The UK’s Treasury may be required to prevent businesses from refusing to accept cash transactions should cash acceptance continue to decline, according to a new report from the Treasury Committee.

Published today (April 30), the Treasury Committee has laid out its recommendations to limit the decline of ‘cash acceptance’ within British businesses and communities.

The Committee recommends HM Treasury establish a system to monitor cash acceptance levels across the UK and report annually to Parliament. It should also define what constitutes a tolerable level of cash acceptance, in order to pre-empt widespread disadvantage or exclusion.

The Committee based its recommendations on evidence and feedback provided by government institutions of HM Treasury and the FCA. Additional business and community insights were provided by the Post Office, LINK, Age UK, Money and Mental Health UK, UK Finance and Consumer Scotland.

Many factors of Cash Usage decline

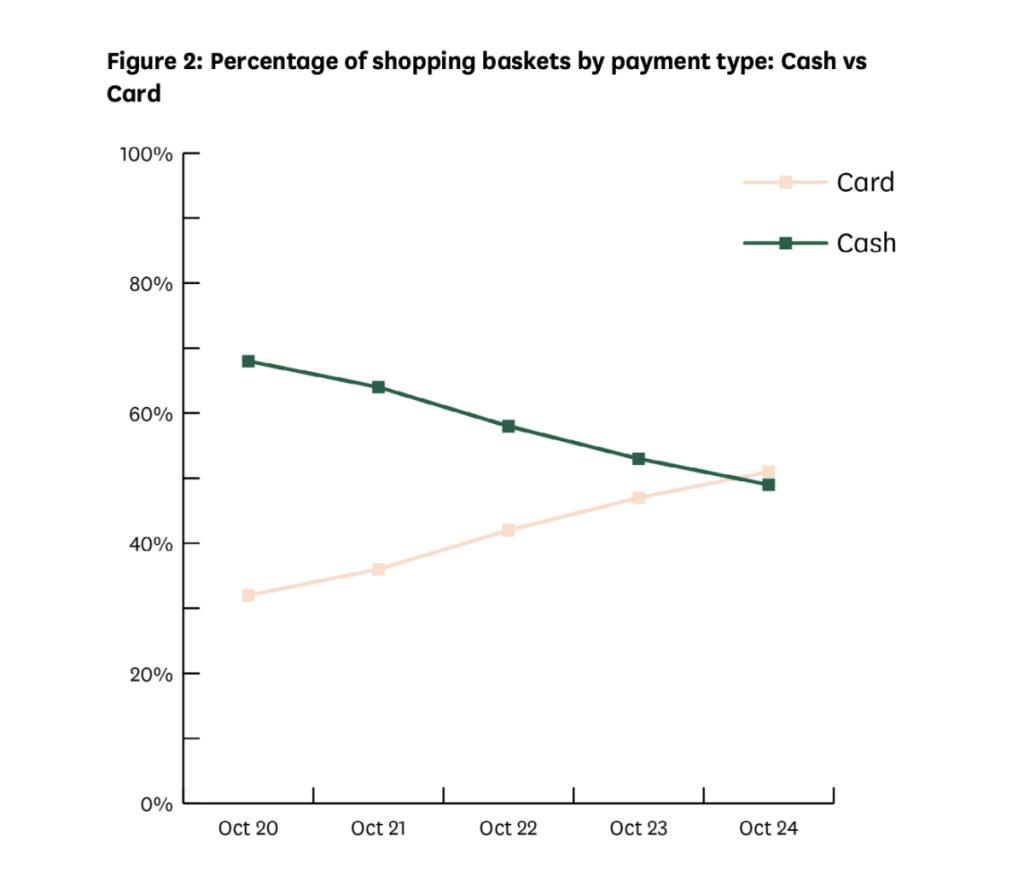

Evidence provided by UK Finance in today’s report indicates cash usage in the UK has declined significantly since 2013, when it accounted for 51% of all payment transactions. Mirroring other major economies, Britain has seen a double-digit drop in the use of cash, as consumers switch to digital payment alternatives.

However, this decline accelerated in the 2020s. The number of cash payments decreased by 7% from 2022 to 2023, totalling 6 billion transactions.

As the Committee notes, “letting physical cash decline in an unmanaged way by not addressing the issue of acceptance may lead to future costs.”

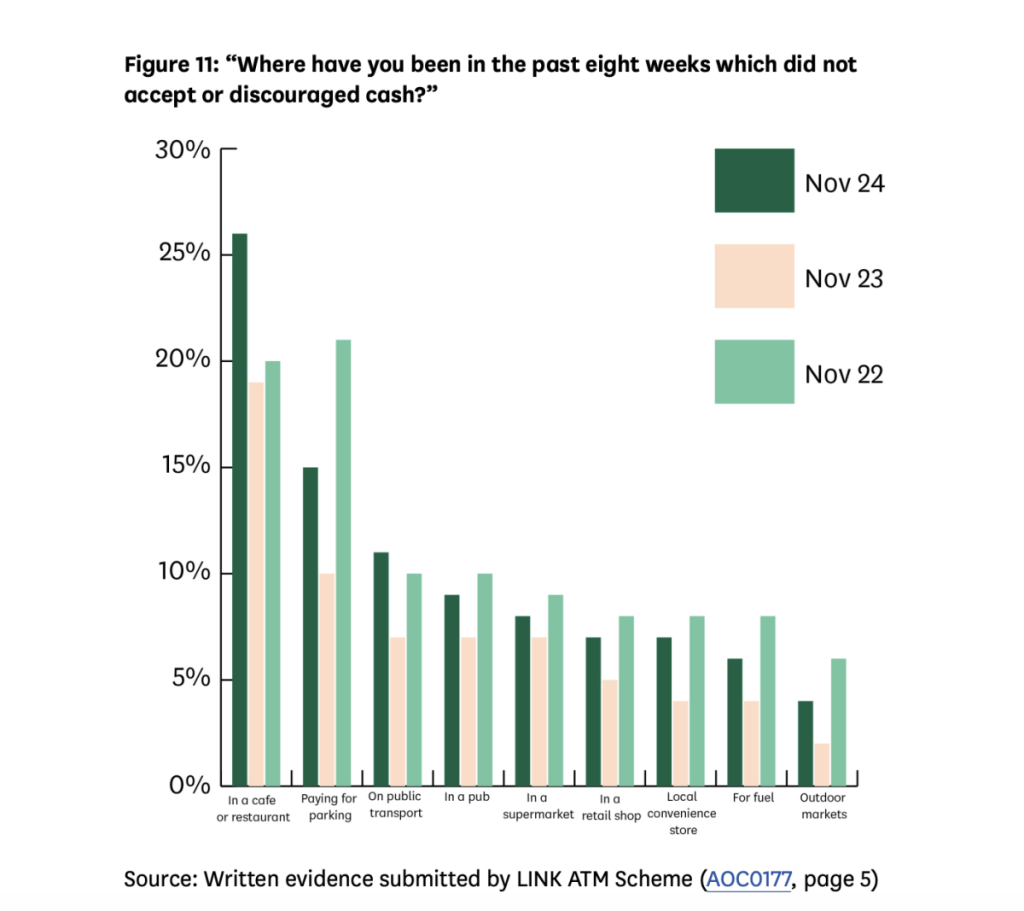

While the UK’s shift towards digital payments is evident, cash continues to play a crucial role for unique groups in society. Demographic data referenced by the FCA Lives Survey included in the Treasury’s report shows that approximately 1.1 million UK adults now primarily use cash for their daily spending up from 900,000 in 2022 – a rise due to budgeting needs during the ongoing cost-of-living crisis.

Financial authorities acknowledge cash remains the second most frequently used payment method in the UK, after debit cards.

According to a 2024 report from UK Finance, in 2023, cash machines accounted for 91% of all cash acquisitions, with approximately 1.3 billion cash machine withdrawals, totalling £114 billion. This represents a slight decrease in volume but a 1% increase in value from the previous year.

Protecting vulnerable communities

The Treasury Committee’s latest report identifies older people (particularly those aged 70 and above), individuals with disabilities, and those with learning difficulties as particularly impacted by the decline in cash.

Cash limitations further hinder social mobility in low-income communities and affect the estimated 1.1 million adults in the UK who remain unbanked. Additional concerns include barriers to escaping domestic abuse and the marginalisation of people with mental health issues.

In one example cited in the Treasury Committee’s report, a participant from a roundtable of individuals said, “you don’t know how much you spend with online banking,” highlighting how cash provides control and clarity that digital methods may lack.

Another contributor stated, “cash is a means for [victim-survivors] to escape an abuser, especially when that abuser can track them through a bank account.”

Recommendations on relevance of cash

To address the ongoing decline in cash acceptance and the associated risks to vulnerable groups, the Treasury Committee has made a series of key recommendations.

The Committee suggests that if current voluntary measures fail in maintaining adequate levels of cash acceptance, the Government should consider introducing legislation to require businesses—particularly those providing essential goods and services—to accept cash payments.

Recognising that some groups are especially reliant on cash, the report emphasises the importance of designing policies that do not leave specific populations behind as society transitions further towards digital finance.

Australia is cited in the report as an example jurisdiction where laws now require essential retailers to accept cash. The Committee believes the UK should learn from such models and explore similar protections for cash users.

As stated in the report, “protecting both access and acceptance would create a virtuous circle, allowing businesses, consumers and wider society to continue to enjoy the benefits of cash.”

Finally, the Committee endorses the expansion of physical cash infrastructure, including banking hubs and shared services, to ensure that access to cash remains practical and convenient for all individuals, especially in rural or underserved communities.

The report concludes by warning UK authorities and financial stakeholders that the continued decline in cash acceptance risks creating a “two-tier society where people who use cash are disadvantaged.”

It urges the Government to act swiftly to ensure that cash remains a viable and inclusive option for all communities.