Operators are rethinking payments as a core commercial lever, with conversion, localisation and speed now directly impacting growth and retention

Payments are no longer treated as a back-end function, but as a direct driver of revenue, as operators face rising customer expectations, increasing localisation demands and tighter regulatory scrutiny.

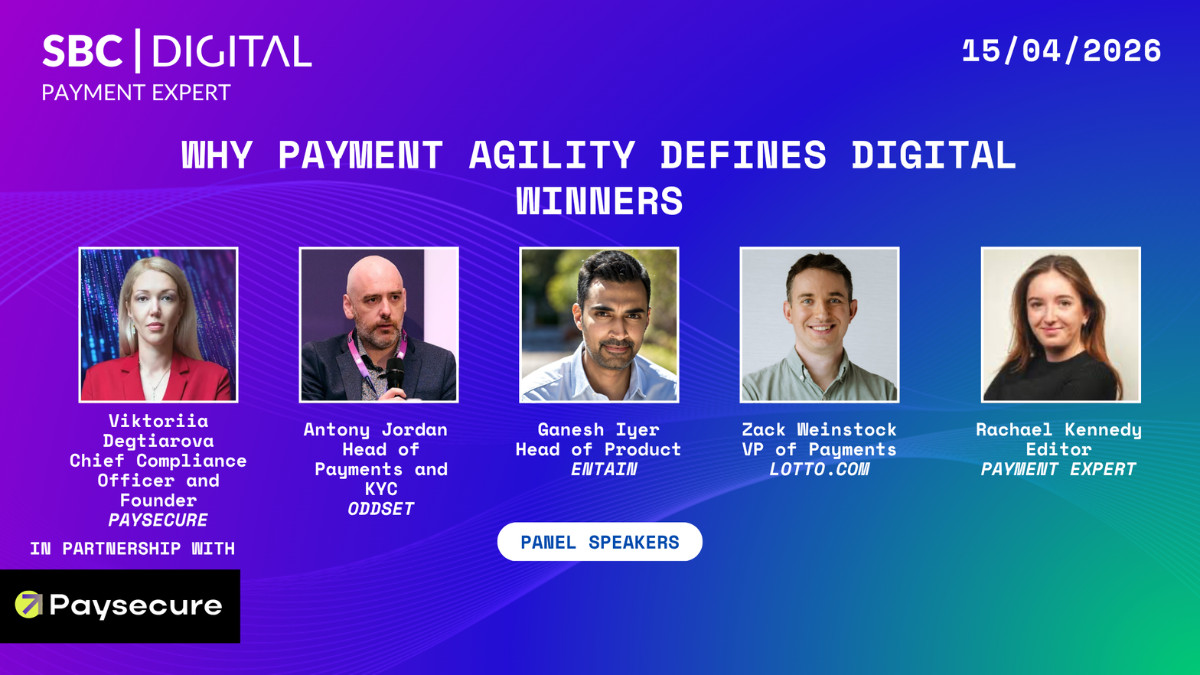

Speaking during Payment Expert’s Digital Day on 15 April, panellists from across the iGaming ecosystem pointed to a structural shift in how payments are viewed, moving from operational necessity to commercial differentiator.

Ganesh Iyer, Head of Product at Entain, described payments as having “moved from being a back-end thing to a top-line revenue optimisation cost”, highlighting how the function now directly influences both conversion and profitability.

This shift, he explained, has been driven by three converging factors: rising player expectations around speed and simplicity, the fragmentation of payment methods across markets, and a tightening compliance environment that leaves little room for error.

Conversion under pressure

For operators, the commercial impact is becoming harder to ignore.

Viktoriia Degtiarova, Co-Founder and CCO of Paysecure, pointed to the increasing cost of acquiring customers as a key pressure point, noting that in some markets acquisition costs can reach several hundred dollars per user. In this context, payment performance is no longer marginal. Conversion rates across the deposit journey, from registration through to repeat transactions, are now closely tied to how effectively payment systems are configured and optimised.

“The conversion is extremely important,” she said, adding that performance at the checkout stage has become a critical determinant of whether operators can recoup acquisition spend.

Zachary Weinstock, VP of Payments at Lotto.com, reinforced this point from a US perspective, noting that introducing new payment methods can deliver an immediate uplift.

“When we’re staying at the forefront adding new payment methods, we see a quick bump in our conversion rate immediately,” he said, pointing to customer demand for speed and convenience as a key driver of that behaviour.

Localisation moves from optional to essential

Alongside conversion, localisation has emerged as a defining factor in payment strategy.

Iyer highlighted the growing dominance of market-specific payment methods such as Bizum in Spain, Interac in Canada and Pix in Brazil, arguing that failure to support these options effectively excludes operators from those markets.

“Not having these methods, it’s almost like you’re not operating there,” he said.

Degtarova echoed this view, noting that cards are no longer the default in many regions and that open banking and local alternatives are becoming fundamental to the payment mix.

“The role of local payment methods has changed significantly. They became fundamental,” she said.

This shift has added layers of complexity to payment infrastructure, requiring operators to manage multiple providers, routing strategies and performance metrics across jurisdictions.

Speed as a competitive differentiator

As payment complexity increases, speed of execution is emerging as a key differentiator. Panellists broadly agreed that the ability to introduce new payment methods or enter new markets quickly can have a direct commercial impact, particularly in competitive or fast-moving regions.

Iyer suggested, in an ideal scenario, operators should be able to integrate new payment methods within weeks rather than months, while Degtarova argued that delays in responding to market or regulatory changes can result in lost revenue.

Anthony Jordan, Head of Payments and KYC at ODDSET, linked this directly to competitive positioning, warning that customers will quickly switch to alternatives if expectations are not met.

“If you don’t have the payment methods that people want, if you’ve given them the experience they want, then they will go somewhere else,” he said.

Despite the growing importance of payment agility, operators continue to face structural challenges in delivering it. Legacy systems, internal silos and resource constraints were all cited as barriers, alongside the complexity of integrating new payment methods across fraud, compliance and customer experience layers.

Degtarova pointed to organisational alignment as a particular issue, with payment initiatives often requiring coordination across risk, finance and technology teams. Weinstock added that implementation costs and competing priorities can slow progress, even where the commercial case is clear.

At the same time, Iyer cautioned that payment transformation is often underestimated, with integrations involving far more than a simple API connection, spanning fraud controls, compliance requirements and user experience considerations.

As operators push for greater flexibility, the need to balance agility with control remains a central challenge. Jordan noted that expanding payment options increases the burden on compliance and risk teams, particularly in regulated markets where new methods require approval and ongoing oversight.

While greater flexibility can improve customer experience and conversion, it also introduces additional operational complexity, requiring careful management of fraud, regulatory requirements and partner relationships.

You can watch the full panel discussion here.