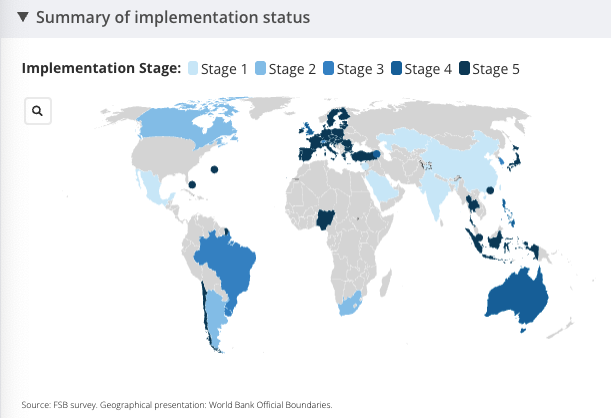

Of jurisdictions reviewed, 11 (39%) have finalised a crypto-asset framework that addresses financial-stability risks; 8 (29%) are consulting or finalising; 3 (11%) are partial; 6 (21%) are still early-stage.

Regulators have spent two years writing rules for crypto and stablecoins. The Financial Stability Board now says the hard part – making them work across borders – has barely begun, leaving gaps big enough for the next crisis to slip through.

The FSB’s thematic peer review, released on October 16, finds countries relying on cooperation pacts that were designed for yesterday’s markets and are still used mainly to license firms or pursue one-off investigations, not to police day-to-day risks that spill across jurisdictions.

The peer review examines how 37 jurisdictions (FSB members plus selected others) have translated last year’s “same activity, same risk, same regulation” blueprint into law. A companion information note with IOSCO maps how 20 markets are applying market-integrity and investor-protection rules to crypto intermediaries.

Together, the reports paint a picture of visible progress, but with uneven depth and little of the real-time, cross-border supervision that crypto actually demands.

The headline risk: cooperation that stops at the border

Most authorities lean on IOSCO’s multilateral memoranda of understanding (MMoU/EMMoU). Those tools were built for securities enforcement and authorisations; the FSB finds they are “mainly used for enforcement” and “do not currently extend to financial stability risks.”

Banking supervisors and stability authorities are often outside these pacts altogether, creating blind spots when a crypto firm spans payments, banking rails and trading venues.

Where bespoke mechanisms do exist, they are young and sporadically used. Some jurisdictions have begun widening MoUs from licensing to enforcement or enabling cross-border on-site inspections, but the review concludes there is still “no evidence” that current arrangements adequately support sharing information relevant to systemic risk. Legal barriers to sharing confidential or personal data compound the problem.

Stablecoins: same promises, different rulebooks

The FSB flags wide divergence in core prudential requirements for stablecoin issuers—capital, liquidity, reserve custody and eligibility, redemption and wind-down planning.

Those differences matter for payments: identical tokens can face contradictory obligations depending on where the issuer is domiciled or where reserves are held, fragmenting liquidity and inviting regulatory arbitrage.

The Board’s remedy is blunt: jurisdictions should close gaps with specific focus on liquidity risk management, capital buffers, stress testing, user redemption, reserve custody and recovery and resolution planning.

What’s been built so far

A growing group of markets now have final frameworks on the books.

The FSB list includes the EU, Hong Kong, Japan, Singapore, Türkiye and others; in total, 11 jurisdictions are in the “finalised” column. Several more, including the UK and Australia, have proposals that are not yet in force. But rules on high-impact activities such as crypto borrowing and lending are far from universal, and the review notes persistent variation in how authorities scope, license and examine multi-function crypto intermediaries.

On supervisory posture, the FSB sees a split: among members with regimes in place, attention is shifting towards recovery and resolution planning for crypto firms and stablecoin arrangements; non-members are still prioritising consumer protection, fraud controls and disclosures as they build capacity.

The divergence reflects different stages of the rulemaking cycle—and adds to inconsistency in the near term.

The IOSCO lens: market integrity still lags

IOSCO’s parallel stock-take focuses on governance, conflicts, custody, retail protections, disclosures and market-abuse controls across 20 jurisdictions.

It underscores that information-sharing should span the entire regulatory lifecycle rather than flare up only when something breaks. That is not how most regimes operate today.

The FSB’s most pointed conclusion is that the world has built national frameworks without the connective tissue to manage cross-border failures or fast-moving spillovers between crypto and traditional finance. That leaves central banks and market regulators trying to monitor systemic linkages with limited data and cooperation tools not designed for stability work.

In the near term, the Board wants jurisdictions to prioritise full implementation of its 2023 framework and to align stablecoin rules, improve supervisory data and extend cooperation beyond licensing and case-by-case enforcement.