Recent reports of “no‑KYC” card programmes has brought to light huge weaknesses in the issuing supply chain, forcing networks to take direct action.

UnCash has criticised Mastercard’s processes after the network shut down cards linked to the company’s “no‑KYC” service.

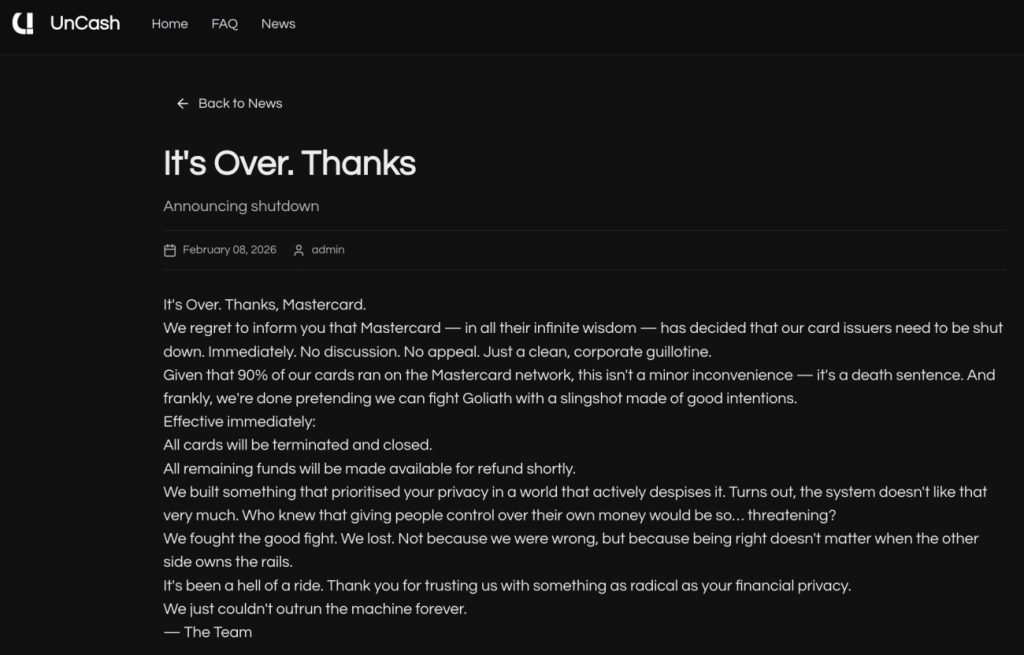

In a statement posted to its website on February 10, 2026, the firm described Mastercard’s actions as “a clean, corporate guillotine,” adding the decision had effectively ended its ability to operate.

The message, which appears to have since been removed, said the majority of UnCash’s cards were issued on Mastercard’s network.

“Given that 90% of our cards ran on the Mastercard network, this isn’t a minor inconvenience — it’s a death sentence,” the company wrote. “And frankly, we’re done pretending we can fight Goliath with a slingshot made of good intentions.”

UnCash told users all cards would be closed immediately, with remaining balances to be refunded. The company insisted it had acted appropriately, claiming it had been treated unfairly.

The statement continued: “We built something that prioritised your privacy in a world that actively despises it,” the statement continued. “Turns out, the system doesn’t like that very much. Who knew that giving people control over their own money would be so… threatening?

“We fought the good fight. We lost. Not because we were wrong, but because being right doesn’t matter when the other side owns the rails.”

What was ‘the good fight’?

UnCash is one of several “no‑KYC” crypto card providers identified in recent reporting by Fintech Business Weekly.

The publication explained how some services have been able to issue spendable cards by registering corporate entities, partnering with lightly supervised programme managers and routing transactions through US Bank Identification Numbers (BINs).

These cards can usually be funded with crypto and used for everyday purchases, despite limited checks on the individuals behind them. The investigation also noted certain providers marketed their cards to users in higher‑risk jurisdictions, including regions where local banking restrictions apply.

The model takes advantage of the card‑issuing supply chain, where fintechs often work through multiple intermediaries to access payment networks. When those layers operate with inconsistent onboarding standards, issuers may not have full visibility into how cards are being used or who controls them.

This has raised several concerns given anonymous or lightly verified cards can threaten anti‑money laundering controls and expose issuers to significant regulatory scrutiny.

What’s Mastercard doing?

Mastercard has taken direct action against UnCash by cutting off access to its network and therefore preventing the company from issuing or supporting cards.

However, relying on one‑off interventions is unlikely to offer a long term solution, especially as similar services have shown they can re‑emerge just as quickly as they are taken down.

While the industry continues to call for stronger oversight from card networks and regulators, Mastercard has been working on changes to BIN sponsorships, which are a key part of the issuing chain.

These updates were not introduced in response to UnCash or the recent issues highlighted across the “no‑KYC” card ecosystem, but announced late last month as part of a wider effort to raise standards.

The company has launched BIN Sponsor Plus, an accreditation programme designed to strengthen expectations for banks which issue cards on behalf of fintechs.

The scheme, rolled out initially in the UK, seeks to offer more detailed requirements around due diligence, operational controls and ongoing monitoring for sponsors responsible for connecting fintechs to the Mastercard network.

Accredited partners will receive additional support from Mastercard, with the company saying the programme is a way to give fintechs clearer visibility over which sponsors meet higher operational and compliance standards.

Under Mastercard’s rules, BIN sponsors hold the principal issuing licence and remain accountable for meeting regulatory and network obligations.

While the UK was selected as the pilot market Mastercard has said it may expand the programme to other regions once the initial launch is complete.

Payment Expert has contacted Mastercard for comment.