Monzo has reported its third consecutive year of profitability, driven by record customer growth, expanding deposit balances and four revenue streams each generating more than £300m

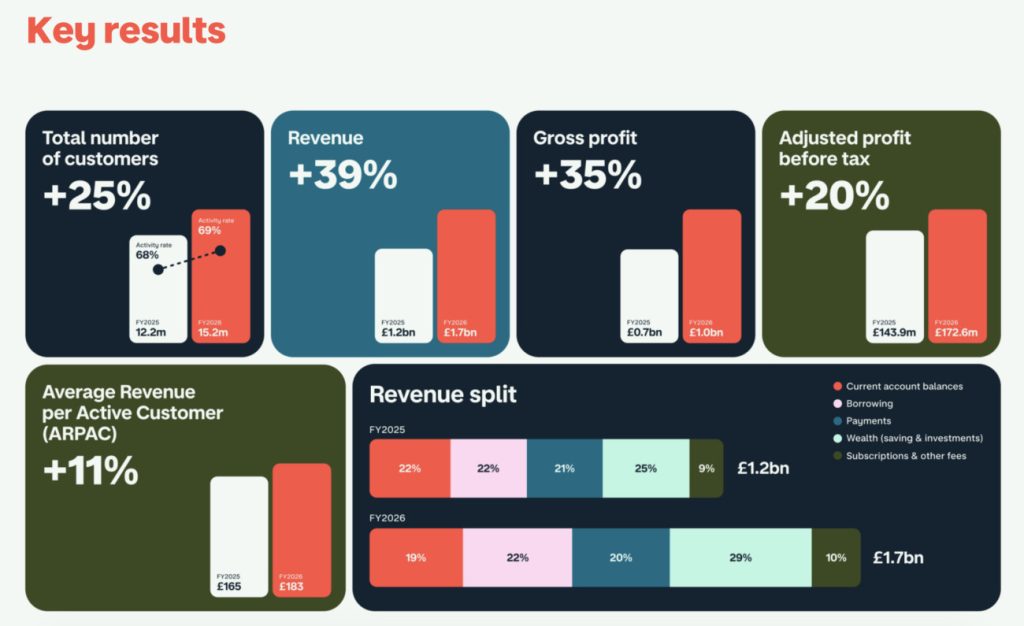

Monzo has delivered its strongest financial performance to date, with revenue climbing 39% year-on-year to £1.7bn ($2.28bn) for the year ended 31 March 2026, as the challenger bank continued to deepen its grip on the UK retail banking market while laying the groundwork for European expansion.

Adjusted profit before tax rose 20% to £172.6m, up from £143.9m in the prior year, with gross profit reaching £1.0bn – a 35% increase.

The results marks the digital bank’s third straight year in the black, which Chair Gary Hoffman described as “pivotal”, adding that the bank’s “diversified business model delivered a strong financial performance” – a characterisation the numbers broadly support.

Monzo: Record customer additions fuel deposit surge

The bank added more than three million customers during the year – its highest annual intake to date – bringing its total base to 15.2 million across personal and business accounts.

Around one in five UK adults now bank with Monzo, with roughly half of its monthly active users, which reached 10.4 million, treating it as their primary bank.

Business banking was a particular bright spot, with customer numbers jumping 45% to 905,000. Average revenue per active customer rose to £167 in personal banking and £484 in business banking, up 9% and 12% respectively.

Customer deposits surged 55% to £25.7bn, buoyed by a 75% increase in savings deposits to £15.5bn. More than 3.5 million customers now hold savings with Monzo, while the lending book grew 42% to £2.6bn. Crucially, credit loss expenses grew at a slower rate than balances, with the loan loss rate improving from 9.4% to 9.0%.

The increasingly diversified revenue base was a notable feature of the results. Four distinct income streams – current account balances, borrowing, payments and wealth – each surpassed £300m for the first time, compared to just one the prior year.

European expansion and first acquisition a sign of strategic shift?

Beyond the headline numbers, FY2026 marked a series of structural milestones. In December 2025, Monzo became the first digital bank to receive a European banking licence via the Central Bank of Ireland, enabling it to begin serving personal and business customers in Ireland. A waitlist of 100,000 preceded the official April launch, with Spain announced as the next target market.

The bank also agreed to acquire digital mortgage broker Hey Habito, completing the transaction on 1 April 2026. With more than 550,000 customers already tracking their mortgage through Monzo’s homeownership feature, the deal provides a capital-efficient route into the broker-led mortgage market.

Monzo also closed its US operations during the year, concentrating investment on the UK and Europe where it believes it can build deeper customer relationships.

CEO Diana Layfield, who took the role from TS Anil in February 2026, said: “Building a business that can innovate at pace and invest for the future while delivering sustainable growth and profitability requires deliberate choices and discipline.”

Investment phase weighs on cost ratios

Not all metrics moved in the right direction. The cost-to-income ratio edged up to 74% from 70% as the bank accelerated hiring across product, technology and financial crime functions, and increased its marketing spend by 46% to £143.1m.

Personnel costs rose 19% to £421.6m, with average headcount growing to 4,674.

Fraud-related costs also increased materially. Monzo reimbursed £59.6m to fraud victims during the year – an 85% increase – reflecting the full-year impact of the Payment Systems Regulator‘s (PSR) mandatory reimbursement regime for authorised push payment scams, introduced in October 2024.

The Financial Conduct Authority‘s (FCA) investigation into historical financial crime controls concluded in July 2025 with a £21.1m fine. Monzo leadership characterised the resolution as drawing a line under issues firmly in the past.