Nearly half of merchants say legitimate customers are now more likely to commit fraud. What does this mean for payments teams?

Fraud in payments has traditionally been seen as a technical problem—something to be tackled with stronger authentication, better risk models and real-time transaction monitoring.

But new data from Ravelin’s Global Fraud Trends 2025 report suggests a different story: the most disruptive form of fraud may now be coming from legitimate users.

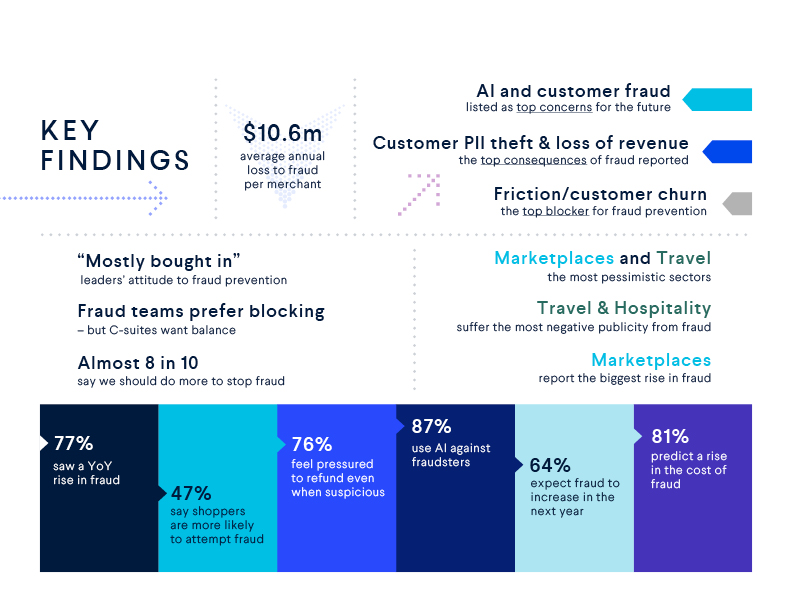

According to the survey of more than 1,400 fraud and payments professionals, 47% of merchants believe that customers are more likely to attempt fraud than in previous years. In parallel, 76% of respondents say they feel pressured to refund customers even when there are signs of abuse.

This shift in behaviour—commonly labelled as first-party fraud—includes false claims for refunds or chargebacks, misuse of return policies, and account takeovers where the fraudster has legitimate credentials.

It’s harder to detect, more complex to resolve, and poses reputational risks if handled poorly.

“Too many retailers are happy to dismiss fraud as a cost of doing business,” said Ravelin CEO Martin Sweeney in the report.

“Downplaying fraud to protect the customer experience is a false dichotomy. Armed with the right tools and intelligence, retailers can build context about every single customer, easily telling fraudsters from legitimate shoppers.”

A cultural shift, not just a technical one

While traditional card-not-present (CNP) fraud remains the most costly (reported by 61% of merchants), refund abuse and friendly fraud are rising rapidly. The report found that 55% of respondents expect refund abuse to increase further in the next 12 months, a concern that now ranks above even account takeover attempts for many sectors.

Part of the challenge lies in how payments and fraud teams are structured. Fraud professionals often favour stronger controls, but the C-suite tends to prefer frictionless checkout experiences.

The number one blocker to improving fraud prevention today, according to the survey, is not budget—it’s concerns about customer friction and churn.

This creates internal tension. Merchants want to preserve the customer journey, but in doing so, may inadvertently create opportunities for abuse.

Missed opportunities in dispute handling

The report also shows that the industry is struggling to push back on first-party fraud through the chargeback system. In 2025, the average success rate for disputed chargebacks fell to 43%, down from 49% the previous year. Marketplaces performed the worst, both in terms of challenge rates and success.

This declining success suggests that many merchants lack the evidence or process infrastructure to effectively counter friendly fraud. Without improvement, it’s a risk area that will continue to drain revenue and increase operational cost.

A path forward: balance, not trade-off

Despite the challenges, there is progress. 87% of merchants now use AI to fight fraud, and many are investing in tools that allow for more nuanced risk scoring—especially around return and refund requests. More merchants are also beginning to treat fraud as a cross-functional issue, with marketing, customer experience, and operations teams all recognising its impact.

“With the financial and reputational stakes rising, the message is clear: fraud is no longer a side issue—it’s a core business risk,” said Sweeney.

“Now, merchants can have robust fraud controls that protect themselves and their honest customers. They can deliver great customer experiences, all while clawing back lost revenues.”