When Swedish payments firm Qliro announced its partnership this week with B2B fintech Two, the partnership promised ‘frictionless’ growth for merchants across the Nordic region.

But beneath the polished phrasing of the announcement lies something more consequential – the slow but steady transformation of how businesses buy from each other.

Long considered the dusty corner of commerce, B2B transactions are now being dragged into the age of instant credit and one-click checkout – and the Nordics are quietly leading the charge.

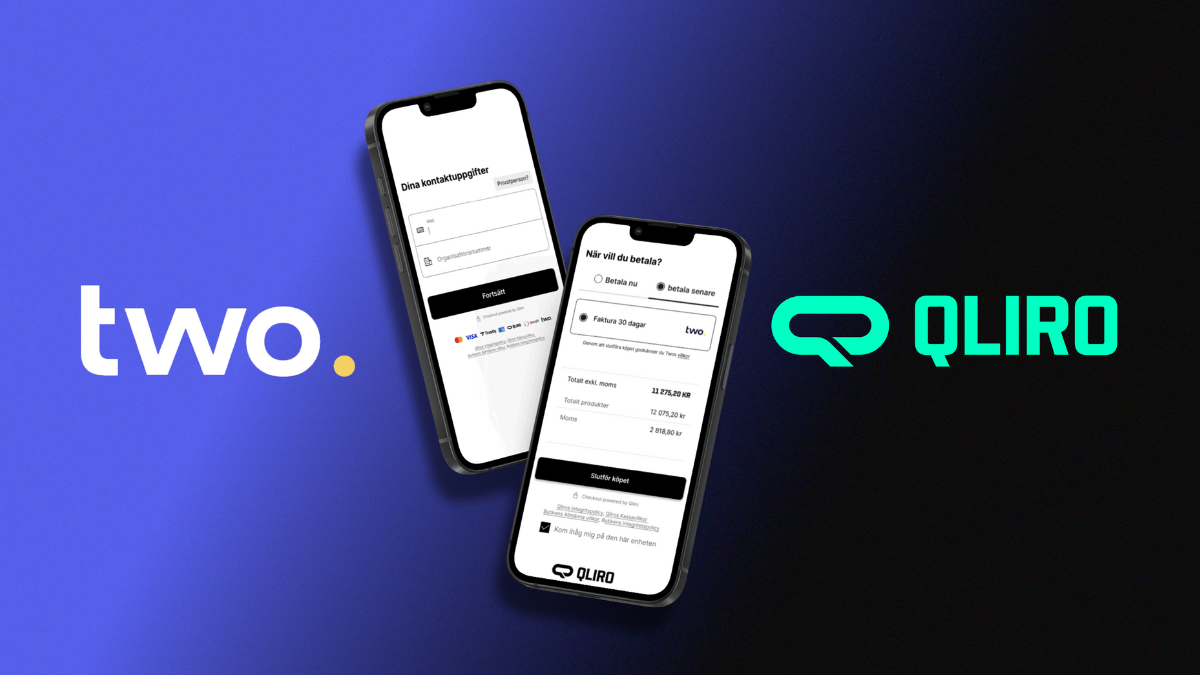

The partnership between Qliro and Two will see advanced B2B Buy Now, Pay Later (BNPL) functionality embedded directly into Qliro’s existing e-commerce checkout. While BNPL has become ubiquitous in the consumer space – driven by the likes of Klarna, also born in Sweden – this move brings the same flexibility to small and medium-sized businesses (SMEs) buying from online merchants.

With the integration, merchants can now offer business customers 30, 60 or 90-day payment terms at checkout without taking on credit or fraud risk. Two’s platform enables this by handling real-time credit decisions, verification and underwriting, while Qliro continues to serve as the front-end facilitator.

According to Two’s CEO and Co-Founder Andreas Mjelde, the goal is “to give Nordic merchants a powerful tool to serve both consumers and businesses – seamlessly”.

The BNPL Boom Spills into B2B

If consumer BNPL was the first wave, B2B is shaping up to be the second – and potentially more lucrative – one.

Businesses have long operated on invoicing and net terms, but those systems are clunky, risky, and slow to scale. BNPL options like Two, Billie in Germany, and Resolve in the US, aim to digitise and de-risk that process entirely.

According to data from Allianz, the global B2B BNPL market is expected to reach a gross merchandise value of $669.5bn by 2029, growing 24.7% annually. The momentum is especially strong in digitally mature regions like the Nordics, where SMEs are increasingly turning to flexible payment tools to simplify procurement and cash flow.

Christoffer Rutgersson, CEO of Qliro, frames the partnership as a merchant growth play.

“We’re enabling frictionless access to enterprise-grade B2B payments with no extra intervention required,” he said.

Why the Nordics are the perfect test bed

There’s a reason this innovation is coming from the Nordics. The region has long been ahead of the curve in fintech adoption, boasting a population comfortable with digital banking, mobile wallets and seamless online experiences.

Traditional credit card penetration is relatively low, especially among businesses, creating room for BNPL to thrive.

Moreover, many Nordic SMEs operate across borders within the EU, making streamlined digital payment options even more essential. Qliro already serves hundreds of merchants in the region, and its checkout is familiar to consumers and retailers alike.

By embedding Two’s capabilities, it is now positioned to capture the growing overlap between B2C and B2B commerce – where businesses act more like individual consumers in how they research, browse and buy.

Efficiency or overextension?

But not everyone is sold on the promise of frictionless finance. B2C BNPL has faced increased regulatory scrutiny over concerns of encouraging unsustainable debt, particularly among young consumers, who are one of the largest demographic adopters of BNPL.

While businesses operate under different financial dynamics, there’s a parallel risk in pushing credit to SMEs who may already face cash flow volatility or delayed receivables.

The Qliro-Two model seeks to address this by having Two assume all the credit and fraud risk – merchants get paid upfront while Two takes on the underwriting. It’s a clever workaround, but whether it can scale profitably across markets remains to be seen.

Analysts have also questioned whether BNPL truly leads to sustainable growth, or simply inflates average order values without long-term retention. For now, the companies are focused on capturing momentum – more than 100 new merchants joined Qliro in 2024, and both firms see SMEs as a key growth segment going forward.

A glimpse into the future of digital trade

For Two, the partnership with Qliro is part of a broader European extension strategy. Already backed by major financial institutions like Santander, ABN AMRO and Allianz, the company is positioning itself as a next-gen infrastructure provider for B2B payments.

Its goal is to make net terms as easy and instantaneous as card payments, without the risk or administrative drag. If it succeeds, the implications go well beyond the Nordics.

A frictionless B2B checkout – with real-time credit, embedded finance and invisible underwriting – could become the new norm across Europe’s €7trn SME economy.

In the meantime, the Qliro-Two alliance offers a glimpse of that future. One where businesses don’t fill out long forms or wait for invoicing cycles, but instead click, confirm, and pay later – just like consumers already do.