Cross-border spend and a faster-growing services arm lifted Mastercard’s third-quarter results, while management held full-year guidance at the high end of mid-teens despite a currency drag.

Mastercard reported a robust third quarter as travel and e-commerce continued to fuel spending and the company’s value-added services grew faster than its core network fees.

Published on October 30, Mastercard’s financial statements showed net revenue rose 17% to $8.6 billion, or 15% on a currency-neutral basis. Adjusted earnings per share increased 13% to $4.38, with GAAP EPS at $4.34. The adjusted operating margin edged up to 59.8%.

CEO Michael Miebach said the quarter was driven by “healthy consumer and business spending” and “continued robust performance” in services such as cyber, authentication and its new commerce media offering, where revenue rose 25% year on year, or 22% currency-neutral.

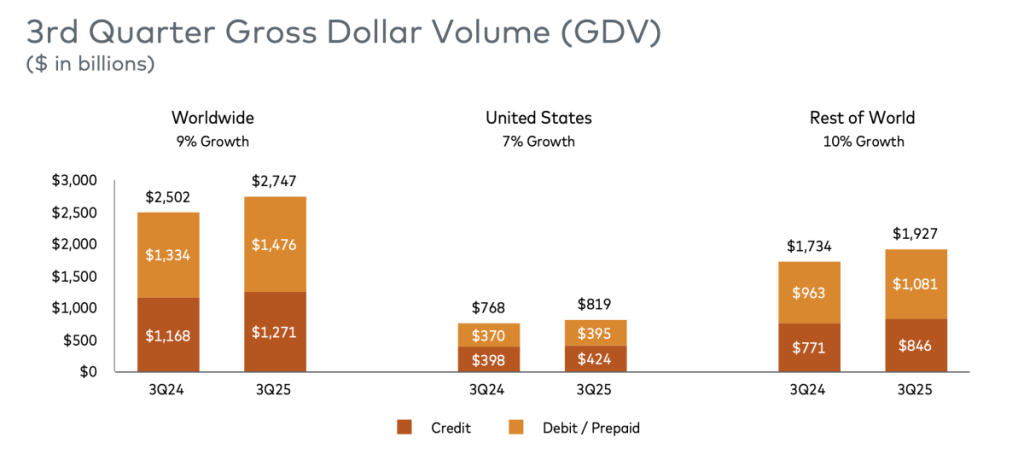

On a local-currency basis, gross dollar volume increased 9%, purchase volume 10% and cross-border volume 15%, while switched transactions rose 10%. Contactless penetration reached 77% of in-person switched purchase transactions and Mastercard and Maestro cards in market stood at about 3.6 billion.

Payment network revenue benefited from the underlying volume growth, but Mastercard again leaned on services wrapped around the transaction, from fraud defence and digital identity to marketing analytics. This helped absorb higher deal costs, with payment network rebates and incentives rising alongside renewals, and adjusted operating expenses up 15% including a four-point contribution from acquisitions.

Company expectations

For full-year 2025, Mastercard still expects non-GAAP net revenue growth at the high end of mid-teens and non-GAAP operating expenses at the high end of mid-teens, with a 1 to 2 percent currency headwind to revenue. For the fourth quarter, management guided to high-teens non-GAAP revenue and opex growth, with foreign exchange a roughly 4 to 4.5 percent drag on revenue.

Capital returns continued to prop up per-share earnings. Buybacks contributed around ten cents to EPS. The company repurchased $3.3 billion of stock in the quarter and a further $1.2 billion through 27 October, while paying $687 million in dividends.

One wrinkle was tax. The adjusted effective rate rose to about 21% in the quarter, reflecting the impact of Pillar 2 rules and geographic mix, which limited the pass-through from operating income to EPS.

Europe leads on volume

Europe was Mastercard’s standout region again in Q3, with purchase volume up to $806bn (from $690bn in Q3’24) and purchase transactions reaching 21.1bn year to date, underscoring continued carded spend resilience across the bloc and UK.

APMEA, however, arguably remained a structural growth engine. Purchase volume rose to $484bn (from $447bn), while GDV climbed to $632bn and purchase transactions to 12.9bn. The region’s mix still skews debit-heavy, which is consistent with faster growth on the debit/prepaid side globally.

Latin America extended steady double-digit momentum, with purchase volume at $169bn (from $145bn) and purchase transactions at 7.4bn, reflecting deeper acceptance and wallet penetration rather than a single-country spike.

In the US, growth was solid but slower. US purchase volume increased to $2.06tn YTD (+7.2%), while purchase transactions reached 11.6bn in Q3, up from 10.9bn a year earlier.