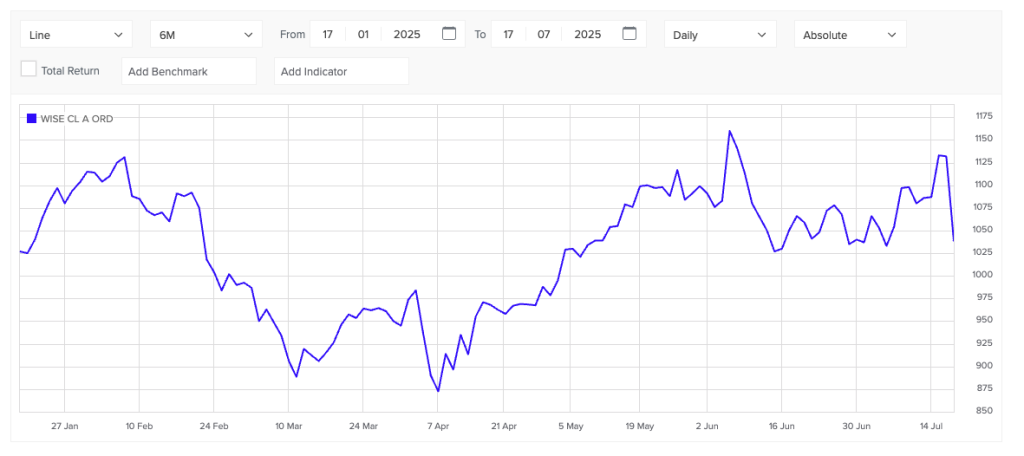

Shares in cross-border payments fintech Wise plunged more than 10% today (July 17) after the company reported weaker-than-expected income and a continued decline in the fees it collects from international transactions.

The London-listed group, which facilitates low-cost money transfers across borders, reported underlying income of £362 million for the three months to June 30, missing analyst expectations compiled by Bloomberg by around £10 million.

Despite growing its customer base to 9.8 million users, a 17% year-on-year increase, and processing £42.1 billion in cross-border volume during the quarter (up 24%), the group’s share price fell to £10.17; its steepest drop this year, erasing previous gains made in 2025.

According to the London Stock Exchange, at the time of reporting, the total volume traded off-book reached nearly 486,000 shares.

Perhaps more notable than the headline miss was Wise’s continued erosion in take rate – the percentage of transaction value the company retains as revenue.

In its Q1 FY26 trading update, the company disclosed that its cross-border take rate had fallen 12 basis points year-on-year, settling at just 0.52%.

That trend reflects Wise’s strategy of cutting prices to attract higher-volume users and grow its market share. While effective in scaling customer numbers and total volume, the approach has created mounting tension with the group’s financial performance, particularly when paired with unfavourable currency movements.

Kristo Käärmann, Wise’s co-founder and CEO, acknowledged the challenges while striking an upbeat tone:

“We have had a strong start to our financial year, progressing on our journey to moving trillions with more people and businesses around the world using Wise,” he said.

Wise reiterated its full-year guidance, projecting underlying income growth of 20 per cent for FY26, which aligns with its medium-term target of 15–20 per cent growth on a constant currency basis.

Listing ambitions meet market realism

The timing of today’s sell-off was particularly stark given Wise’s recent momentum in capital markets.

Just last month, the company confirmed plans to shift its primary listing from London to the US, a move it hopes will deepen investor access and accelerate its ambition to become “the” global infrastructure for money movement.

It also secured a notable win in Europe through its partnership with UniCredit, which will use Wise’s infrastructure to power cross-border payments for personal and business customers, following an earlier tie-up with Raiffeisen Bank.

But the combination of currency volatility and falling margins has highlighted the risks involved in Wise’s global expansion. For all its growth, the company is making less per transaction, and markets are clearly weighing whether that trade-off is sustainable.

Can volume outrun valuation pressure?

With customer holdings up 31% year-on-year to £22.9 billion, and platform partnerships continuing to expand, Wise appears intent on building a global payments network that operates at massive scale.

But it now has to find a way to maintain its low-cost proposition for users, while restoring confidence among investors rattled by shrinking unit economics.