A stark earnings miss has jolted Fiserv into action as management bets that tighter execution around Clover and core platforms can steady margins and restore investor confidence.

“Our current performance is not where we want it to be nor where our stakeholders expect it to be.”

When a chief executive opens an earnings release with a line like that, the numbers that follow rarely soothe markets. Fiserv’s third-quarter figures did not. The company missed expectations, cut guidance, unveiled a sweeping leadership overhaul and said it will shift its listing back to Nasdaq.

Investors responded in kind, sending the shares down by more than 40% on the day.

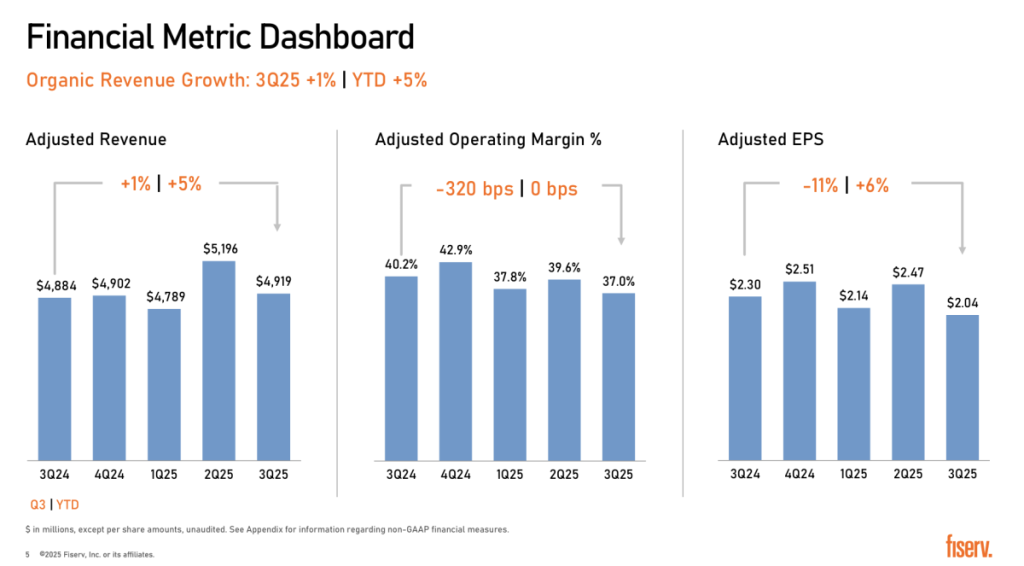

Beneath the mea culpa sits a thorough reset – on the headline figures, GAAP revenue edged up 1% year on year to $5.26bn, with GAAP EPS at $1.46. Adjusted revenue was $4.92bn, up 1%, and adjusted EPS fell 11% to $2.04. Adjusted operating margin compressed to 37%, down 320 bps.

Free cash flow was $1.3bn in the quarter and $2.9bn year to date. Management framed this as “resetting to a new financial baseline” of more recurring, higher-quality revenue.

Organic revenue growth was 1% for the quarter, with Merchant Solutions up 5% and Financial Solutions down 3% (about 1% down if you strip out periodic and licence revenue). This mix shift helps explain the margin pressure: merchant’s adjusted operating margin held in the high 30s, while Financial Solutions’ margin was materially lower than last year.

The forward view is where the knife really fell, however. Full-year organic revenue growth is now 3.5–4% and adjusted EPS $8.50–$8.60, down from roughly 10% organic and $10.15–$10.30 previously. That is a wholesale step-down in ambition and explains the market’s severity.

Execution, capital, and the “One Fiserv” plan

Fiserv insists this is not retrenchment but a re-prioritisation.

The company launched a “One Fiserv” plan with five pillars: client-first execution, scaling Clover into a pre-eminent small-business operating platform, building differentiated finance and commerce platforms including embedded finance and stablecoin, AI-enabled operational excellence, and disciplined capital allocation.

It paired that with visible balance-sheet work and M&A: $2bn of 5- and 10-year notes at a 4.90% coupon, an $8bn revolver, and deals for CardFree and Smith Consulting, plus a definitive agreement to buy StoneCastle Cash Management.

The merchant franchise is still the growth engine, with a fresh Canadian thrust through acquiring part of TD Bank’s merchant processing and a managed-services deal that broadens Clover’s footprint.

There are also nudges at product direction. CashFlow Central has quietly notched 96 wins since launch. The deck touts an SMB POS entry in Japan via a local partner. And in a bid to sit at the bleeding edge, Fiserv highlights “Roughrider Coin,” a state-backed stablecoin pilot with the Bank of North Dakota.

Individually small, collectively these are tells about where the company expects durable growth to come from.

People as the lever

Arguably the most striking part of the day was the simultaneous shake-up of the leadership bench. Paul Todd, who previously served as CFO of Global Payments, succeeds Robert Hau as CFO, who will serve as a senior advisor through the first quarter of 2026 to support a smooth transition.

Two co-presidents arrive on 1 December: Takis Georgakopoulos, Fiserv’s COO and the former head of JPMorgan Payments, and Dhivya Suryadevara, who ran Optum Financial and Optum Insight at UnitedHealth and previously served as CFO at Stripe and at General Motors.

“Takis, Dhivya, and Paul are joining a seasoned leadership team at Fiserv and have the skills and experience to lead critical strategic initiatives to position us for high-quality sustainable growth. We also have opportunities in front of us to improve our results and execution, and I am confident that these are the right leaders to help guide Fiserv to long-term success.” – mike lyons, CEO

All three are paired with a refreshed board, including Gordon Nixon as independent chair, Gary Shedlin as audit chair and Céline Dufétel as a new director from 1 January 2026. The official rationale is execution and long-term value creation, but the subtext is likely to be accountability for a sharper plan.

The market’s verdict

Investors did not wait for the execution narrative. The stock had its worst day in years after the miss and guidance reset, with major outlets pegging the drop at roughly 40–45%, making Fiserv the S&P 500’s biggest decliner.

The sell-off is rational if you believe this year’s earnings base is lower and the path back to double-digit organic growth is longer. It will also test the credibility of the “constant compounder” pitch that management reiterated in the deck.

Alongside the reset, Fiserv announced it will move its listing from the New York Stock Exchange to Nasdaq on November 11 and restore its old ticker, FISV. The company also plans to migrate seven bond listings.

The press release does not spell out the strategy, but two advantages are obvious. First, Nasdaq is the natural home exchange for large payments and software peers and can aid index inclusion and tech-sector peer visibility. Second, reverting to FISV restores brand and ticker continuity for long-time holders.