JPMorgan Chase, Bank of America, Citi and other US banks make move to connect traditional payments with tokenised rails

According to the Wall Street Journal, a number of the US’ major financial institutions are planning a joint tokenised deposit network. Thee network will be operated by the Clearing House, the real-time payments company co-owned by JPMorgan Chase, Bank of America, Citigroup, Wells Fargo and other major US commercial banks.

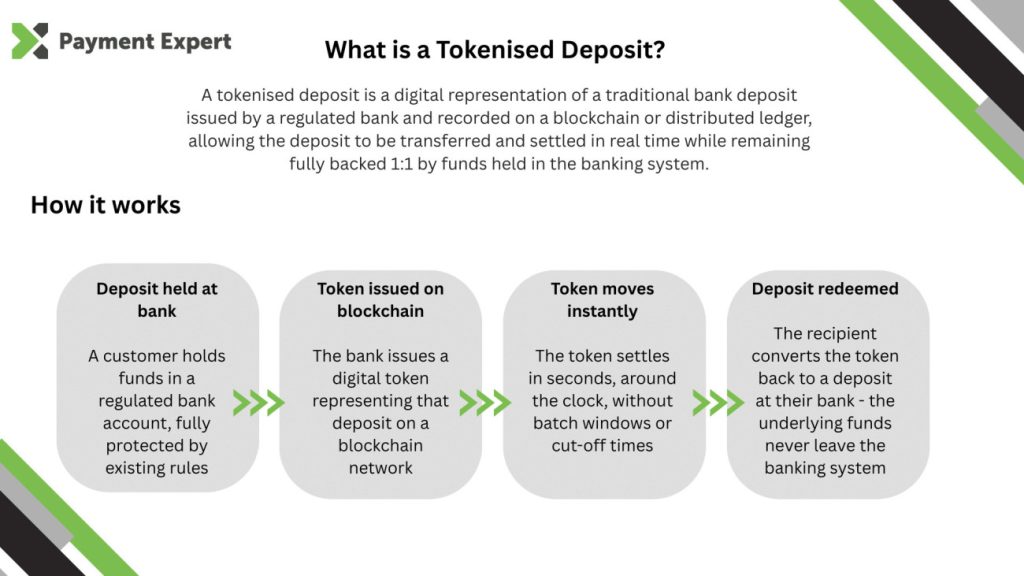

The system would connect traditional payment rails with blockchain infrastructure, aiming to enable instant, 24/7 settlement with a target launch in the first half of 2027.

This would allow tokenised deposits to settle across blockchain technology around the clock, removing the delays and cut-off windows that are a thorn in the side of much of the existing payments infrastructure.

Programmable treasury operations, real-time liquidity management and cross-border payments are expected to be among the network’s primary use cases. However, there are still a lot of details to be confirmed ahead of its introduction, including the selection of a third-party blockchain vendor to power the network.

Banks on the defensive

Since President Donald Trump returned to office in January 2025, his administration has been on a mission to make the US the crypto capital of the world.

This focus has added to the tension between banks and crypto firms, particularly around stablecoins, as issuers start to encroach on the deposit base that banks have controlled for such a long time.

The same scene is being played out around the world. Project Agora, the BIS-led initiative involving central banks and commercial institutions across seven currency areas, is testing whether tokenised money and programmable settlement can address inefficiencies in the banking system.

Speaking at a Bank of Japan seminar in April, BIS General Manager Pablo Hernández de Cos acknowledged the technological appeal of stablecoins while identifying the limits of their role.

While stablecoins offer features that can enable integration with smart contracts and faster cross-border payments, he said, the market is still small and structural features constrain what he called their “moneyness”.

Stablecoins vs tokenised deposits

The rivalry between stablecoins and tokenised deposits was a discussion point at a Money20/20 panel earlier this week, where industry figures shared their thoughts on the landscape.

Iana Dimitrova of OpenPayd lauded the ability to live cross-border transactions converting sterling into stablecoin and into local currency, including Mexican peso and Brazilian real, in under 40 seconds.

“The benefits in terms of cost and speed, and now security and traceability, have been proven,” she said. “It is now a matter of adoption.”

The bigger prize, the panel suggested, lies with tokenised deposits. Done properly, they could eliminate the collateralisation burden that stablecoins carry while freeing up liquidity that the current settlement system keeps locked away.

The idea of stablecoins and tokenised deposits as rivals, however, is not really correct. Bank of America indicated an appetite for stablecoins last year, but said it was waiting for the right regulatory framework before getting started.

In Europe, Qivalis, a consortium of 37 banks, is targeting the launch of a regulated euro-denominated stablecoin in the second half of 2026, with use cases including treasury operations, cross-border payments and financial market settlement.

Carl Grimstad, CEO of Lydian and a payments industry veteran with 25 years of experience, said the announcement suggests that the debate over blockchain’s place in finance has moved on.

“The largest US banks planning a shared tokenised deposit network is a clear sign the conversation has moved beyond whether blockchain belongs in finance,” he said. “These big institutions aren’t asking that question anymore – they’re reacting to where value is already moving.”

Grimstad argued that the harder problem is not creating another tokenised asset, but building infrastructure capable of moving liquidity across an increasingly fragmented mix of bank ledgers, public chains and digital assets.

“It’s not a payment problem we’re facing. It’s a translation problem,” he said.

Grimstad added that while tokenised deposits represent a meaningful step forward, the firms best positioned to lead will be those building the connective layer between traditional finance and the digital asset economy. “In a multi-ledger world, interoperability is the product.”