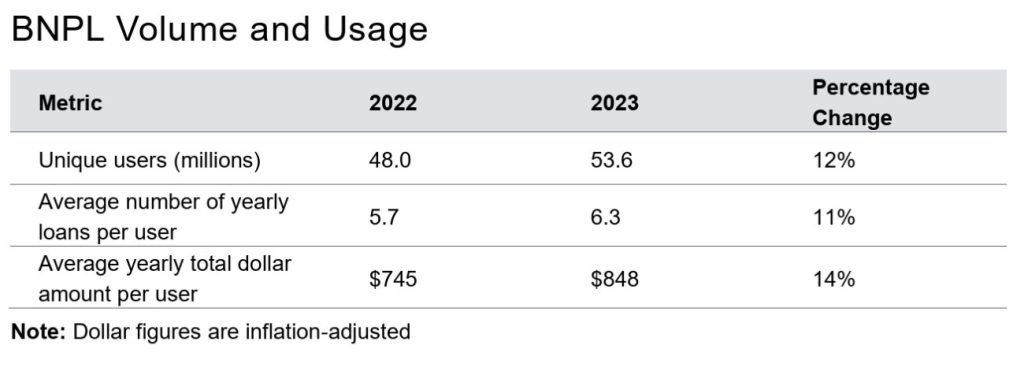

New research shows BNPL users hold multiple concurrent plans, often across different providers

Buy now, pay later products are increasingly being used to cover everyday living costs rather than discretionary purchases, according to a new report from the US Consumer Financial Protection Bureau (CFPB).

This raises fresh questions about whether the fast-growing payment method now functions as a form of consumer credit operating outside traditional safeguards.

The regulator’s latest market study published on December 10, shows BNPL is no longer confined to smoothing cash flow for fashion, electronics or one-off purchases. Instead, a growing share of transactions are linked to groceries, fuel and household essentials, signalling a shift in how consumers rely on the product as cost-of-living pressures persist.

That change in usage, the CFPB suggests, materially alters BNPL’s risk profile, both for consumers and for providers operating at scale.

Everyday spending replaces discretionary use

The report draws on transaction-level data from major BNPL providers and highlights that repeat users increasingly turn to instalment payments for routine expenses rather than occasional purchases. While BNPL has historically been positioned as a budgeting tool, the CFPB’s findings indicate it is now being used to bridge short-term income gaps.

Covering essential expenses through instalment plans could expose consumers to repayment obligations which resemble short-term borrowing, but without the same visibility, affordability checks or standardised disclosures associated with credit cards or personal loans.

One of the report’s more worrying findings is how frequently active BNPL users hold multiple concurrent plans, often across different providers. This behaviour makes it difficult for firms to assess a customer’s total repayment burden and increases the risk that consumers lose track of obligations spread across platforms.

Because most BNPL lending remains off traditional credit files, providers have limited insight into a customer’s wider financial commitments. The CFPB frames this lack of visibility as a systemic issue, warning that it can lead to credit being extended without a full picture of affordability.

Late fees are not marginal

The CFPB also challenges the industry narrative that late fees are rare or easily avoided. While many users repay on time, a meaningful portion incur fees, with repeat fee incidence concentrated among financially vulnerable consumers.

Rather than being isolated mistakes, the report suggests late payments are often tied to structural affordability pressures, particularly among frequent BNPL users relying on instalment plans for essential spending.

Taken together, the findings strengthen the CFPB’s long-standing position that BNPL products should not sit outside consumer credit frameworks simply because they are embedded at checkout. While the report stops short of announcing new rules, its language reinforces the case for closer regulatory alignment with credit products.