Despite the European Union introducing the world’s first crypto regulatory framework, it is the UK that is ahead of its European counterparts.

Ninety-five percent of UK adults are aware of cryptocurrencies and digital assets, placing the UK ahead of Germany, France, and the Netherlands in crypto awareness, according to new research from Ipsos and Deloitte.

The findings, drawn from a survey of 5,000 adults across Europe, were unpacked during a June 11 breakfast session hosted by BCB Group, featuring insights from Adan and CryptoUK.

The UK’s awareness rate outpaces Germany, France, and the Netherlands, which all came in at 92%, underscoring Britain’s leading position in the region’s evolving digital asset landscape.

Awareness of crypto in the UK has surged in the past several years as a digital alternative to physical cash and as an investment instrument, particularly Bitcoin.

Of those surveyed who have acquired at least one crypto asset, the UK leads in adoption with 23%, ahead of the Netherlands (22%), Belgium (22%), Italy (20%), Germany (17%), and France (14%).

Cryptocurrencies came to the fore with the launch of Bitcoin back in 2008; the instrument was originally designed as a peer-to-peer payment system but is generally viewed as an investment vehicle. Among those who hold or plan to acquire crypto assets, 50% said they see them as a way to generate strong short-term gains or as long-term investment opportunities.

The appeal of using crypto for payments is dwindling. Among current holders, the number intending to use crypto as a form for global transactions has fallen from 14% in 2024, to under 10% this year.

Similarly, the share of users motivated by privacy concerns – using crypto to protect personal data – has also declined. However, there was an increase in those turning to using crypto to protect users from rising inflation rates across Europe.

MiCA’s in, but countries undeserving?

One of the more eye-catching findings from the report was UK customers dissatisfaction with its government for crypto support being lower than many European countries. This is likely due to the current regulatory environment being more crowded in Europe than in the UK.

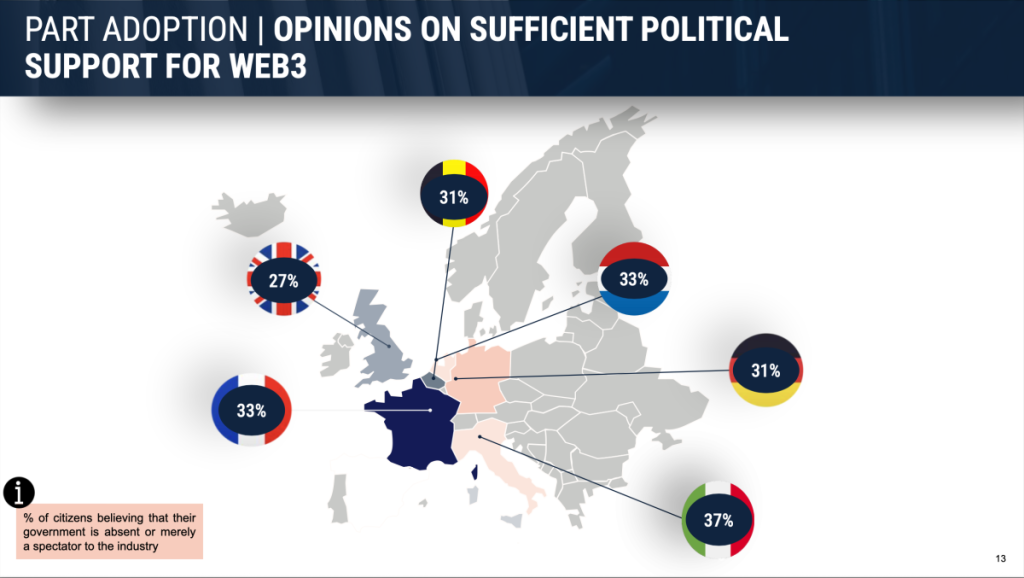

Nearly 30% of UK respondents believe the government is absent or merely a spectator to the industry, whereas Italy (37%), France (33%), the Netherlands (33%), Germany (31%) and Belgium (31%) respondents are more dissatisfied with their respective governments.

Nearly 30% of UK respondents believe the government is absent or merely a spectator to the industry, whereas Italy (37%), France (33%), the Netherlands (33%), Germany (31%) and Belgium (31%) respondents are more dissatisfied with their respective governments. In the EU, the Markets in Crypto Assets (MiCA) legislation governs how members state on how they should approach crypto regulation. But this is bolstered further by independent state level legislation.

Italy, for example, has its own laws when it pertains to payments, not recognising crypto as legal tender and placing a 26% tax rate for crypto transactions that exceed €2,000.

The Banco d’Italia is also working alongside the European Central Bank to help develop the digital euro, a central bank digital currency (CBDC), often viewed as an alternative to the more user-friendly private cryptocurrencies.

Meanwhile in France, crypto rules strongly centre around the need for digital asset service providers to obtain licences to operate, as well as tight AML and CFT regulations around transaction monitoring.

Jérôme Priget, Managing Director of BCB Group, told those in attendance at the breakfast session that the “evolving regulatory” clarity in the EU and UK will play a “crucial role in building consumer and business confidence”.

He also said there should be a “collective responsibility of both the industry and policymakers to enhance understanding across all markets, ensuring Europe remains competitive on the global stage”.