In the second of a three part deep dive for Payment Expert, Patricia Carolina Ramirez Arriaza, PhD student at University of Mariano Gálvez in Guatemala and Michel Reznik, Partner at Estudio Legal Bernal in Mexico, examine Open Banking in Mexico and Guatemala.

The two regions have complex regulatory frameworks, of which have had a significant impact on the growth of Open Banking, with the tech not yet implemented in Guatemala.

Country Focus 3: Mexico

In Mexico the concept of Open Banking was ratified in Article 76 of the Fintech Law (Ley para Regular las Instituciones de Tecnología Financiera) which was implemented by 2018. The initiative of Open Banking has been driven by national regulatory bodies, which has included the Mexican Securities Authority (Comisión Nacional Bancaria y de Valores), Ministry of Finance, Public Credit (Secretaría de Hacienda y Crédito Público) and the Central Bank of Mexico. There is a separate body of data protection laws that apply, predating the Fintech Law, which have to be accounted for.

The Central Bank of Mexico issued a Circular 2/2020 which has clarified the model of Open Banking in Mexico and focuses on exchange of data, aggregation and transactions. However, essential regulatory instruments are still missing for a complete implementation of open banking:

- Secondary legislation in the form of dispositions is expected in relation to the Fintech Law, focusing on Open Banking and specifically transactional and personal data. The only disposition available today is in relation to open data which is public that relates to cash withdrawal points (like ATMs) in Mexico (such as location and types of currencies they provide).

- Public APIs are understood to be currently in the process of being produced by the Mexican Banking Association.

Due to these missing elements, adoption and implementation has, however, been slower than what it could have been. Another factor is that the Fintech Law is ambitious and overarching. Once the missing elements are in place, there is an expectation that the ‘big-tech’ organisations will advance to enter the market.

It is further expected that the Open Banking model will expand to other verticals which are prominent in Mexico, such as telecommunication and utilities.

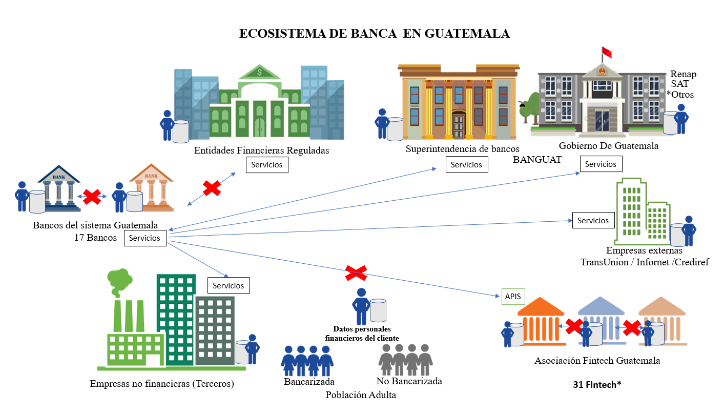

Country Focus 4: Guatemala

At present, Guatemala has not implemented Open Banking in any form and does not make use of any public APIs. The banks and institutions in the local financial system exchange data, are held in a very limited manner, through private APIs.

As such, Guatemala is an appropriate example of how a financial ecosystem operates prior to the implementation of Open Banking and demonstrates the respective inefficiencies as well as elements which it does not have, yet could have if Open Banking was implemented.

The potential, however, of Open Banking in Guatemala is clear as the country today has 17 banking entities (a number which has been stable since 2013) and 31 FinTechs (a number which has grown from zero in 2013 and is growing exponentially).

This does not account for other verticals that could be included in Open Banking and Finance. The breadth of participants in the market presents an opportunity for Open Banking to revolutionalise the financial system and bring with it all the benefits that are associated with Open Banking.

Initiatives are slowly emerging to enable Open Banking through public APIs and Guatemala has the benefit of hindsight of how the other countries in Latin America have done it in order to implement it effectively.