A new BIS paper argues major crypto exchanges have evolved so far beyond their original function that a new classification is needed.

Crypto exchanges are essentially banks without the rules, according to new research from the Bank for International Settlements’ (BIS) Financial Stability Institute

Published in April, the paper titled ‘Cryptoasset service providers as financial intermediaries: risks and policy approaches’ warns the world’s largest cryptocurrency platforms are operating as de facto banks – borrowing from customers, extending credit and transforming risk – while remaining largely outside the prudential frameworks that govern traditional financial intermediation.

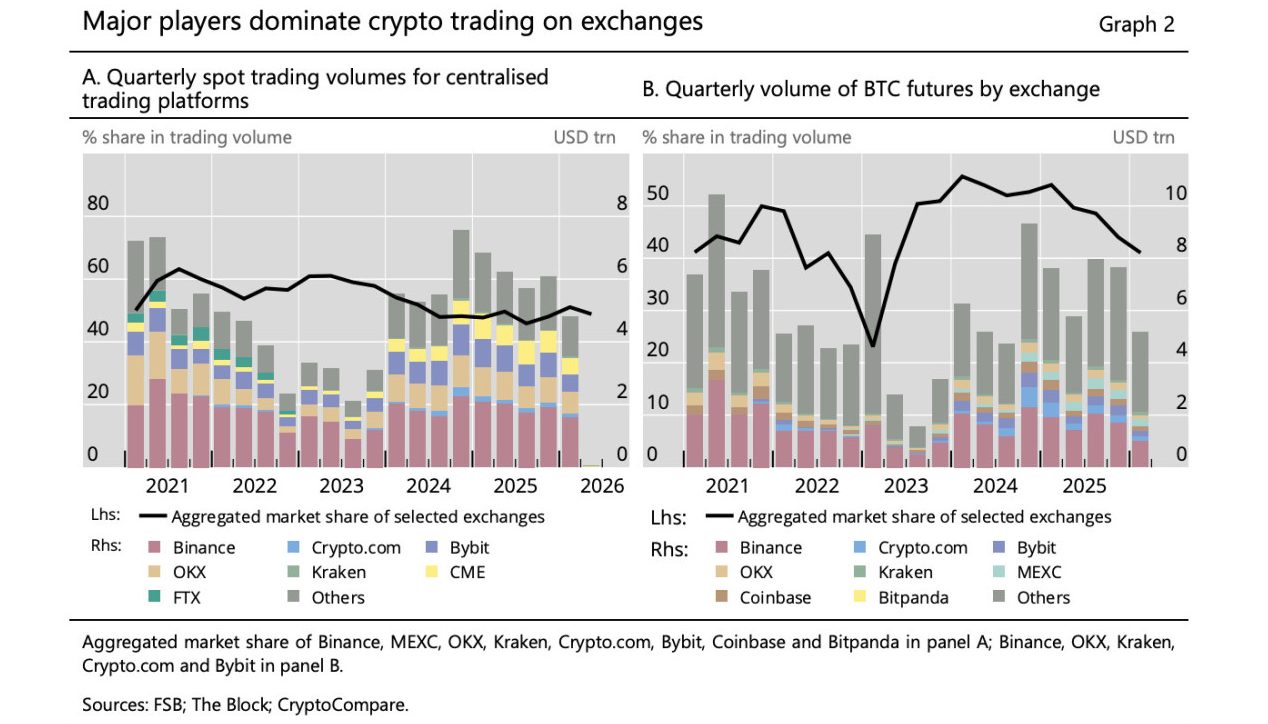

This core finding argues major crypto exchanges have evolved so far beyond their original function that a new classification is needed: multifunction cryptoasset intermediaries, or MCIs. The paper draws on a review of terms and conditions from platforms including Binance, Bybit, Coinbase, Crypto.com, Kraken, MEXC and OKX, conducted between November 2025 and March 2026.

Its conclusion is these platforms’ products, business models, and risk profiles now more closely resemble those of banks or prime brokers than trading platforms or custodians.

Crypto exchanges: earn products are deposits in all but name

The BIS finds so-called “earn” or “yield” programmes, which allow users to deposit cryptoassets in exchange for a return, effectively transferring legal ownership of the deposited assets to the platform.

The paper’s analysis of T&Cs reveals crypto exchanges commingle deposited assets with other customers’ assets, and grant themselves full discretion over how those assets are deployed – whether through lending, market-making or DeFi protocols. The platform then returns an equivalent amount at redemption, along with a yield funded by that deployment.

This structure, the paper argues, creates short-term redeemable liabilities that are economically indistinguishable from bank deposits. The critical difference is that no deposit insurance scheme or central bank liquidity facility stands behind them.

The collapse of Celsius Network in 2022, in which a depositor run on its earn product triggered insolvency after the platform was unable to meet $1.4bn in net withdrawals over six weeks, is cited as a direct precedent for what happens when maturity and liquidity transformation occurs without prudential buffers.

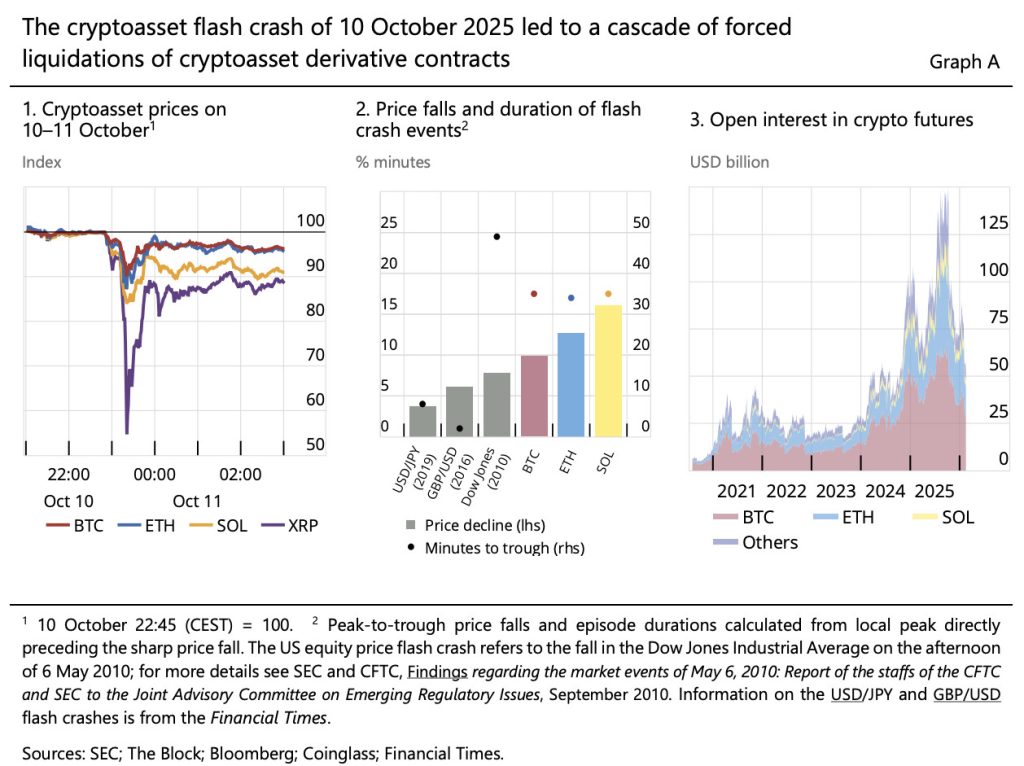

The October 2025 flash crash as a live stress test

The BIS also examines a more recent event: the cryptoasset flash crash of 10 October 2025, in which prices fell sharply within a 30-minute window, triggering a cascade of automated liquidations that BIS estimates caused at least $19bn in direct losses, comparable in scale to the $20bn unwinding of Archegos Capital in 2021.

The event is used to illustrate the amplifying role newly-coined ‘MCIs’ play through their vertical integration of brokerage, pricing, trading, clearing and settlement functions within a single entity.

Binance suffered an operational outage during the flash crash, which restricted investors from closing positions and caused pricing discrepancies that led three margin-eligible tokens – including two wrapped cryptoasset tokens and an algorithmic stablecoin – to briefly lose their pegs on the platform.

Customer losses from those de-peggings alone were reported at $600m, with Binance later announcing $283m in compensation. BIS uses the episode to argue that the combination of high leverage, volatile collateral and vertically integrated intermediation functions makes ‘MCIs’ structurally prone to cascade events under stress.

Regulatory response to ‘MCIs’ has not kept pace

The BIS report finds that the regulatory response has not kept up with the evolution of crypto-trading platforms. Only 11 of the 28 jurisdictions surveyed by the Financial Stability Board (FSB) in 2025 had a finalised framework addressing financial stability risks from crypto platforms.

Of those, only two covered borrowing and lending activities, and only three addressed earn products. Proprietary trading – an activity many ‘MCIs’ are presumed to conduct but rarely disclose – remains the least regulated area of all.

The BIS says a two-pronged approach is needed to close the regulatory gap. Firstly, it says an entity-based regulation is needed to impose capital and liquidity buffers, governance standards and stress testing requirements on ‘MCIs’ as consolidated groups.

Second, it argues for activity-based rules targeting specific high-risk products, including minimum margin requirements for retail borrowers.

The paper also notes several jurisdictions are exploring prohibition of the asset ownership transfers that prop up earn products entirely – preventing deposit-like liabilities from arising without a direct ban on the products themselves.

Payment Expert has reached out to Financial Conduct Authority (FCA) to sound out the UK’s response to these findings.