Cybersecurity is evolving in front of our eyes. Whether that be the role of artificial intelligence (AI) having both an instrumental and detrimental effect, or the innovations occurring in blockchain, security has never been more secure, yet so vulnerable.

These parallels are apparent within the blockchain space. Whilst the emerging technology is already laying the foundations for a new breed of security and data management, it is still in its infancy and needs to be refined more.

Speaking on the matter at the London Blockchain Conference, Robert Huber, Tech Lead at blockchain-based Software-as-a-Service platform Veridat, revealed some of the use cases the company has been providing to its partners to realise the benefits of blockchain as a security measure.

Blockchain for Security

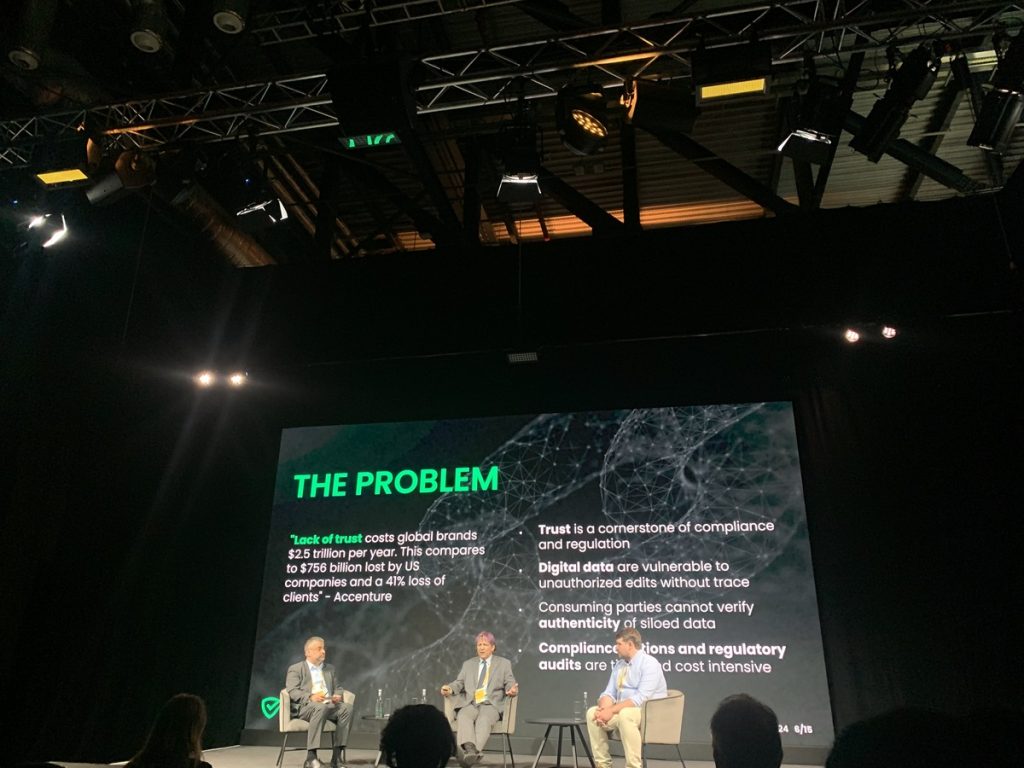

Huber revealed that Veridat has worked with an array of companies from many different industries. The blockchain compliance firm has provided services in the food and drug sector, sectors with significant personal and private data.

These industries, two of the largest in the world, hold a substantial amount of personal data that if breached or stolen could cause a myriad of problems for the companies within them..

But companies have been hesitant to trust blockchain as a means of providing security, and understandably so.

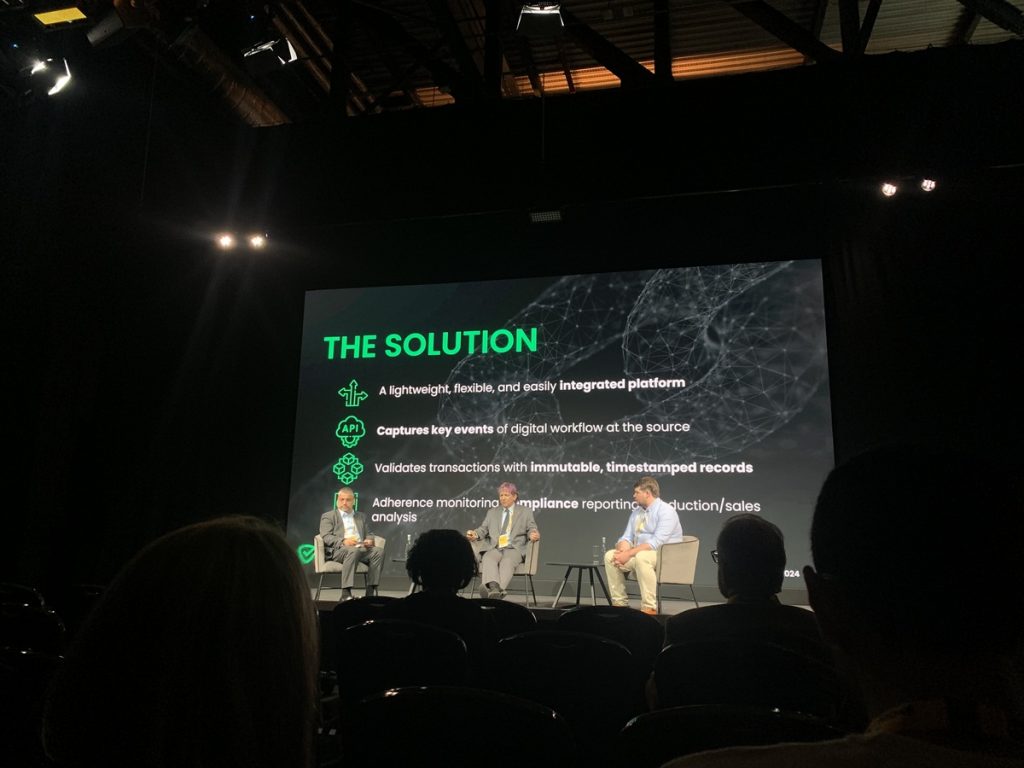

The technology is still in its infancy and has similar issues pertaining to its own security. However, Huber outlined that a lightweight, flexible and easily integrated solution will alleviate those fears.

He explained further: “We help companies by giving them truth systems that back up all the different GXPs of clinical practice, good manufacturing and good laboratory practices.

“We want to put a layer of truth over the data that are being submitted into the Food & Drug Administration (FDA). Our partner White Crow Health Technologies is a company that is absolutely supremely able to acquire data from automated diagnostic machines, without human interference.

“That is really critical because we can catch that before the person touches it and record key events early on in the process, providing a clear data point that everything else can be referenced against.”

And it’s not just companies beginning to open their arms to the idea of blockchain-based compliance solutions. Regulators are increasingly viewing Web3 as a key component through partnership with third-party firms innovating within the space.

Blockchain is also becoming an increasingly vital tool for companies to remain compliant friendly, which Huber notes is also saving entities money too.

“There are a couple of different angles we are really excited about, like the value of blockchain-based technologies to assist us in our compliance solutions we can offer to partners to help them get out of trouble,” said Huber.

“Certainly, a lot of these regulatory frameworks are not cheap to comply with, but what I think has been very clear, non-compliance is a lot more expensive than complying.

“We are a one-stop-shop to help clients to stay compliant, stay within regulations and put data systems in place to allow them to be fully compliant.”

Security for Blockchain

Despite blockchain already playing a heightened role in security measures and data management, does the technology itself need to be secure before it can be properly utilised?

This was a sentiment Joseph Kearney, Research Associate at the University of Kent, believes should be at the forefront of blockchain stakeholders’ minds, and especially before the industry is able to stamp out a looming threat.

He shared: “In terms of blockchain for security vs. security for blockchain, I believe you can’t have security without a secure blockchain. I truly believe over the next decade that quantum computers will present a severe threat to every single blockchain we currently use.

“Essentially, our digital signatures and how we prove who we are, who we say we are on the blockchain, are critically vulnerable to quantum attacks.”

A quantum cybersecurity attack is used to infiltrate existing cryptography on various blockchain networks. These attacks could break the encryption schemes and decrypt data to the will of the attacker, breaching sensitive and valuable information.

Kearney has been studying quantum attacks on blockchain cryptography extensively and revealed that it may take a lot longer than expected before these types of attacks will be completely stomped out.

He said: “A paper I wrote a few years ago proves that proof-of-work is highly vulnerable. We predicted in the paper that by 2042 there could be a single quantum aggressor that could actually perform over a 51% attack on the Bitcoin network, which in theory, should be the most secure because of the high hash rate.

“This integral problem I believe blockchain can be almost a shining beacon for the rest of the world in how we negotiate this change in dynamics of our cryptography and how we progress in a post-quantum world.”

But this is not to say that leaders within the industry are not already aware of quantum attacks, and are working on providing a safe and secure solution to prevent them from spiralling out of control.

“There are a lot of projects working to make Bitcoin post-quantum secure,” revealed Kearney.

“Vitalik Buterin has spoken extensively on how they are planning making Ethereum post-quantum resistant. But I think in the next few years we are going to see how difficult this problem is going to be.”

Why blockchain should be considered

Although the potential rise of quantum attacks may deter outside companies from venturing into the space, Huber believes that blockchain will become an increasingly viable solution for these companies.

He said: “What becomes incredibly attractive right at the beginning of the process is the use of a public blockchain which is that local admin has the opportunity to change digital data without much risk.

“With a public blockchain, there is no admin that can be tampered with. In our case, the blockchain we develop on is BitcoinBSV, and there has been an increase in demand for proof-of-stake alternatives.

He continued: “I think for us the reaction has been very positive. We want to build a blockchain solution to make life easy. We come from the perspective that, together with regulation and the constraint with the work that you do, we want to understand the pain points and provide a solution that relieves you of those problems.”