New data from the UK’s Payment Systems Regulator reveals wide disparities in how banks handled APP fraud claims before October 2024, with outcomes heavily dependent on where customers held their accounts.

The UK’s Payment Systems Regulator has published its final dataset on authorised push payment (APP) scam performance before the introduction of mandatory reimbursement rules, revealing a fragmented system in which customer outcomes varied significantly between banks.

The report, covering January to 7 October 2024, shows that while a majority of victims did receive some form of reimbursement, protection levels differed sharply across the market. According to the regulator, 60% of APP scam losses were reimbursed by value and 73% by volume during the period.

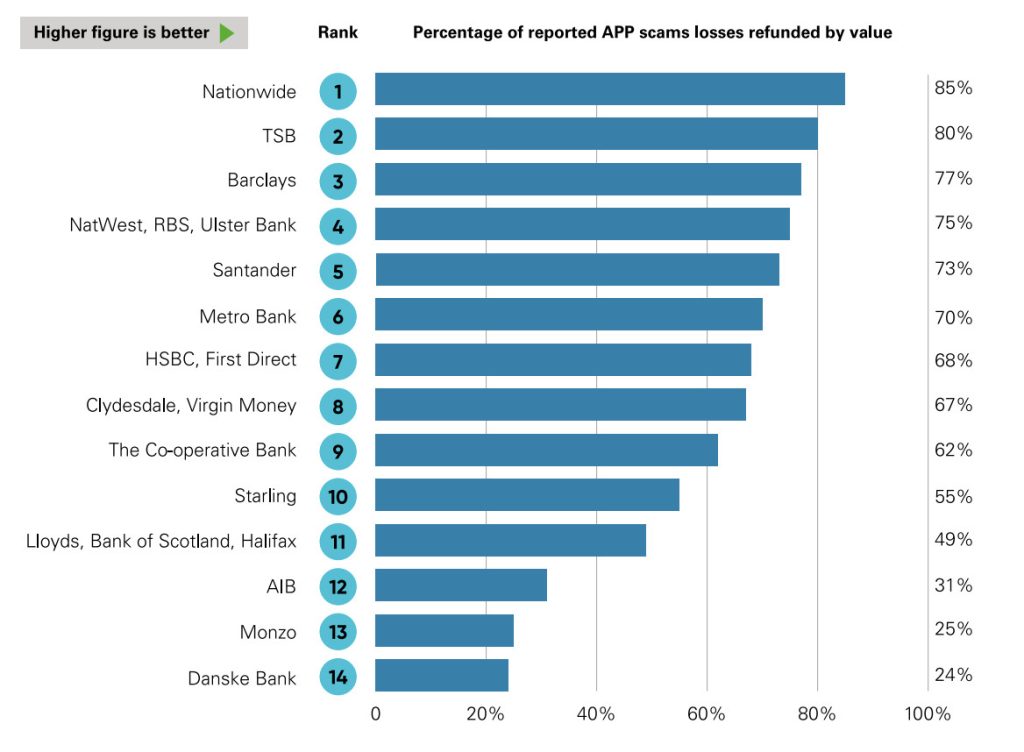

However, this aggregate figure masks a wide divergence in firm-level performance. The PSR identified a gap of 61 percentage points between the highest and lowest reimbursement rates among the UK’s 14 largest banking groups, highlighting what it described as inconsistent outcomes for consumers prior to regulatory intervention.

“Consumer outcomes used to depend on who they bank with,” the regulator stated, underlining the central rationale for its decision to introduce a mandatory reimbursement requirement in October 2024.

Bank-level disparities come into focus

Firm-level data published alongside the report shows clear differences in how banks approached reimbursement. Leading firms (Nationwide and TSB) reimbursed more than 80% of APP scam losses by value.

At the other end of the spectrum, firms including Allied Irish Bank (UK), Danske Bank and Monzo ranked among the lowest for reimbursement rates, with significantly smaller proportions of losses returned to customers. This disparity extended to the number of cases reimbursed, with some banks fully or partially refunding nearly all claims, while others rejected a far greater share.

The findings reinforce longstanding concerns among policymakers that voluntary reimbursement frameworks failed to deliver consistent consumer outcomes, particularly as APP fraud became one of the UK’s most prevalent financial crimes.

APP scams accounted for just over 38% of all fraud losses in 2024, according to the PSR, underlining the scale of the issue prior to regulatory reform.

Fraud risk concentrated in smaller PSPs

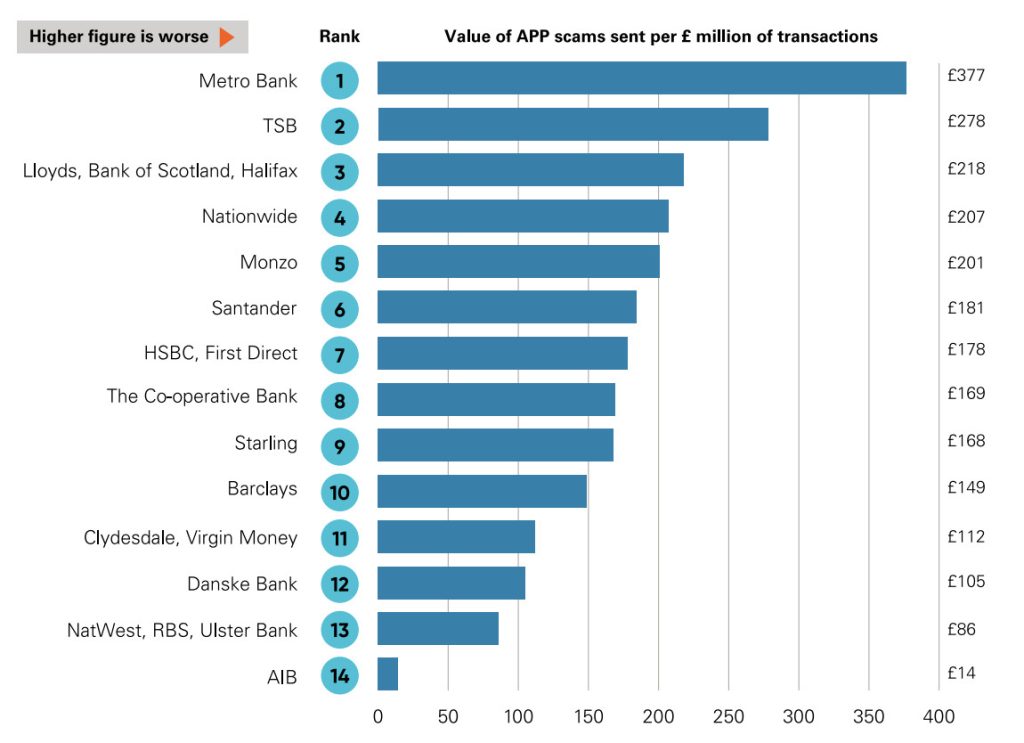

Beyond reimbursement outcomes, the report highlights structural imbalances in where fraud occurs within the payments ecosystem.

Data on receiving firms shows that smaller, non-directed payment service providers (PSPs) account for a disproportionately large share of APP fraud. These firms were responsible for 34% of total fraud value despite handling only 19% of Faster Payments transactions by value.

By transaction volume, the disparity is even more pronounced. Non-directed PSPs accounted for 48% of fraudulent transactions while processing just 10% of payments, pointing to a concentration of risk in a relatively small segment of the market.

The PSR also noted that fraud rates among these firms were significantly higher than those observed at the largest banking groups, with non-directed PSPs recording rates dozens of times greater in some cases.

This imbalance has become a focal point in the regulator’s broader approach, particularly as liability for APP fraud is now shared between sending and receiving institutions under the new rules.

Fraud levels decline but remain significant

The report indicates that overall APP fraud losses showed signs of decline in early 2024, with £145m lost in the first half of the year, representing an 18% decrease compared to the same period in 2023.

The number of cases also fell by 13% year-on-year, suggesting that prevention efforts may have begun to take effect even before the reimbursement requirement came into force.

However, the PSR emphasised that APP fraud remains a major issue for the payments sector, both in terms of financial losses and its impact on consumer trust.

A breakdown of scam types shows a divergence between high-frequency and high-value fraud. Purchase scams accounted for 73% of cases but only 27% of total losses, while investment scams made up just 4% of cases but represented 25% of the total value.

Regulatory shift reshapes outcomes

The dataset marks the end of the pre-reimbursement regime, providing a baseline against which the impact of the PSR’s policy can be measured.

Since the introduction of mandatory reimbursement in October 2024, the regulator reports that 88% of APP scam losses within scope have been returned to victims, equating to £173m.

Under the new framework, reimbursement costs are split equally between sending and receiving PSPs, with the aim of incentivising stronger fraud prevention across the payments chain.

The PSR described the policy as a “global-first approach” designed to improve consumer protection while encouraging greater collaboration between firms.

While firm-level performance data for the post-implementation period has yet to be published, the regulator indicated that outcomes have already shifted significantly, with faster claim resolution times and higher reimbursement rates reported in the first year of the regime.