Santander’s latest research shows that UK consumers are satisfied with how they pay today but want fraud prevention and protection placed at the heart of future innovation.

UK consumers want fraud-first payments innovation, not new ways to pay, a new report from Santander has revealed.

The bank’s Transacting Tomorrow: The role of retail payments in powering UK growth report, published on December 2, finds that most consumers believe the UK’s existing payments landscape “serves consumers well”, with 70% saying current options meet their needs. Only one in five respondents believe brand-new payment methods are required.

Instead, the report highlights the scale of concern around fraud and consumer protection. More than half of consumers polled (52%) said fraud or loss of funds was their biggest worry when making payments, signalling a clear demand for safety-led improvements rather than novelty.

“As our data shows, banks remain the most trusted advocates in driving change and shaping consumer behaviour. We must take these responsibilities seriously” said Santander UK Chief Payments Officer Paul Horlock. “The whole ecosystem from government, regulators, banks and fintechs must build a model that meets consumer demand and protects users, while also ensuring the commercial viability of future ways to pay.”

He added: “At the same time, a more pro-innovation stance from regulators is essential and public political backing for that stance is vital if the UK is to stay ahead globally.”

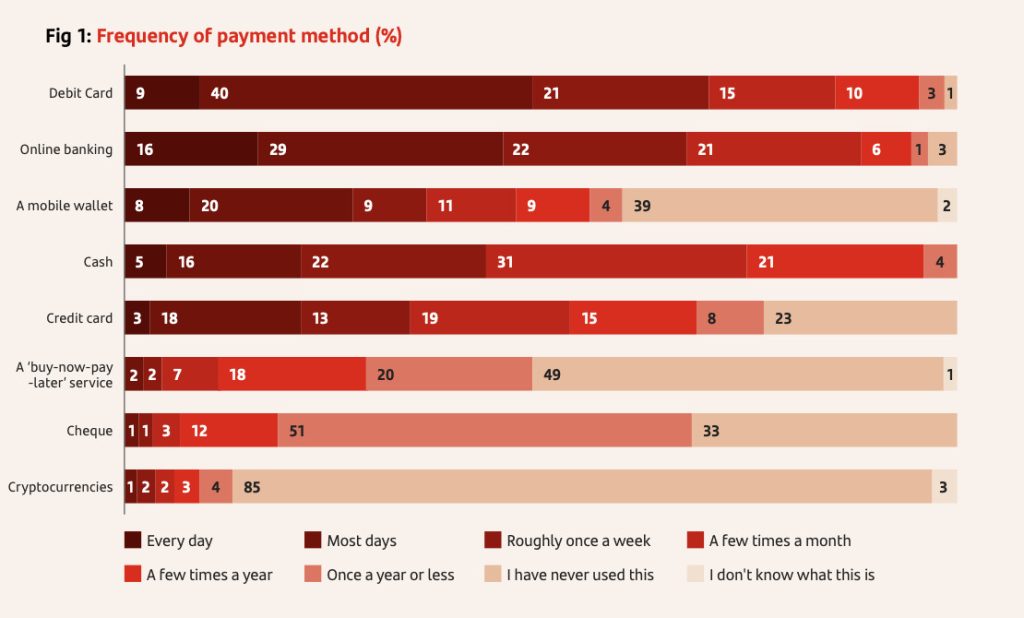

How Britain pays today

The report shows a payments landscape defined by familiarity and practicality. Debit cards continue to dominate everyday spending, while credit cards remain preferred for high-value purchases, particularly because of statutory protections such as Section 75 and chargeback.

Mobile wallets have grown significantly, with around a quarter of consumers now using them most frequently, led by younger demographics. Yet crypto remains marginal: only a small minority use it regularly for payments and 63% of adults say they are “very unlikely” to use cryptocurrencies in future.

Fraud and protection trump speed and novelty

Consumers are clear on where they want innovation: closing the “real gaps” around fraud and loss of funds. Santander argues that future infrastructure should embed prevention measures by design, including the ability to slow suspicious transactions and richer data-sharing across the ecosystem.

For Jonathan Frost, Director of Global Advisory for EMEA at BioCatch, the findings reflect long-standing structural issues: “Payment fraud tops consumer concerns because the UK’s fraud controls remain reactive rather than preventative.

“While the PSR’s mandatory reimbursement requirements have successfully returned millions to victims, they haven’t stemmed the underlying crime. The emotional damage to fraud victims happens long before compensation enters the picture, and lasts long after. If consumers feel exposed using the payments they already rely on, it’s no surprise they’re hesitant to adopt new payment methods.”

He adds that “only one in five believe new payment methods are needed, which is notable given how many also want gaps in fraud prevention and consumer protection closed.”

Low appetite for crypto and the digital pound

The report also reveals low levels of enthusiasm for emerging alternatives. Nearly two thirds of consumers say they are “very unlikely” to use crypto for payments in the future, citing volatility, privacy risks and lack of protection.

Awareness of the Bank of England’s digital pound project remains limited. More than half of respondents (55%) say they have not heard “anything” about it, while many of those who have describe it as unnecessary or confusing.

The public also express concerns about the potential cost to taxpayers and disruption to traditional banking.

Santander’s ten priorities for UK payments

The report sets out ten recommendations for policymakers, regulators and industry. Among the most prominent are:

- Putting consumers first: prioritising fraud prevention and protection ahead of launching new payment methods without clear demand.

- Renewing UK payments infrastructure: replacing Faster Payments and Bacs with modern systems that retain familiar user experiences.

- Designing out fraud: embedding prevention mechanisms and clear liability frameworks into future rails.

- Backing tokenisation over a retail CBDC: prioritising tokenised commercial bank deposits and regulated stablecoins rather than a consumer-facing digital pound.

- Clarifying regulatory roles: using the abolition of the PSR to simplify oversight and enable a more pro-innovation stance.

Banks remain the most trusted players in UK payments, a finding Santander uses to argue that consumer confidence must anchor any future reforms. With instant payments now ubiquitous, the focus is shifting towards the protections and intelligence built around them.

“Now that instant payments have become the norm, the real differentiator is what is built on top,” says Mark Fieldhouse, Chief Revenue Officer at Form3.

“As fraud continues to grow in scale and sophistication, legacy controls will no longer cut it. Banks must prioritise their end customers, which means finding a payments partner that goes beyond meeting basic regulatory requirements, but is investing in automated fraud detection, smarter risk analytics, and seamless Verification of Payee experiences.”

A pivotal moment for UK payments policy

As the UK Treasury coordinates the National Payments Vision and prepares a long-term infrastructure strategy, Santander’s findings feed directly into one of the sector’s most contested questions: how to deliver innovation at pace while strengthening consumer protection.

With public political support for reform still uncertain, Santander warns that the UK risks falling behind global peers unless fraud prevention, tokenisation and pro-innovation regulatory culture advance together.

Horlock said the priorities laid out in the report should “create a payments ecosystem that drives UK growth, protects consumers, and keeps the country at the forefront of global financial innovation”.