The FCA intervention against EES is the latest sign of tougher enforcement across the payments sector over financial crime.

The UK’s Financial Conduct Authority (FCA) has ordered Euro Exchange Securities (EES) to stop providing electronic money and payment services.

The financial watchdog said it had found significant risks linked to financial crime, as well as weaknesses in EES’ safeguarding arrangements, ownership structure and governance framework.

Founded in 2007, EES operates as an electronic money institution offering international payments, multi-currency accounts, currency exchange services and payment products for consumers and businesses.

As part of the intervention, announced on 5 June, the Court has named Duncan Perring and James Bennett of Teneo Financial Advisory as interim managers to temporarily lead the company.

The action was taken under the Payment and Electronic Money Institution Insolvency Regulations 2021, with EES set to appear before the Court on 11 June.

At that hearing, the Court will decide whether to lift the current order or place the firm into special administration.

Why the FCA took action

The FCA said “serious concerns” about the way EES was operating led to the intervention, pointing to what it described as significant financial crime risks across the business.

According to the regulator, these risks were caused by weaknesses in EES’ controls around financial crime prevention, safeguarding of customer funds and internal governance. Those issues affected how the firm monitored transactions, assessed clients and separated customer money from its own operations.

EES operates in both the US and Spain, and the FCA has applied for UK proceedings to be recognised by US authorities.

In filings submitted in the US, the regulator raised concerns about the “high-risk nature” of parts of EES’ customer base, as well as alleged “widespread breaches” of anti-money laundering requirements.

/ Shutterstock.com

According to reports, the FCA also said companies connected to EES’ wider network, as well as some of its clients, had been linked to money laundering activity or failures to prevent it.

The FCA’s enforcement comes amid a wider global tightening of enforcement in the payments sector, where regulators have targeted firms with cross‑border exposure and complex client structures.

One of the most well-known cases was in 2023, when Binance agreed to a $4.3bn (£3.22bn) settlement after US regulators found AML and sanctions‑screening failures across its global payments and trading flows.

What happens next?

The Court hearing on 11 June will allow EES to respond to the FCA’s concerns and the restrictions currently placed on the business.

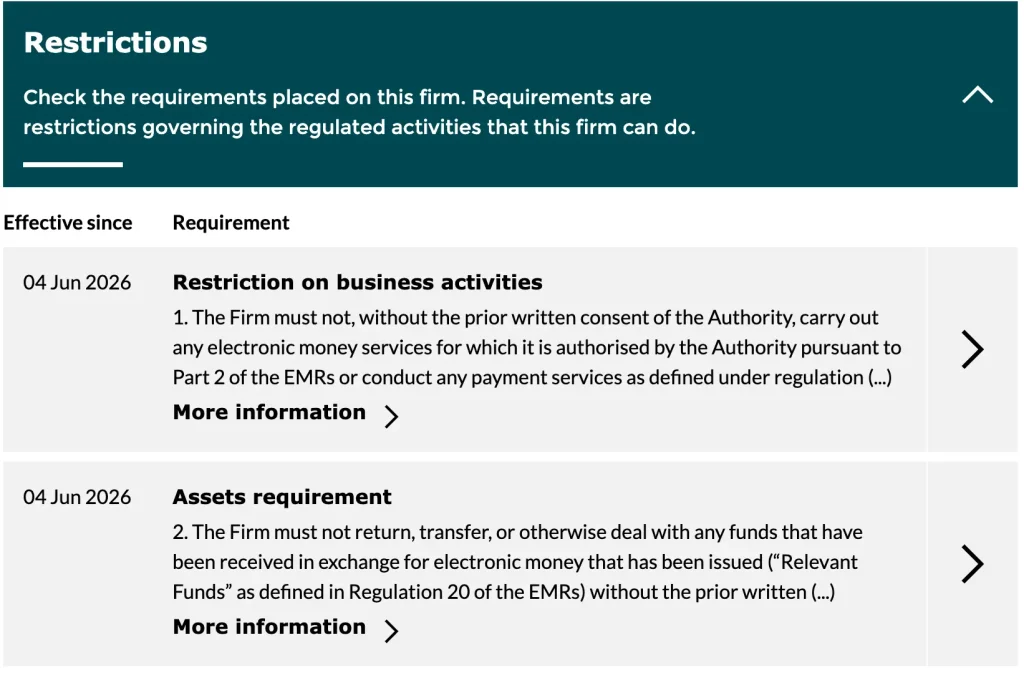

At the moment, the firm is not allowed to carry out any electronic money or payment services without prior FCA consent, including onboarding new customers or accepting additional funds from existing clients.

EES is also prohibited from returning or transferring customer funds without approval, with all relevant balances required to be ringfenced in designated safeguarding accounts.

Additionally, the firm must appoint an independent third party, approved by the FCA, to oversee the process of returning customer funds. Any redemption requests will only be processed where customer due diligence has been reviewed and verified to the satisfaction of an independent overseer.

The Court-appointed interim managers from Teneo Financial Advisory have taken temporary control of the company. Their role is to supervise EES’ operations, assess its financial position and support the safeguarding and return of client funds where possible.

At the upcoming hearing, the Court will decide whether the current order should be lifted or whether EES should be placed into special administration.

Special administration applies to payment and electronic money firms, differing from standard insolvency because it prioritises the protection and return of customer funds.

If imposed, administrators would take control of EES, focusing on safeguarding client money and assessing whether any part of the business can be restructured or wound down in an orderly way.