Payment Expert has arrived at MoneyLIVE in Amsterdam, providing you live coverage for the next two days. Expect insights from industry leaders engaging in conversations around payments, fraud, AI and much more.

17:30 – Time to reflect and prepare for Day 2

Wow, over already? It’s been a packed schedule at MoneyLIVE, covering everything from fraud and deepfake threats to new regulations, payments innovation and some lively debate…

My personal standout moment would be when Uber Payments COO Divya Bhardwaj delivered a jab at the banks while sharing a stage with Standard Chartered, ING and JP Morgan.

However, looking past the drama, there’s been a clear theme of collaboration. Across discussions on fraud, data and customer protection, you could feel the ecosystem coming a little closer, united by shared challenges and solutions.

It’s been a pleasure bringing you all the updates from the floor today, and I’ll be back tomorrow with full coverage of Day 2.

16:30 – Reluctantly looking past compliance

The conversation then turned to creativity and what comes after compliance-heavy migration work.

Bouille said that once banks have fully completed their transitions, they’ll be able to offer more flexible, value-added services for corporates, something she said businesses are increasingly seeking.

“Once everything is in place, it will reinforce their partnership,” she said. “Banks will be more than just transaction processors.”

16:20 – The ISO 20022 deadline is upon us

There is big date creeping up on us, no not christams, but the ISO 20022 migration deadline.

BNY Mellon’s Isabelle Bouille, Director and Principal Product Manager, Treasury Services, explained adoption is currently at 86%, leaving 14% still to go.

Swift has prepared fallback plans for firms which miss the deadline, ensuring messages can still be sent on the previous standard while they finish migrating.

As for the industry mood? “We’re not seeing the benefit yet,” Bouille said. For now the focus is to get everyone over the line, then improving data quality comes next.

“The migration is far from over,” Bouille said.

15:00 – More needs to be done…

“Reimbursement is never going to be the end game,” said NatWest’s Leslie, adding that while the volume of APP fraud is falling, the value of attacks continues to rise.

When the PSR first announced its reimbursement framework, many payments firms felt the model was unfair. This was because most fraud originates on social media platforms, which is outside banks’ control.

Virgin Media O2’s Harwood explained how the telecoms sector is adapting, stating the company has already blocked suspicious SMS at scale, but this only pushes fraudsters onto alternative channels like WhatsApp. Virgin Media O2 has also deployed new fraud-detection technology, but Harwood noted the limits. He said if the system mistakenly blocks a legitimate call, the reputational damage is significant.

Looking for a way around this, the company has shifted toward call labelling rather than outright blocking. When a call is labelled as a suspected scam, customers answer 42% less often, and even when they do answer, the call duration drops by over 90%.

Both speakers agreed that the path forward relies on far better data sharing between telecoms, banks and tech platforms. However, it appears there is still frustration in the banking sector.

14:50 – PSR reimbursement rules bring new operational challenges

The Payment Systems Regulator’s (PSR) new reimbursement rules, which came into force in October 2024, has entered the spotlight. The regulation requires banks to reimburse victims of authorised push payment (APP) fraud, with the sending and receiving banks now sharing liability 50:50.

On stage to unpack the impact were Jonathan Leslie, Payments Fraud Lead at NatWest, and James Harwood, Head of Fraud, Fraud Strategy and Policy Product Owner at Virgin Media O2.

Harwood reminded the audience that Virgin Media O2 isn’t directly under the PSR remit, but the company has still taken action by signing a new fraud charter alongside BT and Vodafone. The aim is to create more structure around data sharing across the telecoms sector, improving identification and prevention of fraud attempts.

Leslie described the operational reality for banks since October. The 50:50 split between sending and receiving institutions has required NatWest to overhaul processes and significantly scale teams, particularly on the receiving side, which handles recovery and repayment to other banks.

“It wasn’t a small feat by any means,” Leslie said.

14:30 – Revolut Pay’s and why experience matters

Revolut Pay sits at the centre of its 67 million customers and 1 million businesses, and Hellkvist reminded the audience that today’s users don’t compare brands within a category but compare experiences. He said, if an online checkout feels slow, consumers won’t ask why it’s slower than other banks, they’ll ask why it’s slower than Uber.

Most express checkouts may be fast, Hellkvist said, but they offer little else. Revolut Pay aims to change that with a two-click experience which also delivers benefits.

How does it work?

Tap Revolut Pay, the Revolut app opens, facial recognition confirms identity, the customer selects any available discount, pay. “As easy as that,” Hellkvist said.

14:15 – Did Somebody Say Keynote?

Welcome back! After a much-needed lunch break, the crowd at MoneyLIVE has returned, recharged and ready for the second half of the day.

Stage 1 is kicking things off with a strong opener as Anton Hellkvist, Head of Sales, Merchant Acquiring at Revolut, takes to the stage for his keynote: “Revolut Pay: transforming the online checkout experience.”

Hellkvist will outline the major pain points in recurring payments today, explore how convenience and control can be improved for end users, and highlight the opportunities Revolut Pay can create for merchants.

13:05 – Time for lunch

Did someone hear the dinner bell ring? Not exactly, but after a packed morning of panels and insights at MoneyLIVE, it’s no surprise the audience rushed toward the lunch tables.

Sessions resume at 14:20, and Payment Expert will be back to bring you the latest conversations and takeaways from the floor.

12:55 – Audience Question: Is loyalty fraud a growing problem?

An audience member asked whether loyalty programmes bring new fraud risks.

The speakers said yes, challenges do exist but there are solutions. Olerinskiy offered an example, where some customers buy bundle offers counted as loyalty deals and then return part of the bundle to exploit the system. In more extreme cases, he said, fraudsters even try to steal other people’s identities to access their rewards – these examples were not linked to Decathlon stores.

The panel agreed the key is to design loyalty programmes with no stealable benefit. Rewards should be converted or redeemed instantly, leaving nothing for fraudsters to exploit.

12:45 — Data, data, data

After exploring how data helps detect and prevent fraud, MoneyLIVE is now looking at how payments data can boost consumer loyalty.

Dmitry Olerinskiy, Digital Strategy Program Director at Decathlon, and Lucy Whittemore, SVP UK Partnerships at Cardlytics, discussed how transaction data reveals what customers do when they’re not shopping with you, offering a “full wallet view.”

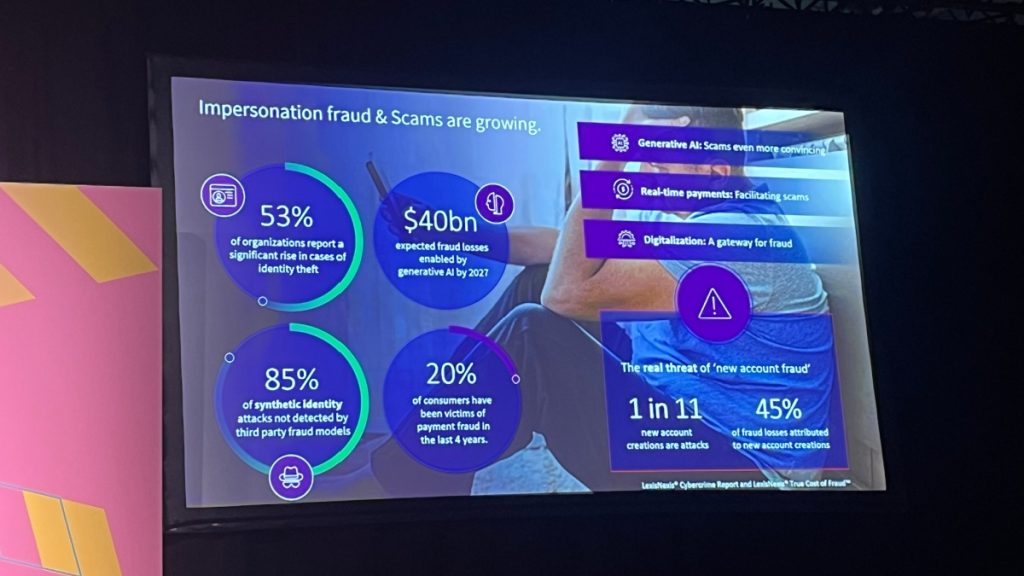

12:10 – Fighting fraud with AI

Jason Lane-Sellers, Director of Fraud and Identity at LexisNexis Risk Solutions, delivered some compelling insights on the fraud landscape. He revealed one in every 11 new account openings is an attack, often powered by AI. Fraudsters are now using generated scripts, AI imagery, synthetic identities combining images, voice deepfakes which take just 30 seconds to replicate, and even AI-driven adverts.

However, AI isn’t just a tool for bad actors, as Lane-Sellers explained companies can fight fire with fire. He said by analysing thousands of data points during onboarding, businesses can spot what AI can’t replicate, such as a person’s unique digital persona. Did they check the train schedule this morning? Interact with family? Small behavioural cues can help validate identity.

AI can also detect subtle differences in how people interact with their devices, including swiping patterns, typing rhythms and engagement with options like card personalisation. While genuine users explore choices, fraudsters often stick to defaults, giving away their intentions.

11:45 – Deepfakes aren’t funny anymore

Gunning said generating fake documents from scratch using generative AI hasn’t been a major issue, but biometrics are a different story. What used to be “laughable” is now high quality enough to worry banks.

Poon explained there’s no silver bullet to combat these threats, adding systems need multiple layers of checks, like examining image depth or whether videos are off balance. Regulatory expectations are also rising, with banks required to maintain robust controls against financial crime.

Banks can choose the technology they want, but Poon noted a key challenge is that AI decisions need to be explainable, which is not always easy when algorithms are involved.

11:35 – Tech is getting better, but it’s also getting cheaper

After a lively coffee break, the tone changed quickly as Simone Poon of Standard Chartered, Jamie Renehan of Bank of Ireland and Fourthline CEO Krik Gunning took the stage to tackle the rise of deepfakes.

Gunning compared today’s fraud techniques to “Mission Impossible” levels of sophistication, but Renehan warned the real danger is how accessible the tools have become. You can now buy advanced deepfake tech for less than €50, he said, meaning the barrier to entry has disappeared.

10:45 – Can Europe replicate Brazil’s success?

The conversation has shifted to alternative payment methods, which continue to surge globally, particularly in emerging markets.

Pix is the standout example. Now five years old, the system has become the backbone of payments in Brazil since its launch by the Central Bank in 2020. More than 150 million people use it, and in 2024 alone it processed 64 billion transactions worth $4.6 trillion.

Jeroen Kok, Head of Payments Netherlands at JP Morgan, said Europe’s progress looks “disappointing” by comparison, pointing to relatively small peer-to-peer volumes. When it comes to replicating the Pix model in Europe, “the devil is in the details,” he noted.

Uber’s perspective is that Europe’s challenge isn’t infrastructure but behaviour. Consumers need to be educated and incentivised to use new payment methods. In Brazil, Pix succeeded because it solved real problems for the underbanked.

10:30 – Uber takes a shot at banks

The stage is getting crowded for the final panel of this morning’s session, not that the speakers are complaining, as it means they can huddle for warmth.

Predicting the future is difficult, but with voices from Uber Pay, Standard Chartered, ING and JP Morgan, this panel may be as close as it gets.

The benchmark for modern payments is speed and seamlessness, with anything less than instant increasingly viewed as too slow. Divya Bhardwaj, COO of Uber Payments, said reaching that vision will require deep collaboration across the ecosystem, especially with banks.

In a slightly bold move given her fellow panellists, she flagged bank outages as one of the biggest obstacles to progress. Bhardwaj said she wants to see far greater investment in resilience if Europe is going to deliver the payment experience consumers now expect.

10:10 – Amazon: Why more choice isn’t always better

For the second panel in a row, the moderator kicked things off by asking the audience whether they’ve used the speaker’s product. Earlier it was Mercedes, this time it was Amazon. Unsurprisingly, far more hands went up, though as Mual joked, it might be because the payment point is a little lower.

William Olgiati, GM of Payment Acceptance and Experience for EU and the UK at Amazon, dived into how the company is working to improve the ecommerce payment journey. A big part of that comes down to partners. Many online retailers think the answer is to offer more and more payment options, but Olgiati argued diversification isn’t always the best route.

He said some payment methods in the EU “lack features customers expect naturally,” which means Amazon spends a lot of time helping partners improve their offerings.

When assessing new payment partners, he said there has to be a clear need and a genuine gap to fill. Amazon looks at whether the method brings higher approval rates, access to new customers, or whether it simply cannibalises existing options.

09:50 – Does losing your car mean losing your wallet?

Mélisande Mual, Managing Director and Owner of The Paypers, asked how do you stop a family member, or anyone else, using your in-car payments if they get behind the wheel?

Mual raised a great point…

Once, losing your wallet meant your payment details were exposed. Then it was your phone. Now, with cars becoming payment devices, the stakes have gone up again. The thing storing your card details is becoming a lot more expensive to misplace, not to mention the risk to your bank account.

Kersten reassured the room that Mercedes has already built in protections. Every driver gets their own ID, and most new models now include biometric verification. Mercedes is also rolling out facial recognition, because, as Kersten put it, it would be wrong to have a giant screen in the car and still ask the driver to verify payments on their phone.

“Can my wife fuel on my card? No, she can’t. Because we use biometric authentication.”

9:40 – Making the most of “smarthphones on wheels”

Nico Kersten, CEO of Mercedes pay, summed up his team’s role with a line that got the room smiling: “Imagine us as the fintech inside Mercedes-Benz.”

He described the automotive industry as being in the middle of a transformation, where buying a car now comes with the same digital expectations as buying a phone or laptop. Today’s vehicles are packed with software and screens, and drivers increasingly expect them to work just like the devices they use at home.

“It’s a smartphone on wheels,” Kersten joked, adding that services like charging, fuelling and parking all depend on seamless digital payments. Making that work, he said, requires combining automotive know-how with payments expertise.

9:15 – Digital wallets will shape Europe’s sovereignty push

Francesconi continued by highlighting why wallets will be critical to user adoption on Europe’s journey toward payment sovereignty. He pointed to high wallet adoption in mature markets.

Research from Finder shows around 40% of online transactions are now made via digital wallets in the UK.

He said Wero is preparing for expansion into new markets including Austria and is exploring collaboration with EuroPA in countries such as Italy, Spain and the Nordic region. The long-term goal is interoperability across local solutions to create a connected European payments ecosystem.

9:05 – Europe’s payments future begins with one wallet

Day one opened with Ludovic Francesconi, Chief Member and Strategy Officer at EPI Company, who set out the vision behind EPI Wero. The ambition is a single wallet for Europe, removing payment borders in the same way streaming or hotel booking already work across the continent.

Francesconi argued sovereignty is the main aim, with profits currently flowing to non-European providers, consumer data often sitting outside EU protections and the region having limited control over key payment infrastructure. “Why should payments stop at borders,” he said.

09:00 – We made it

Good morning readers, I’m Kieran O’Connor and I will be giving you live, instant reactions from the event. The weather may be grey and miserable outside, but it’s hard to notice once you step into the SugarFactory here in Amsterdam, a impressive, renovated industrial space. Some of the rooms are a little on the dark side, but judging by the speaker lineup, the insights today should shine a light on the future of payments.