The Bank of England has opened a consultation on a prudential regime for sterling-denominated systemic stablecoins and, in a companion paper, published the modelling it used to calibrate proposed retail and business holding caps.

The Bank of England has published a consultation on how it would regulate sterling-denominated systemic stablecoins, outlining backing, liquidity and transition rules as the UK prepares for stablecoins to sit alongside existing payment instruments.

The paper was published on November 10, 2025, with feedback due by 10 February 2026.

Under revised proposals, issuers would hold at least 40% of backing assets as unremunerated deposits at the BoE and up to 60% in short-term UK government debt. A “step-up” path would allow issuers recognised as systemic at launch, or moving across from the Financial Conduct Authority regime, to hold up to 95% in short-dated gilts initially, tapering to 60% as they scale.

The BoE is also considering a backstop lending facility for eligible, solvent issuers to reinforce resilience in stress.

To manage transition risks to bank funding, the BoE proposes temporary holding limits of £20,000 per coin for individuals and £10 million for businesses, with exemptions to accommodate the largest firms. The limits would not apply to stablecoins settling wholesale transactions in the Digital Securities Sandbox.

The BoE has also set out a methodology for assessing deposit outflows into digital money, which informed the proposed limits.

On supervision, non-systemic issuers remain under the FCA. If HM Treasury designates an issuer as systemic, it would move into joint regulation: the BoE leading on prudential and financial stability, and the FCA overseeing conduct and consumer protection.

The authorities plan to publish a detailed joint approach in 2026 to support smooth transitions between regimes.

The consultation maintains the BoE’s location policy: non-UK based issuers of sterling systemic stablecoins would need a UK subsidiary to issue to UK users and to hold backing assets and capital domestically, aligning with access to BoE deposit accounts and any liquidity facilities.

Sarah Breeden, Deputy Governor for Financial Stability, said the proposals are “a pivotal step towards implementing the UK’s stablecoin regime next year,” adding that they are designed to “support innovation and build trust” and give industry clarity to plan.

The BoE expects to consult on detailed Codes of Practice later in 2026, following review of consultation feedback.

The devils in the details

After pushback on the Bank’s 2023 idea of 100% unremunerated central bank deposits, the new proposal allows up to 60% of backing assets in short-term UK government debt, with at least 40% held as unremunerated deposits at the BoE to anchor par redemptions in both normal and stress conditions. Temporary deviations from the split could be permitted to meet large, unexpected redemptions. Issuers may lend securities via repos to raise liquidity but borrowing via repo is not allowed.

Issuers recognised as systemic at launch, or moving across from the FCA regime, could initially hold up to 95% in short-dated gilts, stepping down to 60% as scale is reached. The Bank is also considering a backstop central bank lending facility for eligible, solvent issuers to monetise those assets in stress.

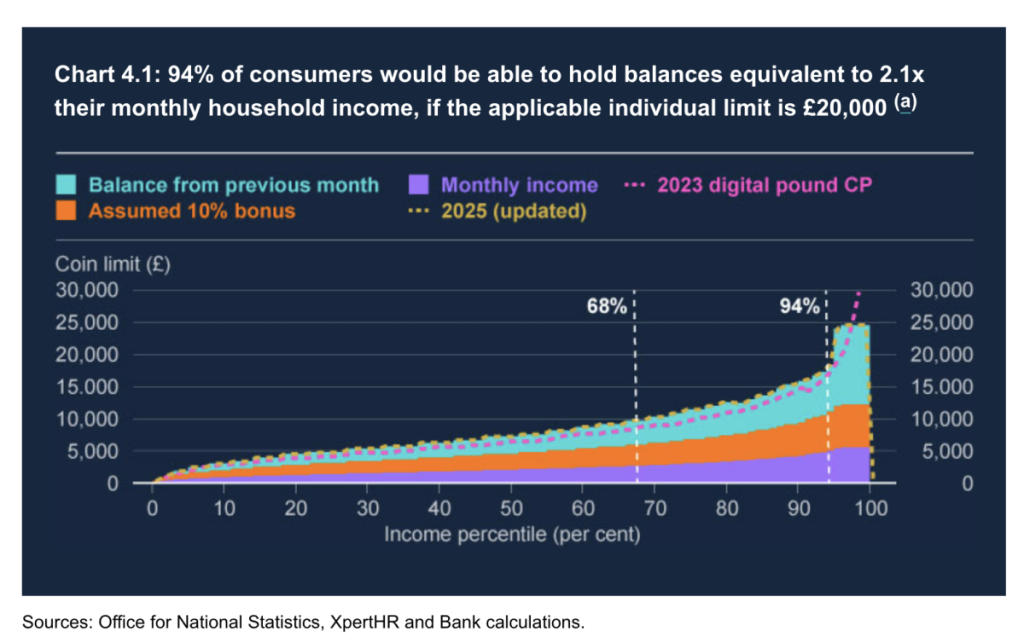

Holding limits: £20,000 per person, £10 million per business

To manage deposit flight during the transition to “multi-money” payments, the BoE proposes temporary caps of £20,000 per person per coin and £10 million per business, with exemptions for very large firms. Limits would not apply to wholesale settlement use in the Digital Securities Sandbox.

The consultation also invites views on alternative tools, including aggregate coin caps and transaction limits, and acknowledges the operational complexity of enforcing per-person limits across multiple wallets and smart contracts.

Supervision and custodians

The BoE expects to adapt its financial market infrastructure (FMI) supervisory playbook for stablecoin issuers and will publish a supervisory approach in 2026.

For custodial wallets, the BoE intends to rely on the FCA’s proposed custody rules (CASA-style safeguarding and segregation), reserving the option to regulate a custodian directly if HMT recognises it as systemic.

Inside the Bank’s holding-limits paper

The companion Financial Stability paper explains how the Bank quantified risks from a rapid shift of bank deposits into digital money during a severe, system-wide stress.

It models system liquidity under two stages: a baseline guided by observed outflows in March 2023 (SVB, Signature, First Republic, Credit Suisse), and a “severe illustrative” scenario with higher outflows driven by the ease and perceived safety of moving into digital money.

Key modelling assumptions

- Scope and starting point: The model looks at sterling deposits at a group of UK banks, incorporating conservative reductions in reserve levels to reflect quantitative tightening and TFSME repayments.

- Digital money uptake: Before stress, it assumes three sterling stablecoins and a potential digital pound together reach c.15% of sight deposits for individuals and businesses.

- Stress outflows: During stress, uninsured deposits are assumed to face very high outflow rates to digital money (around 75% for individuals, 100% for businesses), while insured deposits see smaller but material outflows (about 10% for individuals, c.40% for businesses). These rates are intentionally more severe than recent history to explore tail risk.

- No deposit recycling: For simplicity, the main results assume deposits leaving banks for digital money are not recycled back into banks via HQLA sellers, increasing pressure on banks’ LCRs. The paper notes that some recycling could occur, but would still worsen LCRs as retail deposits are replaced by higher-outflow wholesale deposits.

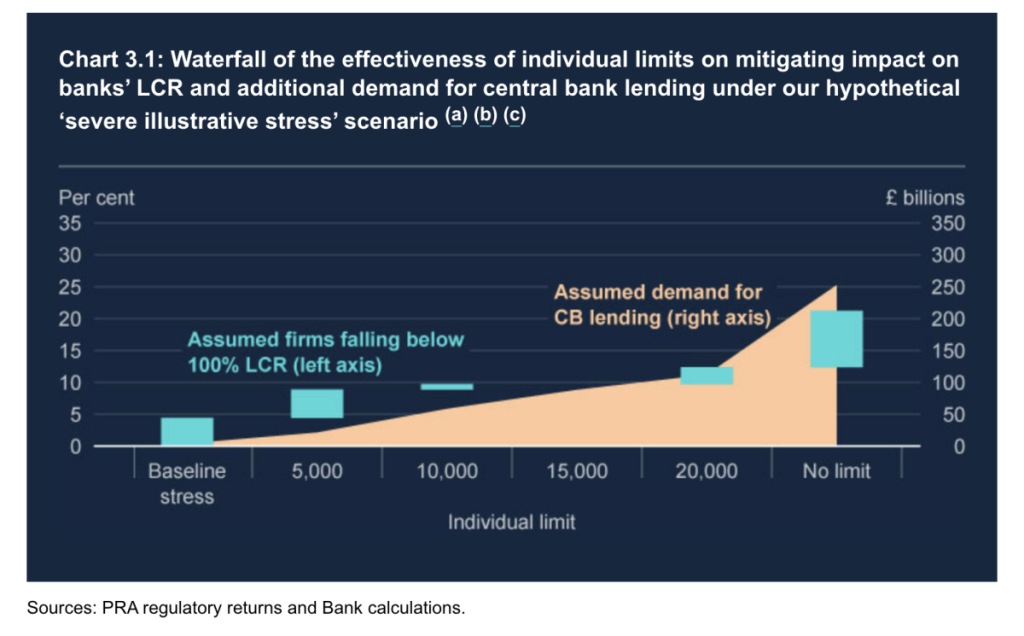

How limits change the picture

The BoE evaluates how different per-person caps affect three system metrics: the share of banks falling below a 100% LCR after using pre-positioned collateral, additional demand for central bank lending against collateral, and any residual shortfall.

Moving from £5,000 to £10,000 and from £10,000 to £20,000 increases risk, but the incremental change is smaller at higher caps. “No limits” produces substantially higher risk on all three metrics.