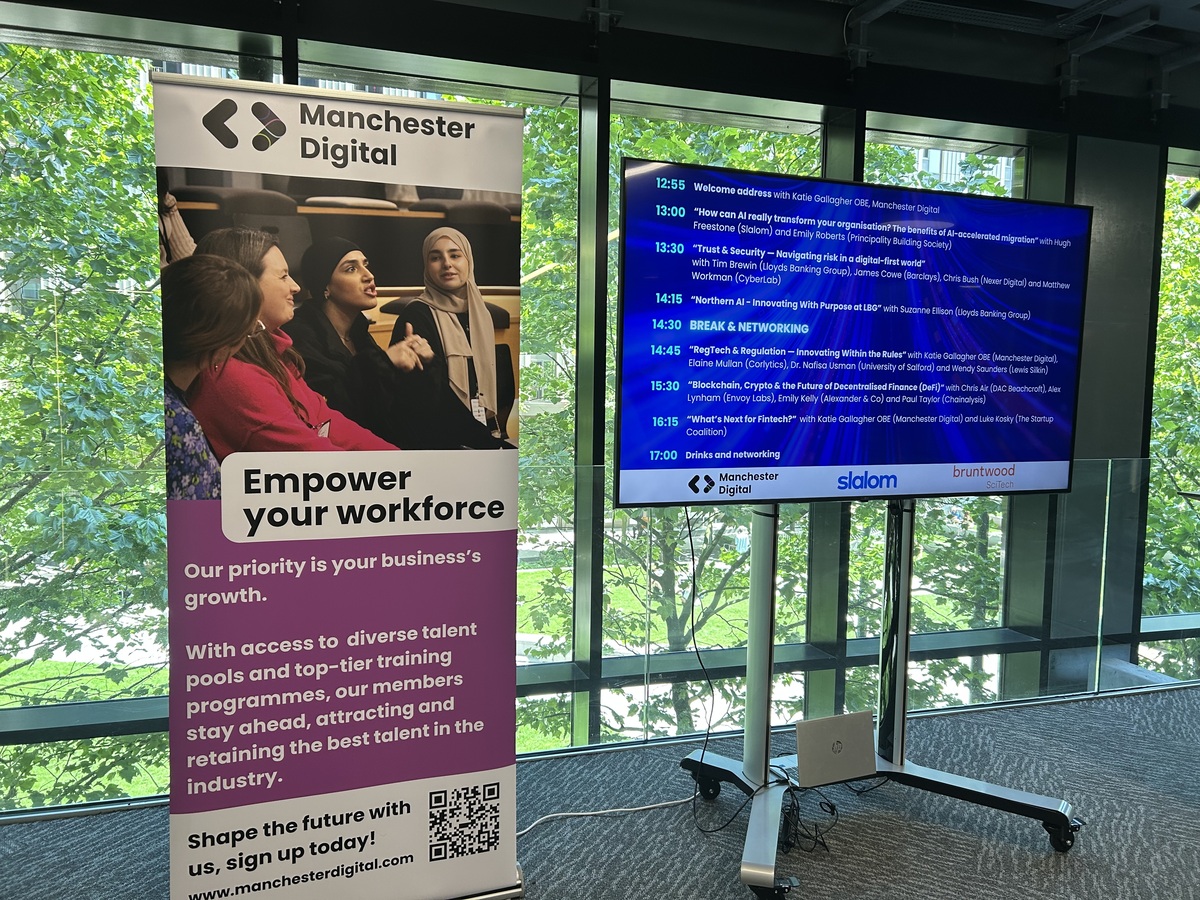

Artificial intelligence may not be a new concept in fintech, but its accelerating application across databases, customer support, regulatory compliance, and even regional development made it a dominant theme at this year’s Fintech Conference in Manchester.

Held on June 19, the 2025 edition brought together leaders from banks, tech firms, and consultancies to discuss the role of AI in modernising core systems, streamlining communication, and building consumer trust.

Here’s Payment Expert’s five key takeaways from the event:

- AI is transforming database’s

The opening panel saw Emily Roberts, Data Platform Lead at Principality, explain how the building society migrated its old, traditional database to an AI-powered solution which accelerated the integration process.

Roberts revealed a typical database transformation takes at least 18 months, but with the help of management consulting firm Slalom, this process took only seven months. This was in part due to the rapid capabilities of AI, in particular Agentic AI.

Principality now uses AI to automate minor updates within its database, having switched to a new language that allows AI agents to analyse customer data and relay the relevant information to another AI agent, which then extracts what’s needed for the company’s engineers.

Roberts noted stakeholders were initially concerned about the new AI database, but assured them human oversight would be present and ensure testing and reconciliation over the process.

“We wanted to use Slalom for new opportunities for the new platform,” said Roberts. “Stakeholders were concerned over reconciliation, wanting a human in the loop as a key part of the business case showing every change and transformation with testing done by engineer. Now we have a motivated engineering team to continue discovering AI.”

- AI is building customer trust

In another panel, industry participants discussed banks’ utilisation of AI when it pertained to customer usage and trust.

James Cowe, CTO at Barclays, believes when it comes to AI’s involvement within the banking space, “transparency is king” and detailed how Barclay’s is being upfront and open with its customers on how AI is helping to detect potential fraud attacks and serves as an overall protector to customers.

Matthew Workman, an Account Executive at CyberLabs, explained banks and financial services are turning to AI models to combat threats like fraud, not only because the technology itself has advanced, but also because fraudsters are using more sophisticated phishing tactics, prompting a faster and more efficient detection process in response.

But there are also instances of AI not working as efficiently as some banks and companies may have hoped for. Chris Bush, Head of Design at Nexer Digital, highlighted how a merchant like Booking.com began offering customers the option to engage with AI assistant chatbots, emphasising that providing choice is increasingly important for both users and the effectiveness of AI.

- Lloyds are developing Northern AI

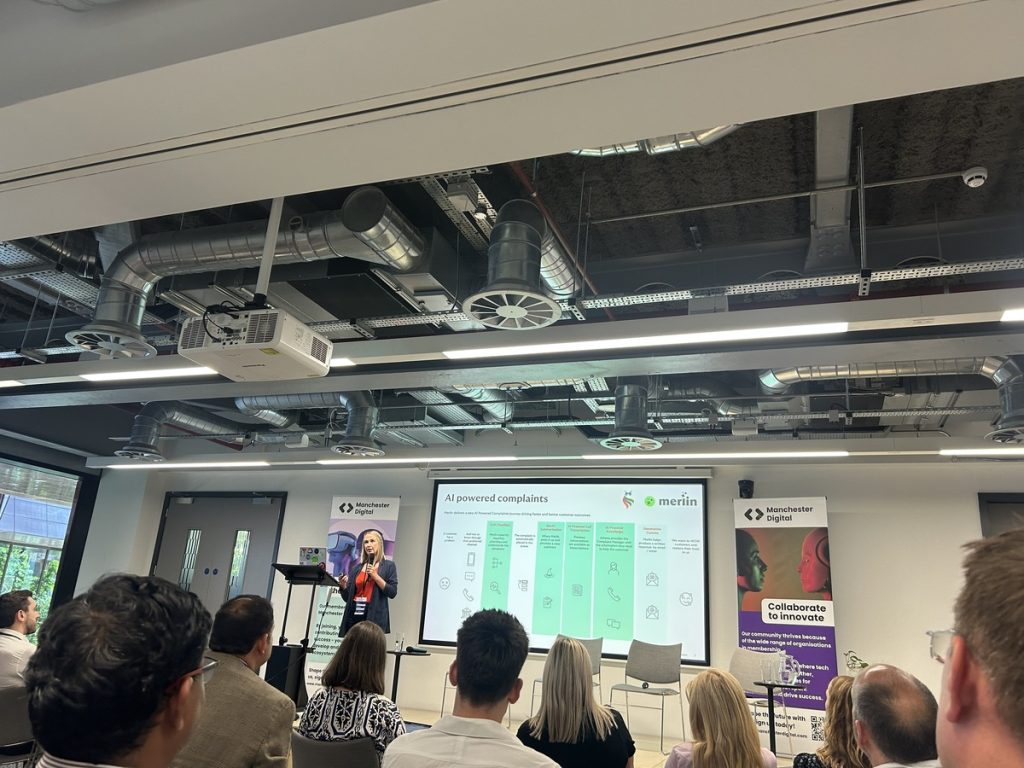

In response to Lloyd’s Bank developing a majority of its AI research and production in London, Suzanne Ellison, Head of Product at Lloyd’s shared how the bank is focusing on developing its own AI products in the north of England.

Ellison revealed in the last several years, the northern Lloyd’s AI team has grown from 120 people to up to 300 people, building out its own engineering team to launch two AI Agentic models, Athena and Merlin.

Athena serves to streamline how knowledge and data is shared across the northern Lloyd’s team that automates how colleagues retrieve information to better support its customers in the event of responding back to them with the relevant information.

Merlin is the “complaints wizard” Ellison described as the AI solution which helps balance the trust “make or break” from customers. Merlin helps guide customers in the right direction if they have a specific problem with automated responses from an AI chatbot, and also leverages its insights into what department to contact as it does not recommend solutions.

Ellison asserted Lloyd’s, particularly in the north, are heavily focused on consumer duty and its new AI solutions complement that push towards a more automated customer experience.

- Now is the time for RegTech adoption

In an evolving regulatory environment from country to country, where technology like AI is outpacing frameworks, is it now time that companies and policymakers make a new push for RegTech?

This was discussed by Elaine Mullen, Head of Marketing and Business Development at Corlytics, who stated “we’ve never seen anything like the evolution of financial regulation” as we have today, citing 159,000 regulatory notices on consumer duty since 2023.

With this in mind, RegTech has often been heralded as the answer to enable companies and policymakers to adapt quicker with the innovation occurring the fintech and payments space, with Wendy Saunders, Partner and Head of Financial Services Regulatory at Lewis Silkin, commenting on the calls from the UK to further adopt RegTech and create more engagement with the relevant sectors.

Dr. Nafisa Usman, a Professor at the University of Salford, explained that this can be achieved through a “compliance by design” model; bringing together engineers, regulators, and companies to share cross-sector knowledge and develop a regulatory framework that is both compatible with and achievable through the use of RedTech.

The UK has fostered innovation for RegTech through the launch of various digital sandboxes in recent years. These have enabled collaboration across key companies and regulators to develop more sophisticated RegTech models

- Crypto companies need to know about tax

In one of the closing panels Emily Kelly, Tax Senior Manager at Alexander & Co Chartered Accountants, revealed UK operating crypto companies will need to report their transactions to HMRC by 2027 or incur hefty fines.

This mandate from HMRC reveals more crypto companies should be aware of tax compliance of operating in the UK, which is included in the amended Crypto Asset Reporting Framework.