The ECB has revealed that eurozone banks may spend €4–5.8bn implementing the digital euro, far less than PwC’s earlier estimates, and with minimal risk.

When Europe launched the single currency a quarter of a century ago, policymakers fretted over the cost of minting, printing and distributing a new form of money.

Economists warned of logistical nightmares, treasury officials argued over budgetary strain, and sceptics predicted chaos at the cash register. The euro, in the end, became one of the continent’s most quietly successful acts of integration — but not without its share of fiscal and political angst.

Now, the debate has returned in digital form.

On October 10, the European Central Bank (ECB) published a pair of technical analyses that cast new light on what it will take to bring the digital euro – the planned central bank digital currency (CBDC) for the eurozone – from concept to reality.

One paper, a detailed assessment of bank investment costs, estimated that euro area institutions would collectively need to spend between €4 billion and €5.8 billion over the four-year implementation phase. The other, a technical annex on financial stability, examined whether the introduction of a digital euro could trigger deposit flight or liquidity stress across the banking system.

Together, the reports paint a picture of cautious feasibility: an ambitious monetary project that, while far from free, appears neither prohibitively expensive nor systemically risky.

A measured price tag

The ECB’s assessment of bank investment costs is clear in its arithmetic. Analysts concluded that banks would likely face annual expenditures of $1.16bn (€1 billion) to €1.44bn between now and full rollout, roughly 0.7% of the sector’s annual net income and 3.4% of significant banks’ yearly IT upgrade budgets.

The total, spread across nearly 2,000 credit institutions with retail payment operations, is “broadly comparable to those incurred under PSD2 and lower than SEPA implementation costs”, the paper notes.

In a letter accompanying the reports to Aurore Lalucq, Chair of the European Parliament’s Committee on Economic and Monetary Affairs (ECON), ECB Executive Board member Piero Cipollone described the findings as evidence that “using the digital euro for daily payments will not harm financial stability.”

He added that the cost estimates “provide a reference point for evidence-driven discussions and a constructive dialogue with the banking industry towards the shared goal of minimising investment efforts.”

The central bank’s economists suggest the burden could shrink further if institutions “leverage synergies in investment costs, for example through central or specialised service providers that can serve multiple banks and reduce redundancies.” In other words, the more the industry collaborates, the cheaper the transition becomes.

This stance effectively rebuts earlier claims from PwC, whose analysis for the European Banking Federation had suggested far higher figures – potentially several times the ECB’s estimate. The ECB’s modelling, developed with consultancy Roland Berger, challenges PwC’s assumptions, arguing that they overstate costs by ignoring existing infrastructure and shared outsourcing models.

The ECB’s own range, it insists, reflects a realistic, mutualised investment environment rather than a fragmented one.

Counting the digital cost

What does €1bn a year really mean in practice?

For a sector whose combined net income nears €200 billion, not much. The paper’s authors liken the scale of spending to other regulatory or technological overhauls. The roll-out of SEPA – which harmonised euro payments across borders – was costlier. Even PSD2, which forced banks to open up customer data to third parties, required similar investment levels.

In context, the digital euro appears financially digestible, though politically more charged.

The ECB’s analysis breaks costs into components familiar to any bank IT executive: interface development, back-office integration, compliance, and testing. The advantage, it argues, lies in shared digital plumbing. If banks adopt common infrastructure or rely on collective providers then overall costs could fall by up to 40%.

Italy’s CBI Globe and Spain’s Redsys are cited as examples where mutualised systems already deliver such savings.

Stability by design

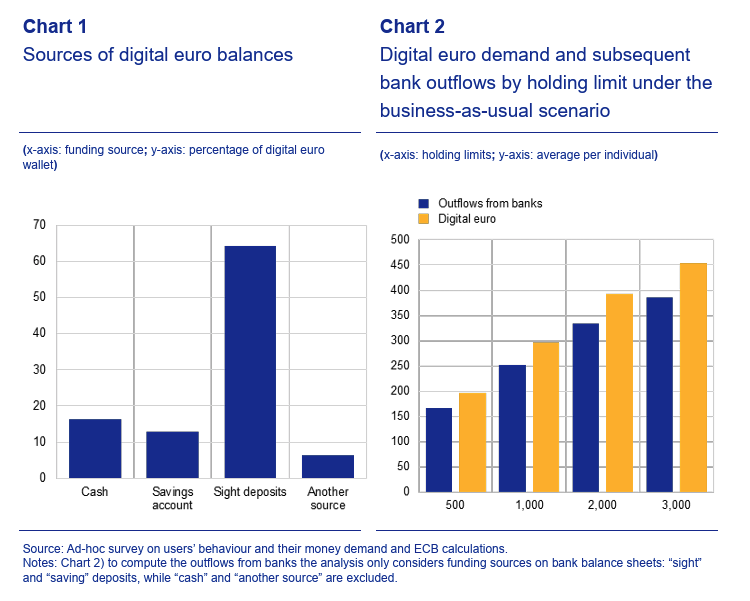

The ECB’s technical annex on financial stability, published alongside the cost study, addresses the deeper fear that a digital euro might suck deposits out of commercial banks, destabilising the financial system. Using newly constructed models and supervisory data from over 2,000 banks, the ECB tested several “holding limit” scenarios – caps on how much digital euro individuals could own, ranging from €500 to €3,000.

Under a business-as-usual scenario, the estimated deposit outflows are modest. Even with a €3,000 limit, total outflows amount to less than 2% of retail sight deposits, well below regulatory liquidity assumptions. Under a hypothetical flight-to-safety scenario (a system-wide crisis in which everyone moves funds into central bank money) deposit outflows could reach €699 billion, or about 2.2% of total banking sector assets.

Yet even then, the ECB finds that banks’ liquidity coverage and funding ratios would remain “well above 100%”, meaning the system could absorb the shock.

The report notes that in aggregate, banks’ liquidity coverage ratio (LCR) would fall only slightly, from 166% to 163%, even in stress conditions. Their net stable funding ratio (NSFR) would dip marginally from 128% to 127%. Profitability impacts are minimal: the ECB estimates that banks’ return on equity (RoE) would decline by 9 to 18 basis points, barely 1% of the historical volatility in the sector’s earnings. And when factoring in ongoing digitalisation trends, some banks could even see a net increase in deposits as cash continues to fade.

The conclusion, in the ECB’s own phrasing, is that “holding limits effectively restrict deposit outflows from the banking sector to levels that safeguard the stability of the financial system.”

Politics, perception, and the single currency’s next act

The latest documents from Europe’s central bank form part if it’s strategy to reassure legislators as negotiations intensify over the Single Currency Package, the legislative framework underpinning the digital euro.

In recent months, members of the European Parliament – including rapporteur Stéphanie Yon-Courtin and Lalucq – have pressed the ECB for clearer evidence on how a digital euro would affect banks and consumers. The analyses released last week are a direct response to those requests.

Cipollone’s covering letter explicitly invites MEPs to share the findings “with members of the Parliament’s negotiating team… to facilitate swift progress.”

For the ECB, their research says the digital euro can coexist with commercial banks rather than replace them; that it can modernise payments without draining deposits; and that, despite the inevitable start-up bill, it is a manageable investment in Europe’s monetary sovereignty.

A familiar cycle of scepticism

If the conversation sounds familiar, it’s because Europe has been here before. The euro’s paper-and-metal debut in 2002 was preceded by years of budgetary haggling and doomsday projections. Then, as now, the sums seemed eye-watering, until history redefined them as the cost of progress.

The digital euro may prove a smaller, subtler revolution, but the principle is similar; building public money for a new era of payments. Whether banks see the €4–6 billion investment as a burden or an opportunity may depend less on spreadsheets than on imagination. As the ECB’s analysts dryly note, these figures exclude the potential “revenue opportunities and business model benefits” that could emerge once the system is live.

In other words: what begins as an expense line may end up as infrastructure.