued by Tether, does not. Given their scale and systemic footprint, this lack of transparency carries growing implications.

The study also raises concerns about market dynamics during stress. Whereas inflows allow for flexible investment timing, redemptions demand immediate liquidity. This distinction likely explains the larger impact of outflows on yields. Should redemptions accelerate under pressure, the risk of destabilising sales in the Treasury market cannot be ruled out.

Quiet influence, growing weight

Probably the most alarming of the BIS findings is the subtlety of the effects. A few basis points in yield movement may seem negligible in isolation. Yet in financial markets, such shifts carry weight, especially when triggered by private entities with limited oversight.

The authors note that were stablecoin markets to grow to $2 trillion by 2028, as projected by the US Treasury Borrowing Advisory Committee, a proportionally larger inflow could suppress short-term yields by nearly 8 basis points. These movements would matter not just to traders, but to policymakers seeking to manage interest rates and liquidity.

This introduces a new layer of complexity to monetary policy transmission. Demand for Treasury bills from a rapidly scaling sector outside the banking system could reduce the responsiveness of yields to central bank signals. That challenge is reminiscent of past puzzles in bond markets, such as the early-2000s “conundrum” faced by former Federal Reserve chair Alan Greenspan when long-term rates failed to respond to rate hikes.

A shift in financial architecture

Stablecoins are increasingly embedded in the architecture of financial markets. They provide liquidity, serve as collateral, and now visibly affect the price of public debt. Their reserves resemble those of money market funds. Their flows move interest rates. And yet, their regulation, risk buffers and transparency standards remain inconsistent.

The BIS analysis offers an early but concrete signal that this evolution is already shaping market outcomes. While stablecoins were designed for efficient digital payments, their reserve strategies are turning them into macro-financial actors.

How far this influence extends will depend on market growth, regulation, and how central banks choose to respond.