Capped wallets and voluntary participation for non-eurozone providers perhaps show a more pragmatic push to secure support for the digital euro.

European Union (EU) lawmakers have approved several amendments in a bid to control the distribution of the digital euro outside the eurozone.

Ahead of an all-important vote on digital euro legislation set for the first half of 2026, lawmakers on January 28 and 29 looked to re-angle the project from hype to real implementation.

The European Parliament’s committee amendments set out who can distribute the digital euro, under what conditions and how cross-border wallet usage will be capped.

The digital euro is a proposed central bank digital currency issued by the European Central Bank (ECB), invented to provide a public form of digital money alongside cash and commercial bank deposits.

Digital euro spillover under scrutiny

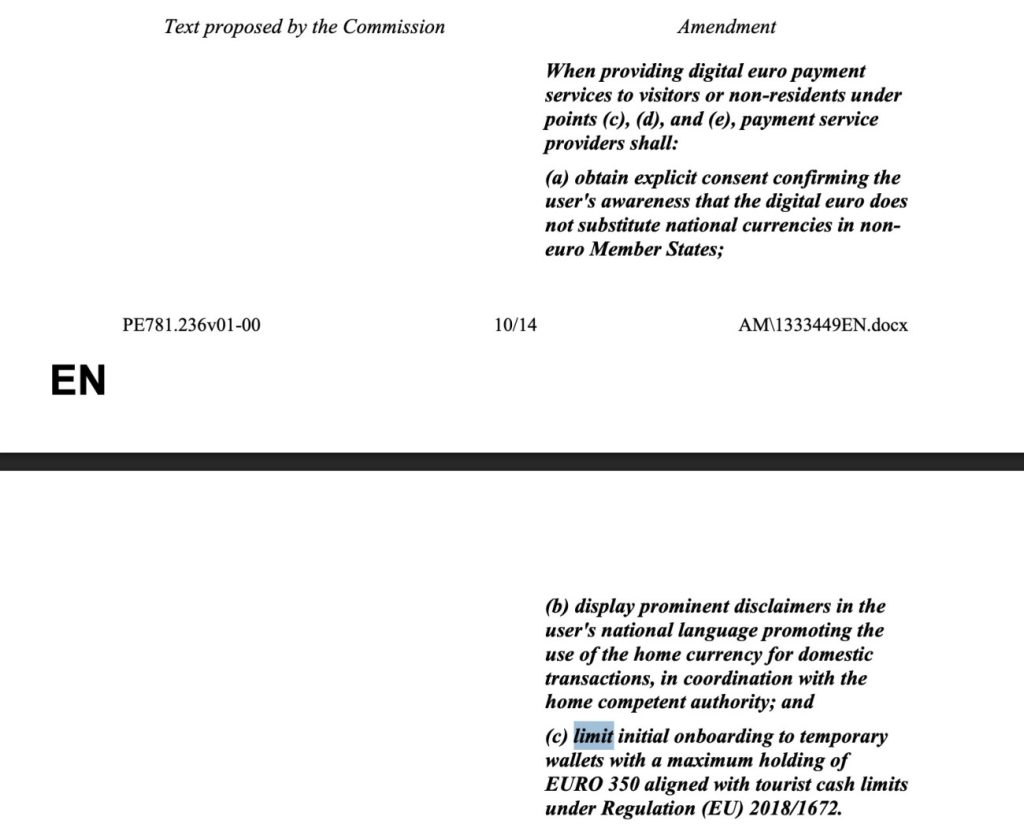

Several amendments target the risk of “stealth euroisation,” where digital euro wallets could gain traction in countries which have not adopted the euro, such as Sweden, Denmark and Poland.

The amendments introduce monitoring requirements for non-Euro countries to help address these concerns, obliging payment service providers (PSPs) to report usage patterns to regulators.

This reporting could include metrics like the number of active wallets, transaction volumes, and the locations of users, aiming to give authorities visibility into adoption and allow them to respond quickly to any unexpected spillover.

At the same time, wallet balances for users outside the eurozone will be capped. By limiting how much digital currency a non-euro user can hold, regulators hope to ensure the digital euro remains primarily a tool for eurozone users.

The amendments also require that digital euro wallets carry clear disclaimers stating the digital euro does not replace the local currency, with users to be informed transactions remain governed by domestic law.

Voluntary participation for non-eurozone providers

During the meetings, lawmakers also shed light on how PSPs outside the eurozone can interact with the digital euro. Previously, even onboarding a single euro-area customer could lead to compliance obligations, creating uncertainty for non-euro banks and PSPs.

Participation is voluntary under the new rules, meaning non-euro PSPs are not required to offer digital euro wallets, which will provide them the freedom to engage with the currency on their own terms.

The amendments also allow non-eurozone merchants to accept digital euro payments through local PSPs, even if the merchant is based outside the eurozone, which could help expand cross-border commerce and B2B payments without forcing full euro adoption.

However, eurozone PSPs are still required to distribute digital euro wallets. These different rules aim to promote the digital euro while respecting the financial independence of countries outside the eurozone.

Is the ECB feeling the pressure?

As noted, legislation governing the digital euro is set for a vote in the European Parliament later this year. If approved, the ECB’s roadmap could be accelerated, with issuance currently targeted for around 2029. Support, however, remains divided.

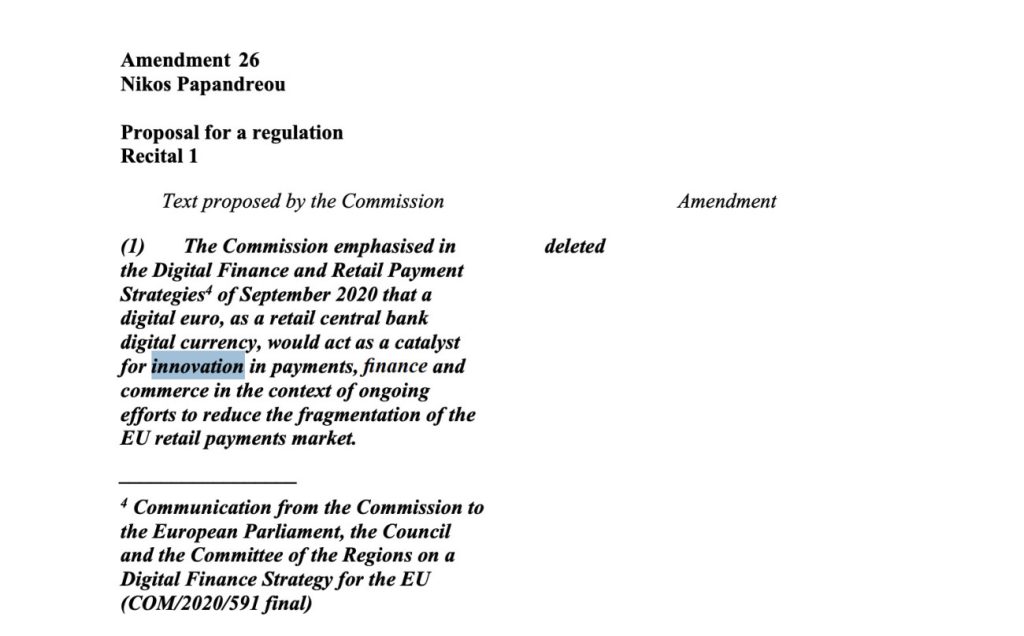

Recent committee amendments highlight a turn in how the project is being developed, showing urgency and a more pragmatic approach.

References to the digital euro as a “catalyst for innovation” have been removed and changes from “must” to “may” in key provisions will likely lead to questions about whether the project is being watered down or simply adjusted to secure wider political backing.

Earlier this month, a group of 70 European academics offered their opinion, urging policymakers not to dilute the digital euro.

In an open letter to MEPs, they warned political compromises could undermine Europe’s financial sovereignty. “A strong public digital euro is not a nice-to-have; it is an essential safeguard of European sovereignty, stability and resilience,” the letter read.